Key Details:

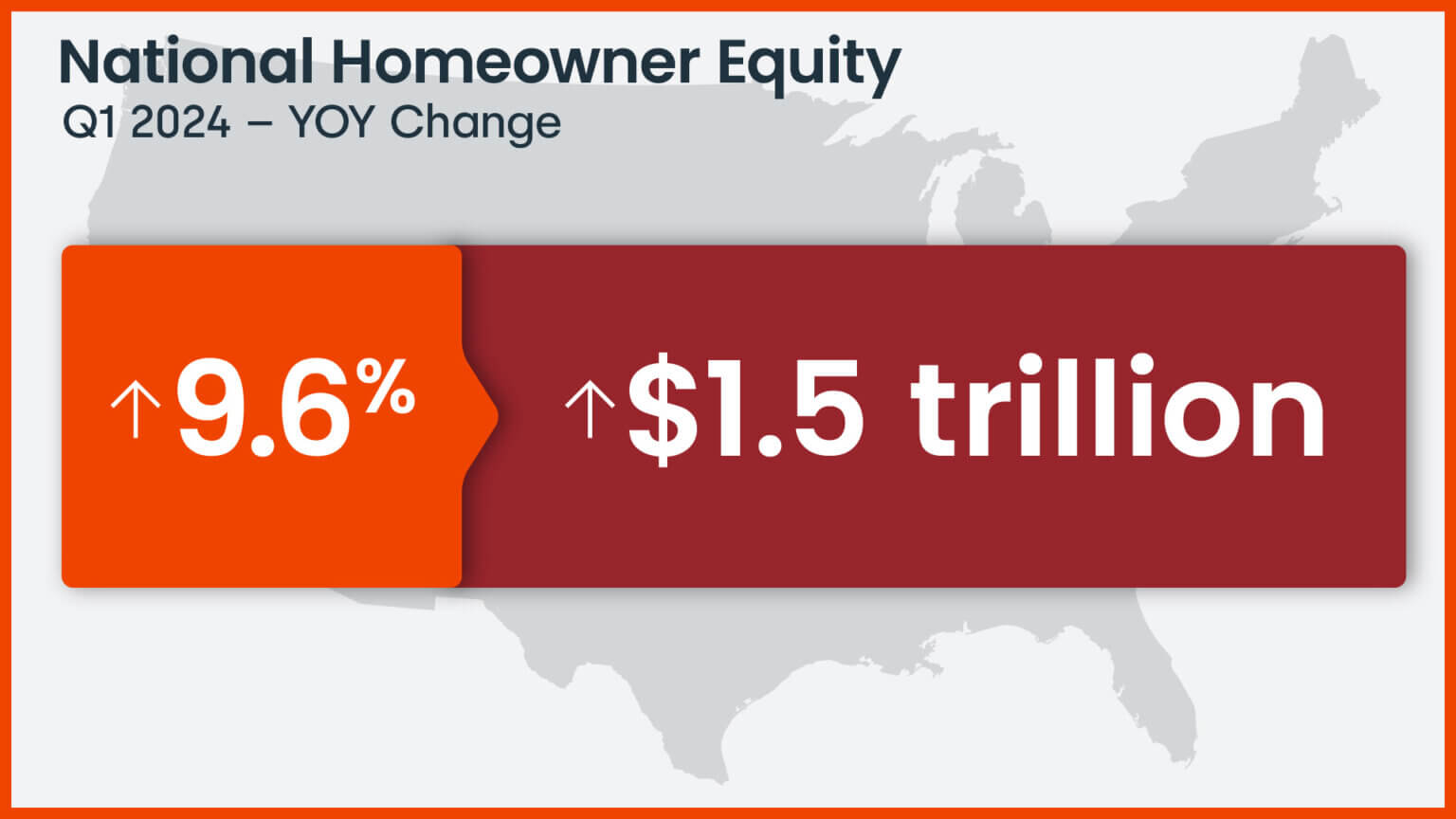

- CoreLogic released its quarterly Homeowner Equity Insights report for Q1 2024, which shows a 9.6% year-over-year increase in total homeowner equity.

- The report also highlights a 2.1% quarterly decline and a 16.1% annual decline in mortgage residential properties with negative equity.

In the first quarter of 2024, U.S. homeowners with mortgages (accounting for roughly 62% of all properties) gained 9.6% in total equity from Q1 2023.

That’s according to CoreLogic’s Homeowner Equity Insights report, which also highlighted a drop in the number of mortgaged homeowners with negative equity.

From Q4 2023 to Q1 2024, that number dropped 2.1%. Year over year, it declined by 16.1%.

Homeowners with negative equity are also described as being “underwater,” since the level of their debt is higher than the level of their home’s current market value.

That said, as home values increase (as recent forecasts suggest) and homeowners continue paying their mortgages, the number of underwater mortgages is likely to continue declining.

Data for this report is based on properties with outstanding mortgages. Non-mortgaged homes (those currently owned outright) are not included in the numbers.

Equity increased year over year while negative equity declined

In Q1 2024, homeowners with mortgages saw a total equity increase of $1.5 trillion since Q1 2023—marking a 9% annual gain.

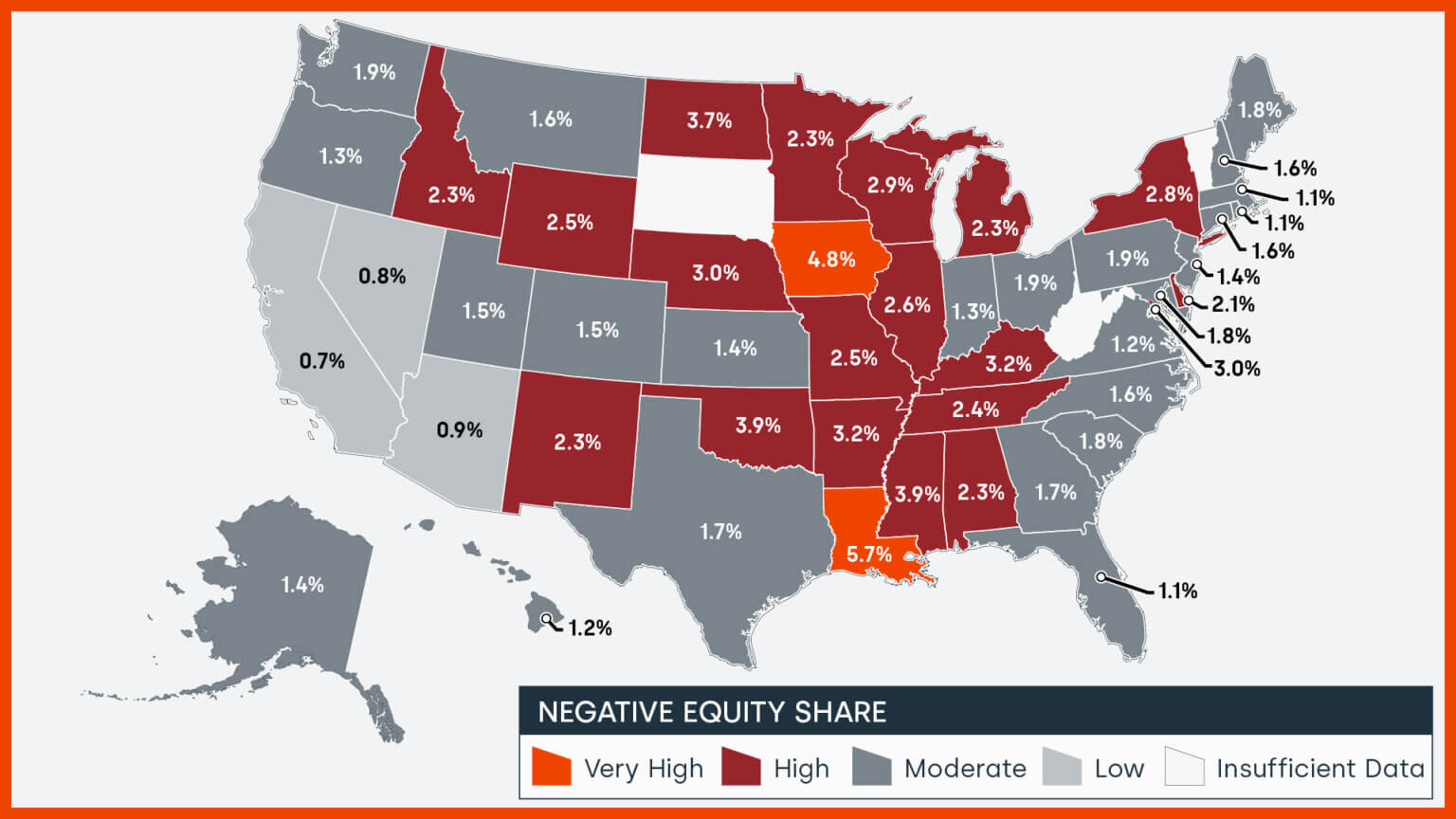

Meanwhile, the number of underwater mortgages—i.e., mortgages with negative equity—fell 2.1% from the previous quarter (Q4 2023), equivalent to 1 million homes or 1.8% of all mortgaged U.S. properties.

Year over year, the number declined by 16.1%, representing 1.2 million homes (2.1%).

Because home price changes affect home equity, borrowers whose equity is near the negative equity cutoff (+/-5%) are likely to move out of or into negative equity as prices rise and fall.

Looking at outstanding mortgages in Q1 2024, if home prices rise by 5%, 110,000 homes would move out of negative equity into positive. If home prices drop by 5%, 153,000 mortgages would go underwater.

According to the most recent CoreLogic HPI Forecast™, home prices will rise by 3.7% year over year from March 2024 to March 2025.

Nationwide, at the end of the first quarter, the aggregate value of negative equity stood at $321 billion—down $2.8 billion (or 1%) from the previous quarter and down $17.6 billion (5%) year over year.

With home prices continuing to reach new highs, owners are also seeing their equity approach the historic peaks of 2023, close to a total of $305,000 per owner. Importantly, higher prices have also lifted some 190,000 homeowners out of negative equity, leaving only about 1.8% of those with mortgages underwater. Home equity is key to mortgage holders who have seen other homeownership costs soar, including insurance, taxes and HOA fees, as a source of financial buffer. Also, low amounts of negative equity are welcomed in markets that have shown price weaknesses this spring, such as Florida (1.1% of homes underwater) and Texas (1.7% of homes underwater) — both of which are below the national rate — as further price declines could drive more homeowners to lose their equity.

For context, negative equity peaked in Q4 2029 at 26% of all mortgaged U.S. properties, shortly after the start of CoreLogic’s equity data analysis in the third quarter of the same year.

Equity changes at the state and metro level

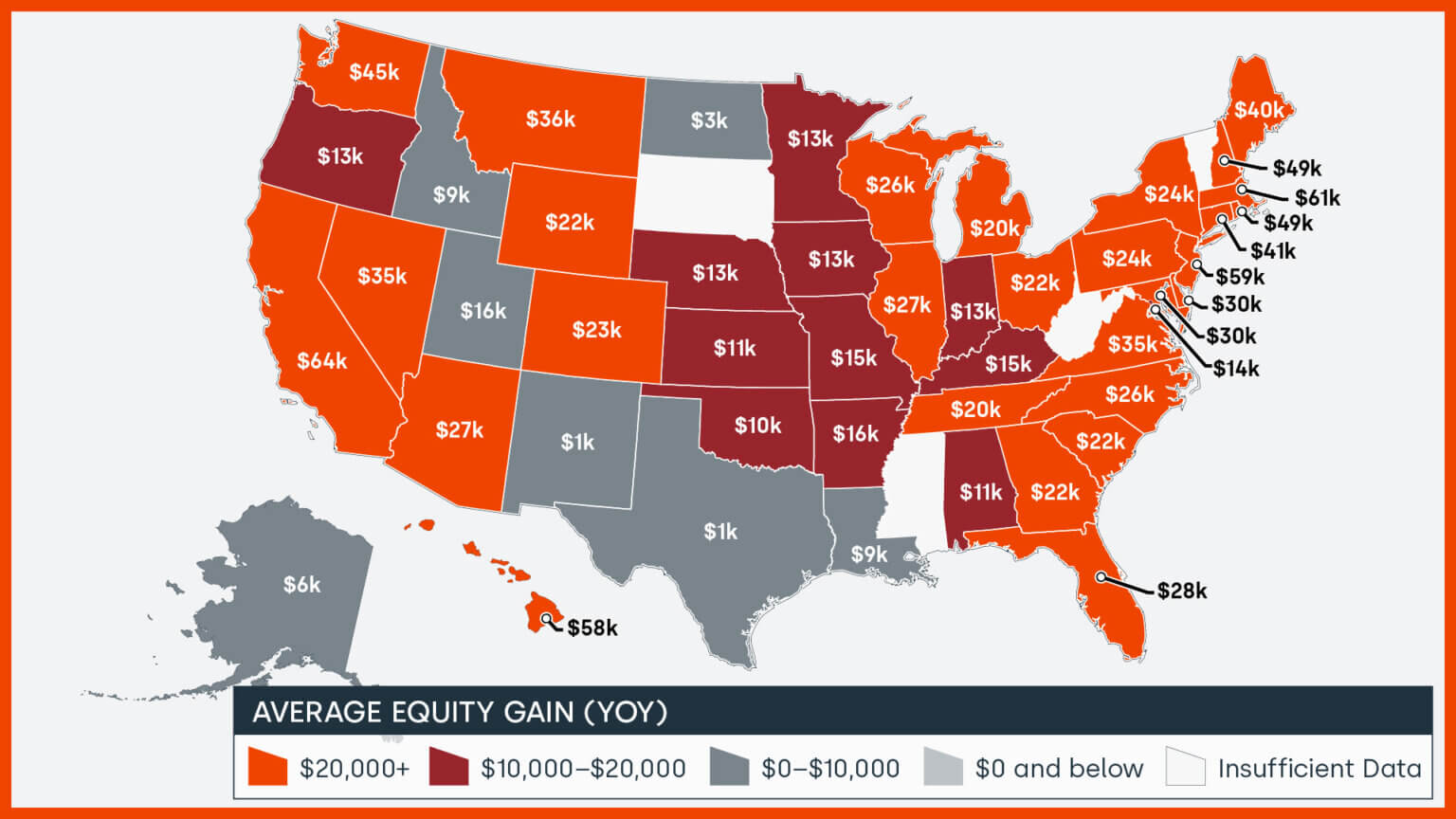

Mortgaged homeowners in California saw the biggest equity gains in Q1 2024 at $64,000, with Los Angeles netting even more at $72,000. The average homeowner in the U.S. gained $28,000 in equity year over year. Not a single state reported an annual equity loss.

States with the biggest annual gains in homeowner equity:

- California (Homeowners gained $64,000 in equity year over year in Q1 2024)

- Massachusetts ($61,000)

- New Jersey ($59,000)

- New Hampshire ($49,000)

- Rhode Island ($49,000)

- Washington ($45,000)

At the state level, negative equity share—the share of outstanding mortgages in a particular state that are underwater—is lowest in Las Vegas at 0.6%, followed by Los Angeles (0.7%) and San Francisco (0.8%).

The chart below shows negative equity shares for 10 select large U.S. metros, based on CoreLogic’s detailed equity data for these markets.

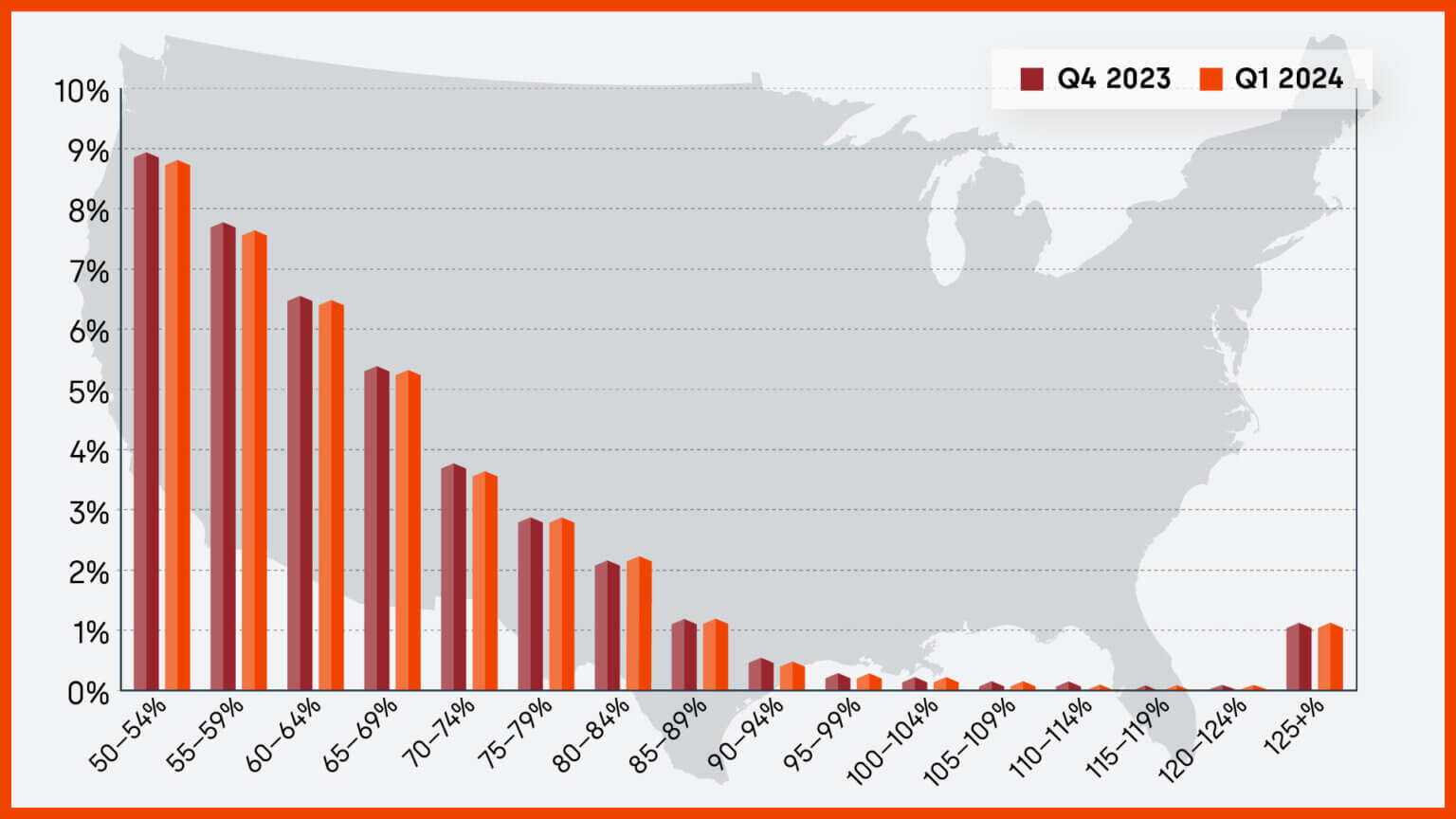

The CoreLogic report also includes a chart illustrating changes in national home equity distribution across multiple loan-to-value (LTV) segments for Q4 2023 and Q1 2024.

Read the full report for more information, including methodology.

- BAM")