A single Truth Social post from President Trump sparked one of the loudest housing debates of 2025: would a 50-year mortgage help buyers or trap them?

On Saturday, November 8, President Trump floated the idea of a 50-year mortgage to help more potential buyers enter the market. As several analysts pointed out, stretching a loan an extra 20 years would lower monthly payments. But that doesn’t mean everyone is on board.

Reactions were immediate and divided, ranging from applause for the potential affordability boost to concern from economists warning of long-term risks.

Here’s what we’re seeing so far from folks across the industry, including Byron Lazine, who broke down the news on today’s Hot Sheet.

What President Trump Actually Proposed (and Why)

Trump’s weekend post compared the 30-year mortgage, introduced under Franklin D. Roosevelt, to his proposed 50-year plan, suggesting it could be a “game changer” for housing affordability.

Soon after, Federal Housing Finance Agency (FHFA) Director Bill Pulte appeared to confirm the idea on X:

“Thanks to President Trump, we are indeed working on The 50-Year Mortgage, a complete game changer.”

Thanks to President Trump, we are indeed working on The 50 year Mortgage – a complete game changer. https://t.co/HZDPzO0qJG

— Pulte (@pulte) November 8, 2025

Byron went over the proposal on today’s Hot Sheet and shared his biggest concerns with it. For one, as long as the Dodd-Frank Wall Street Reform and Consumer Protection Act remains in place, the maximum loan term for a qualified mortgage is 30 years.

Anything over that would be considered a non-QM loan and would not have the same government guarantee of coverage if the borrower defaults on their mortgage.

“Those usually come with a higher rate and stricter underwriting standards because the bank knows the government, Uncle Sam, is not going to bail them out… When the bank doesn’t have Uncle Sam helping them, they’re more conservative.”

So, we’re looking at either a non-QM loan with a 50-year term or, if Dodd-Frank is overturned (which is unlikely), the maximum term for government-subsidized loans would go up to 50.

And that presents another issue for buyers and their agents to keep in mind.

“You can make the argument that some of the 30-year fixed mortgage products available today are subsidizing, which has increased home values. When we went down to 0% rates, we were subsidizing the market.

“…You’ve seen this in student loans. You subsidize the student loan and costs go up. You’ve seen this in health insurance. You subsidize health insurance, what happens? Health insurance keeps going up… Subside mortgages, what happens? House prices keep going up.”

He brought up Dave Ramsey, who famously discourages homebuyers from taking out a 30-year mortgage, arguing that the interest homebuyers pay on a 30-year versus a 15-year mortgage is best avoided, if at all possible.

The math for a 50-year is an even bigger lump to swallow.

“Look at all the interest you’d pay on the 50-year! It’s astronomical! Now, you’re not going to stay in the same home for 50 years, I get that. But you’re essentially renting from the bank at that point; the bank gets to collect more fees, you slow down that equity growth… The 50-year mortgage doesn’t solve the problem. It’ll only extend this unaffordability that we talk about…

“You saw a lot of backlash on this, and I think for the right reasons. The real estate community understands what would happen: the more you step in as a government and try to inflict your will on the free market, the more you inflate prices.”

Short-Term Upside vs Long-Term Risks

On the surface, the math seems simple. Extending a loan term reduces monthly payments, which could make homeownership more accessible in a high-rate environment.

According to USC housing economist Richard Green, a 50-year loan would cost about $564 per $100,000 borrowed, compared to $632 for a 30-year mortgage. For a $500,000 loan, that’s roughly $340 less per month.

But that short-term relief comes with a long list of tradeoffs:

- Higher total interest costs: Longer-term loans carry higher rates since they’re riskier for lenders.

- Slower equity growth: More of each payment goes toward interest, meaning buyers build wealth at a crawl.

- Greater risk of negative equity: If prices dip, borrowers could end up owing more than their homes are worth.

After the 2008 housing crash, millions of underwater homeowners defaulted when their equity vanished. Researchers found borrowers with negative equity were “150% to 200% more likely to default” than those with positive equity.

Industry Reactions So Far

Public response to the idea has been explosive.

Marjorie Taylor Greene, one of Trump’s own allies, pushed back, writing:

“It will ultimately reward the banks, mortgage lenders and homebuilders while people pay far more in interest over time and die before they ever pay off their home.”

I don’t like 50 year mortgages as the solution to the housing affordability crisis.

It will ultimately reward the banks, mortgage lenders. and home builders while people pay far more in interest over time and die before they ever pay off their home.

In debt forever, in debt for…

— Rep. Marjorie Taylor Greene🇺🇸 (@RepMTG) November 8, 2025

Investor Graham Stephan echoed that sentiment, warning:

“A 50-year mortgage would let you buy about 10% more house, but at the expense of nearly doubling your payment schedule. There’s no way that ends well.”

Not everyone disagreed with the idea, though. Investor John Pompliano wrote:

“The 30 year mortgage is one of the best financial products available to Americans. 50 years is even better.”

While crypto analyst Wendy O argued it gives consumers the freedom to pay off early if they choose.

After all, not all renters are going to see this as a disaster in the making. Some will see it as a chance to pay less for a home with more rooms and a shot at eventually building equity. So, sort of like renting…but with a foot in the homeownership door and more space to call their own.

For some of them, equity won’t be the immediate concern or the primary motivator. All the more reason for knowledgeable real estate pros to help them see the fuller picture of the “savings” they’re hearing about.

They might be thinking, “So, I can finally say goodbye to annual rent increases and lock in a house with more living space at a lower monthly payment? Sign me up!”

Of course, that assumes the monthly savings would be enough to make it worthwhile. And judging by a recent Mike Simonsen Tweet, the math is a lot less impressive than what the imagination might immediately suggest.

Here’s how good a deal that 50-year loan is likely to be. pic.twitter.com/Y8bpW9xMge

— Mike Simonsen 🐉 (@mikesimonsen) November 9, 2025

Keep in mind, too, that the savings Simonsen calculated was for a median-priced home, not the below-median-price options a lot of renters would be looking at. Monthly savings for those would be even less.

Yet other caveat: even if 50-year mortgages become an option, how many banks will happily grant 50-year loans to homebuyers at the median age of 40-plus?

Agents React to the News

Economists, politicians, and investors weren’t the only ones to weigh in. President Trump’s proposal immediately caught fire across social platforms.

BAM’s IG post featuring Lance Lambert’s tweet on the topic drew hundreds of comments, with agents and consumers split between calling it “long overdue” and “a recipe for disaster.”

View this post on Instagram

Real estate coach Jared James and Today Years Old, also shared the headline with their audiences, each post drawing thousands of comments debating whether a 50-year mortgage would truly help affordability or simply stretch debt across generations.

View this post on Instagram

In Jared’s words:

“…Regardless of what side of this you’re on, if you’re a buyer in the market, and this happens, you’d better buy immediately! Because what this is going to do—the explosion in the market—the COVID market was a precursor to what will happen with this.”

In other words, if this gets to be a thing, and if any of your buyers are keen to take advantage of what they see as their window of opportunity finally opening, they’ll want to jump on this ASAP.

View this post on Instagram

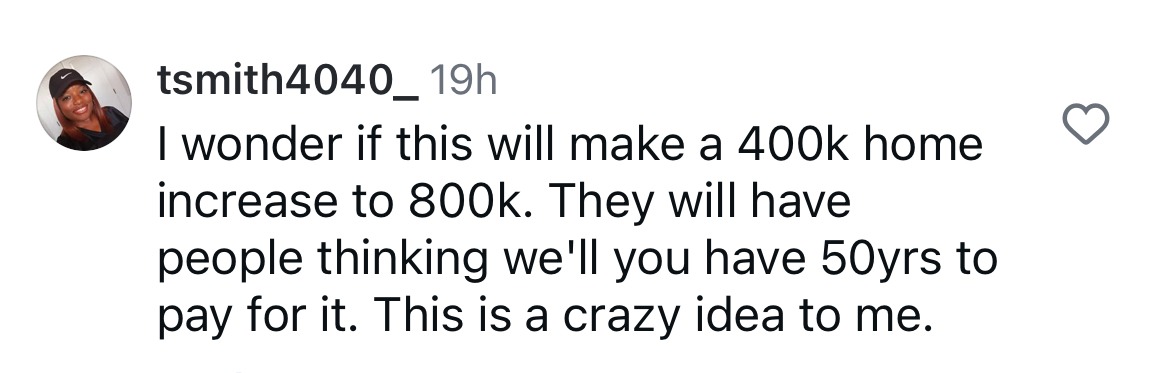

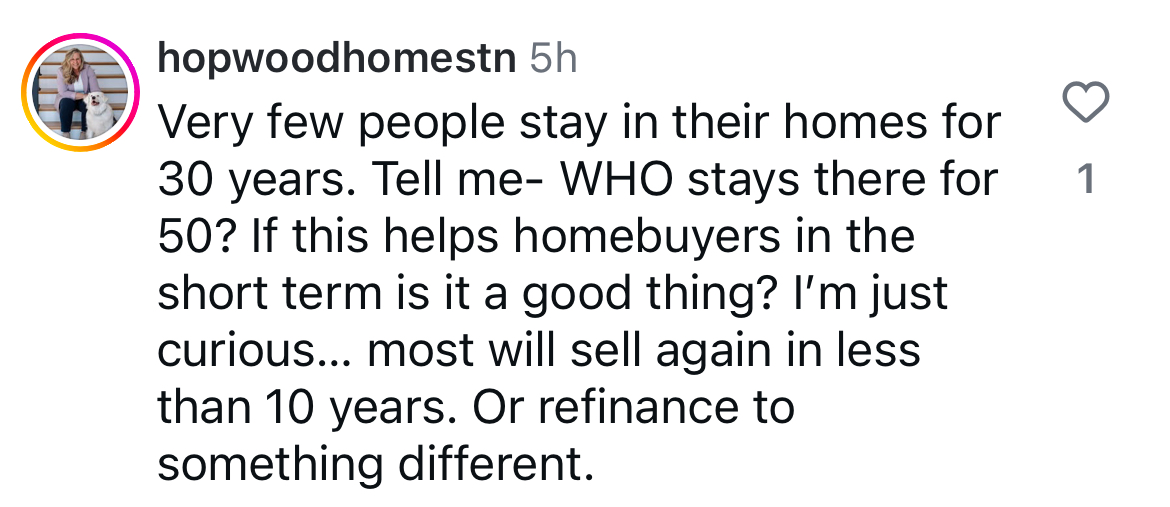

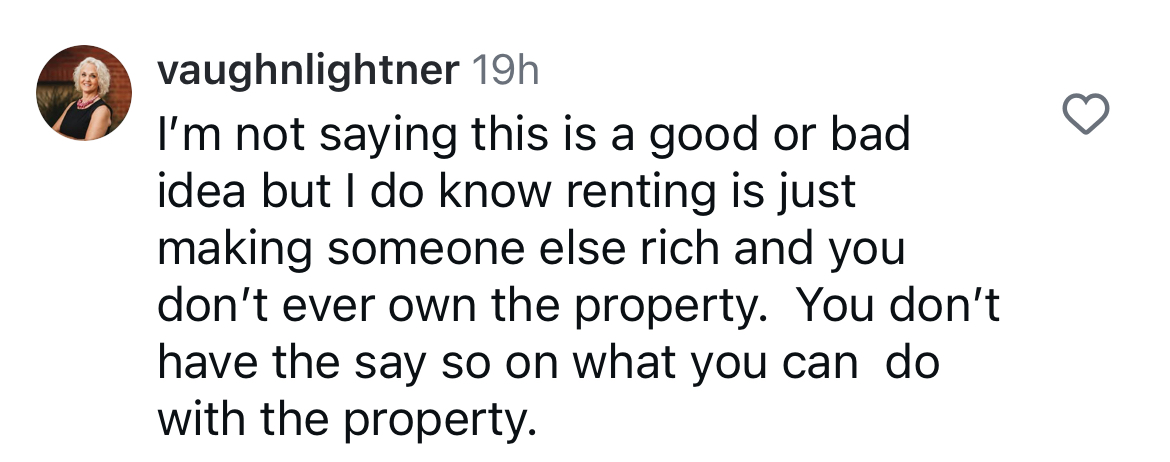

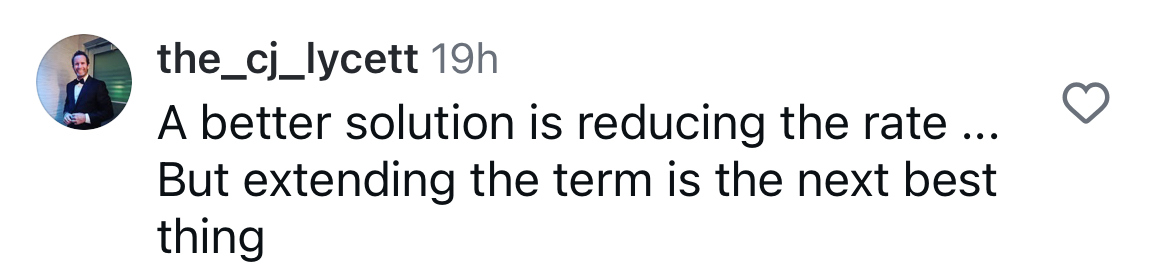

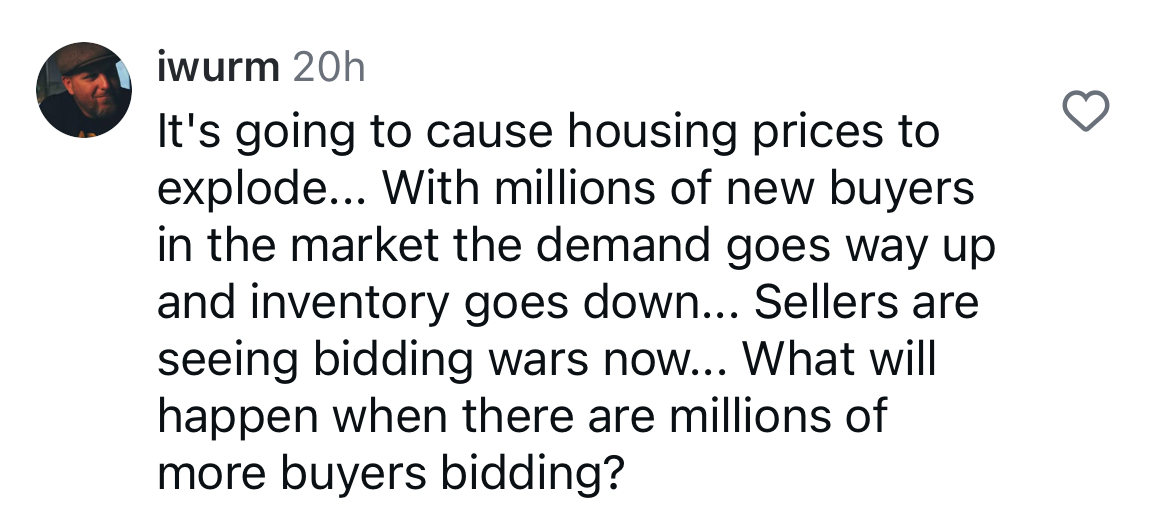

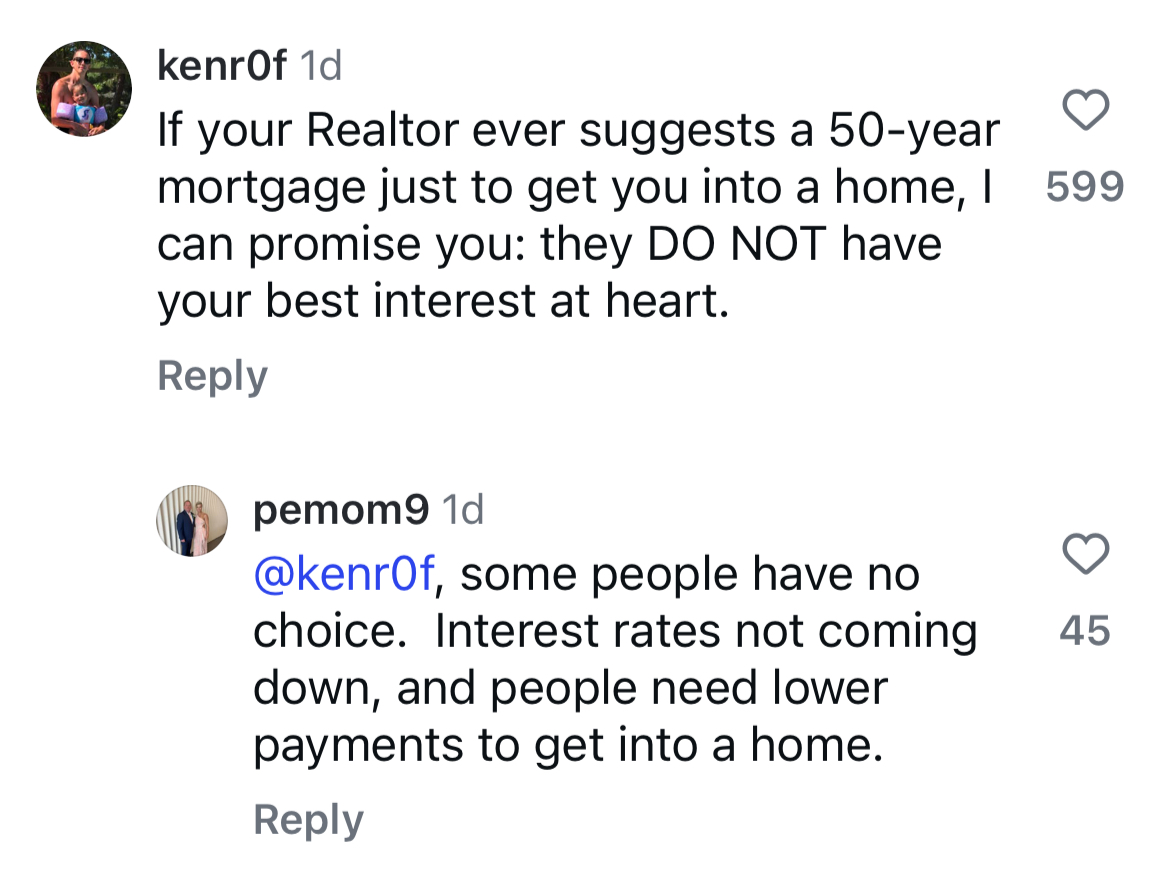

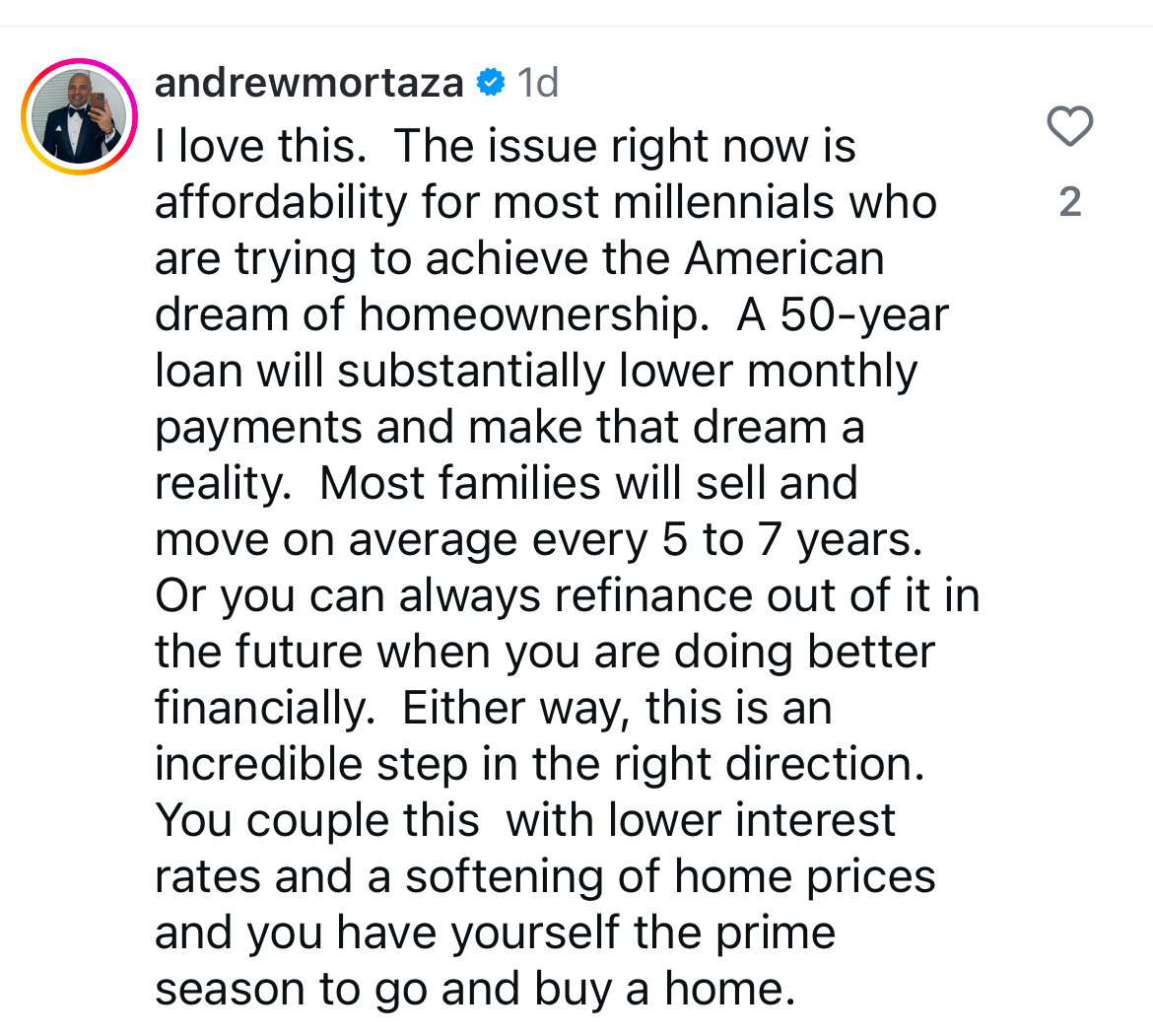

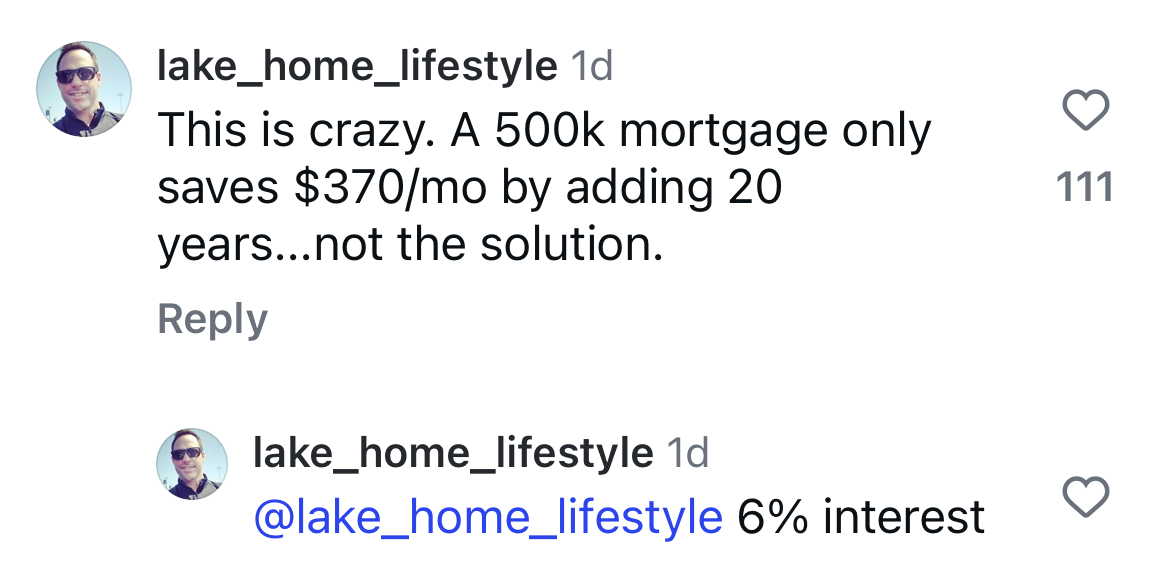

Here’s just a sampling of the reactions we’re seeing so far:

For now, though, the idea remains just that: a proposal. Whether it ever becomes reality will depend on sweeping legislative and regulatory changes.Still, the conversation it sparked shows how desperate Americans are for relief and how closely the real estate community is watching for any shift in lending policy.

Byron’s closing thoughts sum up what a lot of real estate pros are thinking right now:

“The fact that the government is looking at a 50-year mortgage as a potential tool, as a potential fix, for the affordability issues that we’re faced with housing tells me they have no idea what they’re doing or how to solve the problem.”

Byron and co-host Nicole White also discussed the 50-year mortgage on this week’s episode of The Real Word.

So, where do you lean on this? Do you see a real potential upside for sidelined buyers, or does this feel more like a trap?

- BAM")