Key Details:

- A new market report from Zillow brings some encouraging news for both homebuyers and sellers at the end of 2023.

- Lower rates have shaken some sellers free from the lock-in effect and, combined with slightly lower home values, have made slight improvements to housing affordability for homebuyers.

- New listings are still below pre-pandemic norms, but the gap, which peaked at roughly 35% in April, dropped to about 14% in November.

- Price cuts are still more common than normal as motivated sellers respond to high rates.

Zillow released its November market report with some encouraging news for homebuyers. As mortgage rates have dropped from just above 8% in October, more sellers have re-entered the housing market, adding to available inventory.

And while rates remain high, these sellers are still making more price cuts than normal.

Add that to the slight improvement in monthly housing costs due to lower rates and small declines in home values, and buyers are understandably more hopeful about finding an affordable home this time of year—or early into the next.

Mortgage rates and home prices are ticking down

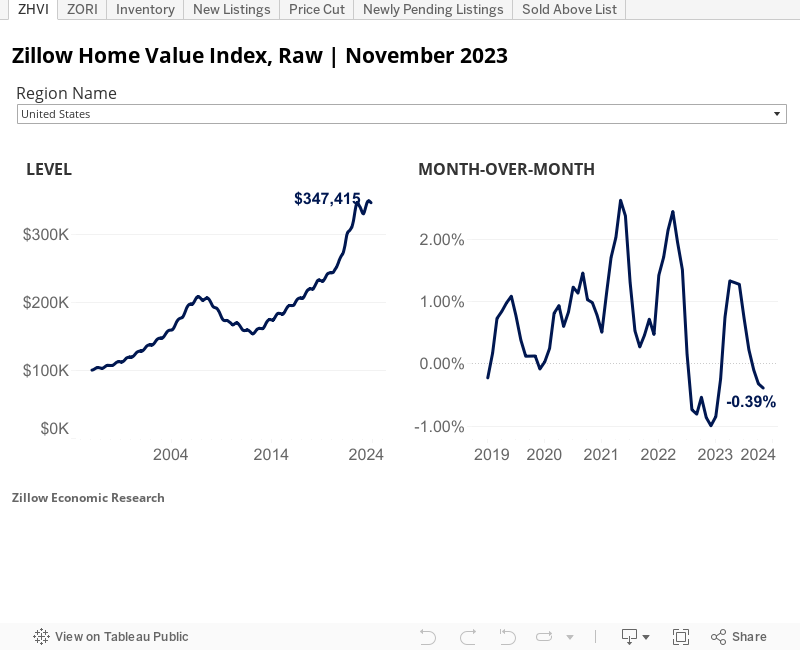

November brought some month-over-month declines in housing costs, mostly due to lower mortgage rates. But those rates are still high enough to have a cooling effect on demand, which has helped drive home prices down a tick.

Meanwhile, annual growth in the Zillow Home Value Index (ZHVI) keeps climbing, even as more negative monthly home price trends reflect the impact of mortgage rates that stayed above 7% for prime borrowers in November.

Source: Zillow

The typical U.S. home value for the month was $347,415. And the typical monthly mortgage payment was $1,925, assuming a 20% down payment. That’s up 9% from a year ago and up 120% compared to before the pandemic.

Month over month, home values increased in only two of the 50 most populous U.S. metros:

- Miami, FL (0.3%)

- Las Vegas, NV (0.1%)

The five metros with the largest monthly declines in home values:

- New Orleans, LA (-1.6%)

- Austin, TX (-1.3%)

- San Antonio, TX (-1%)

- Minneapolis, MN (-1%)

- San Francisco, CA (-0.8%)

On an annual basis, home values increased in 37 of the 50 most populous U.S. metros.

The five metros with the highest annual increases:

- Hartford, CT (11.3%)

- Milwaukee, WI (8.5%)

- San Diego, CA (7.6%)

- Providence, RI (7.4%)

- Boston, MA (7.2%)

The five metros with the largest annual declines in home values:

- New Orleans, LA (-8.9%)

- Austin, TX (-8.2%)

- San Antonio, TX (-3%)

- Jacksonville, FL (-1.5%)

- Memphis, TN (-0.9%)

Inventory is slowly climbing to shrink the shortfall from pre-pandemic levels

As November wrapped up, new listings were at 14.1% below pre-pandemic norms for this time of year—compared to the 34.8% shortfall we saw seven months ago in April.

It’s a welcome change, if a small one, as more sellers return to the market, partly due to the drop in mortgage rates and possibly also because of a mindset shift in those no longer expecting rates to fall much further (if at all) in the near future.

Month-over-month, new listings still dropped 20.5% in November, but they were 3.1% higher than a year ago, despite mortgage rates being higher this year.

Total housing inventory for November—meaning the number of listings active at any time during the month—fell by 5.3% month over month and was 2% lower than a year ago.

Inventory levels for November were 37.2% below pre-pandemic norms for this time of year.

Price cuts are still more common than normal

While the share of listings with price cuts is down 1.6 percentage points compared to a year ago, it remains unseasonably high at 22.6%, which is a 2.5 percentage point drop from October’s 25.1%.

Compared to typical November levels, more home sellers are making price cuts in response to higher mortgage rates and overall affordability challenges for buyers.

Home sales are down—but homes that do sell are selling quickly

As mortgage rates dropped to levels close to what we saw at the end of 2022, available homes also spent less time on the market.

Homes that sold in November spent only a median of 21 days on the market before going under contract—five days slower than the previous month but one day faster than November 2022 and more than two weeks faster than what was normal for this time of year before the pandemic.

Even with some buyers still on the sidelines due to high mortgage rates, inventory was still no match for existing demand, which kept competitive pressure fairly high for homes that were selling.

That said, newly pending sales dropped 15.9% month over month in November and were down 4.6% from a year ago.

Rents dropped month over month, in line with seasonal norms

Month over month, asking rents ticked down across the U.S. in November to a level close to historic norms for this time of year. Compared to a year ago, rents were up 3.3%.

Rent growth has been stronger for single-family homes (+4.8% year over year) compared to multi-family homes (+2.5%). According to Zillow’s 2024 housing predictions, that trend is likely to continue.

Source: Zillow

The Zillow Observed Rent Index (ZORI) puts the typical U.S. rent for November at $1,982, showing a month-over-month decline of 0.2%, compared to the pre-pandemic average change of -0.1% for this time of year.

Source: Zillow

Compared to the previous month, rents dropped in 32 of the 50 largest U.S. metros.

The five metros with the largest monthly declines in November:

- Raleigh (-0.9%)

- San Jose (-0.8%)

- San Francisco (-0.8%)

- San Diego (-0.8%)

- Austin (-0.7%)

Compared to a year ago, November rents were up in 47 of the 50 largest U.S. metros.

The five metros with the largest annual increases in rent:

- Providence (7.3%)

- Hartford (7.2%)

- Cincinnati (6.4%)

- Columbus (5.8%)

- St. Louis (5.7%)

Read the full report for more.

- BAM")