Key Details:

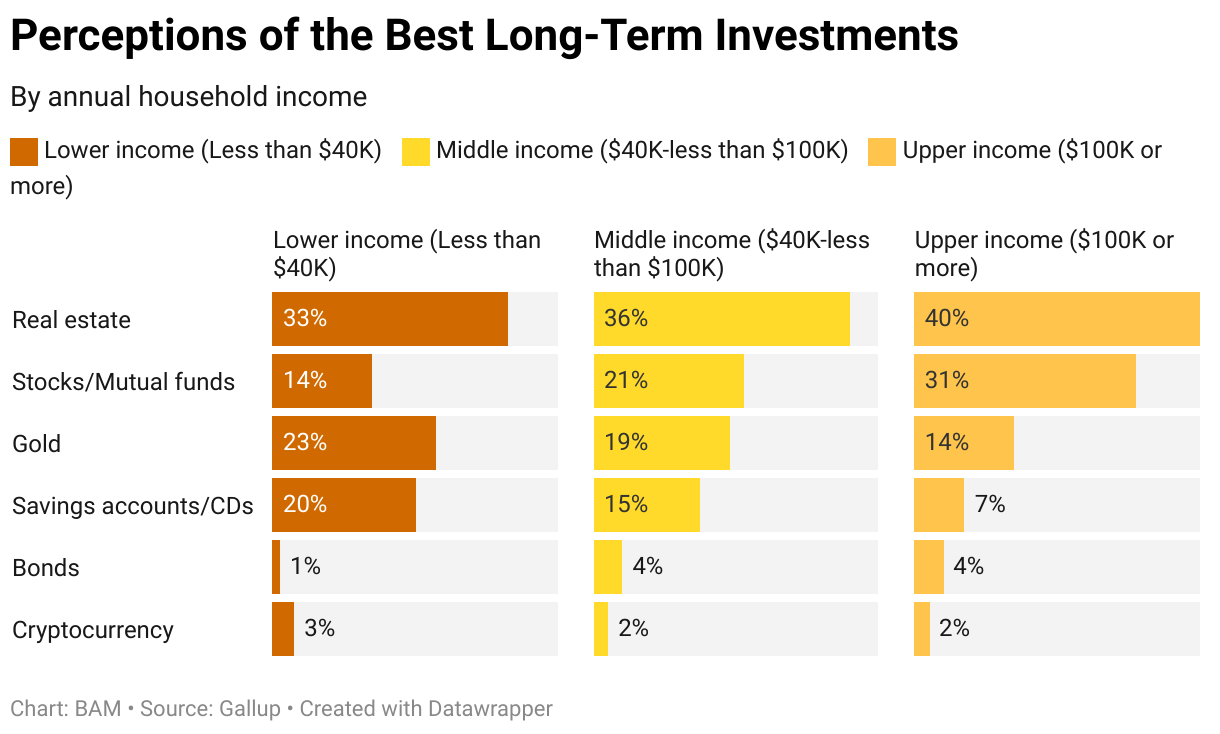

- Over one-third (36%) of Americans see real estate as the best long-term investment, not so much because of its potential returns but because of its overall stability, with home value consistently climbing.

- Another advantage to housing as a long-term investment is its versatility; the investor gets to live in it as its value grows.

A recent Gallup poll shows 36% of Americans rank real estate as the number one long-term investment.

That said, according to a CNBC article, some financial pros are saying they might be wrong.

Don’t discount that 36% just yet, though. There are multiple reasons they put buying real estate at the top of all their long-term investment options.

For one (and this is something no other investment vehicle can offer), folks who buy a home can actually live in it while its market value continues to grow.

Consumers value safety and stability over massive returns

For that 36%, the best long-term investment option isn’t necessarily the one with the biggest potential for returns. These consumers rank safety and stability higher on the list of desirable qualities for investment vehicles.

After all, even if their home value doesn’t grow as quickly as they hoped when they bought the home, it still gives them a place to live.

Some homeowners are leveraging their home equity to make a down payment on a rental property to bring in additional income—an investment strategy known as “house hacking.”

According to some financial pros, however, putting all your eggs in the real estate basket may not be the best investment strategy.

Brian Vendig, president at MJP Wealth Advisors, recommends spreading investment dollars across different asset types—which deliver different types of income and are subject to different market forces, increasing the odds of a net profit over the long term.

We allocate alternative investments for clients—including real estate—around a core, traditional portfolio [of stocks and bonds]. Real estate is not only a great hedge for inflation, but it also generates tax-advantageous income.

For many Americans, though, buying a home gets them the most bang for their buck. And for buyers facing affordability challenges, contributing to other monthly investments may be a big ask—especially if paying for a knowledgeable advisor is outside their current budget.

So, it’s not surprising to see household income influence consumer rankings of long-term investments.

Steady home price growth adds to consumer confidence

Judging by the data on home price growth over the past decades…home price growth is pretty much a given. There may be hiccups along the way—the Great Financial Crisis (GFC) of 2008 coming to mind. But overall, home prices have consistently trended upward.

This graph from Lance Lambert at ResiClub makes that general upward trend hard to miss.

The above chart is a Byron Lazine favorite that is well worth sharing with well-meaning relatives warning that home prices are about to crash. And as Lazine has pointed out multiple times on the Hot Sheet, the current market is not even close to the market we had before the GFC.

Here’s a quick overview from the ResiClub article on U.S. home price growth by decade:

- +30.1% – ‘90s decade

- +47.3% – ‘00s decade

- +44.7% – ‘10s decade

- +47.1% – ‘20s decade

Also, according to ResiClub founder Lance Lambert, the 2020s stand out with a higher level of home price inflation before the midpoint compared to the previous three decades.

Read the full ResiClub article for more.