Key Details:

- Fannie Mae conducted a Consumer Mortgage Understanding Study in 2015, 2018, and again in 2023. The purpose of these studies is to uncover opportunities for industry professionals to address consumer knowledge gaps pertaining to mortgage qualifications, as well as to highlight areas to improve in the mortgage process.

- This article focuses specifically on consumer understanding of the mortgage process and confidence in their ability to qualify for a mortgage.

Fannie Mae’s last Consumer Mortgage Understanding Study (2023) revealed some significant shifts in consumer perceptions and attitudes compared to its earlier studies in 2015 and 2018.

Here, we’re focusing on how well today’s consumers understand the mortgage process, as well as consumer confidence in their ability to qualify for a mortgage.

One of the main factors behind that confidence is the consumer’s perception of the housing market and the overall economy.

Fewer than one in five (19%) consumers believe now is a good time to buy a home—a sharp decline from 62% in December 2018.

For those holding off on buying a home, the main reasons cited are elevated mortgage rates, high home prices, and unfavorable economic conditions:

- Home prices have grown by 57% from Q4 2018 to Q4 2023.

- The supply of existing homes for sale dropped by 35% during that time.

- The 30-year fixed mortgage rate increased by 28% in the same five-year period.

Despite those affordability challenges, though, 92% of consumers believe owning a home is important, with 70% considering a home purchase a safe investment. And 95% would rather own a home—if they could afford to—than rent one.

And among those currently renting, 21% are working on preparing themselves financially for a home purchase—up five percentage points from 2018.

Consumer Understanding of the Mortgage Process

One of the biggest challenges facing prospective U.S. homebuyers today is the persistent knowledge gap surrounding the mortgage process, including lending standards for—

- Minimum credit score (for each loan type)

- Debt-to-income (DTI) ratio

- Minimum down payment

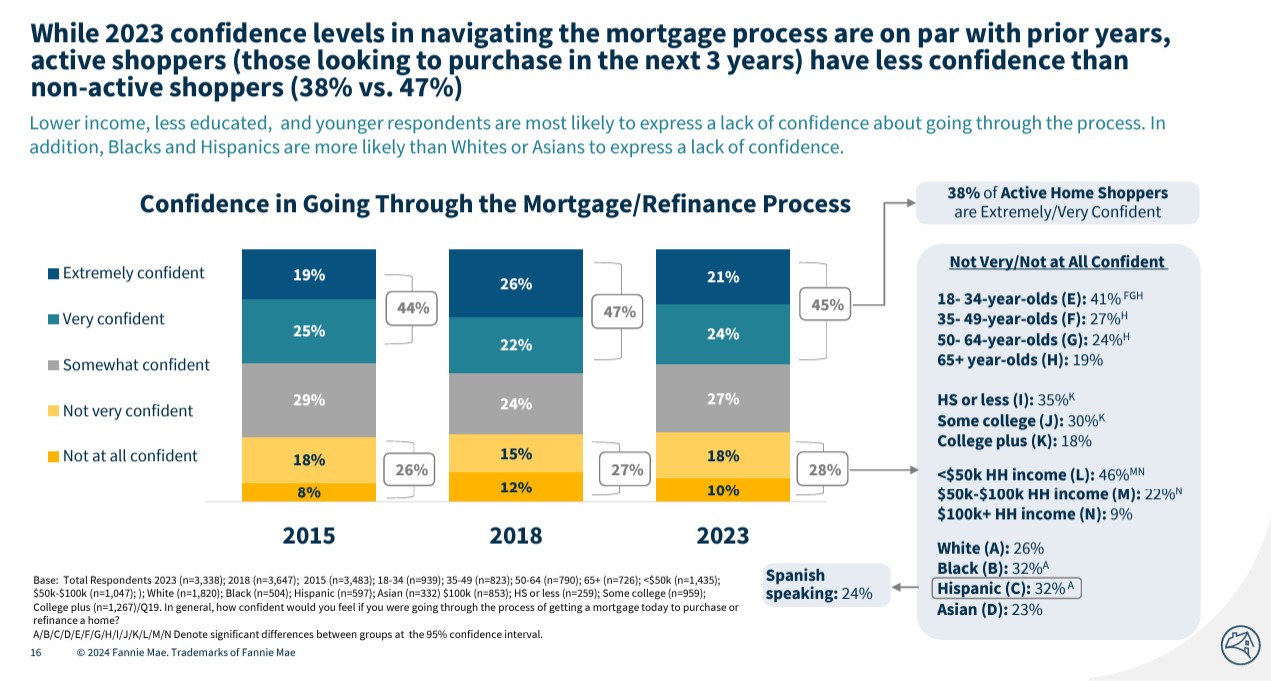

For starters, 45% of consumers not actively shopping for a home feel confident navigating the mortgage process—compared to just 38% of those who are actively home shopping.

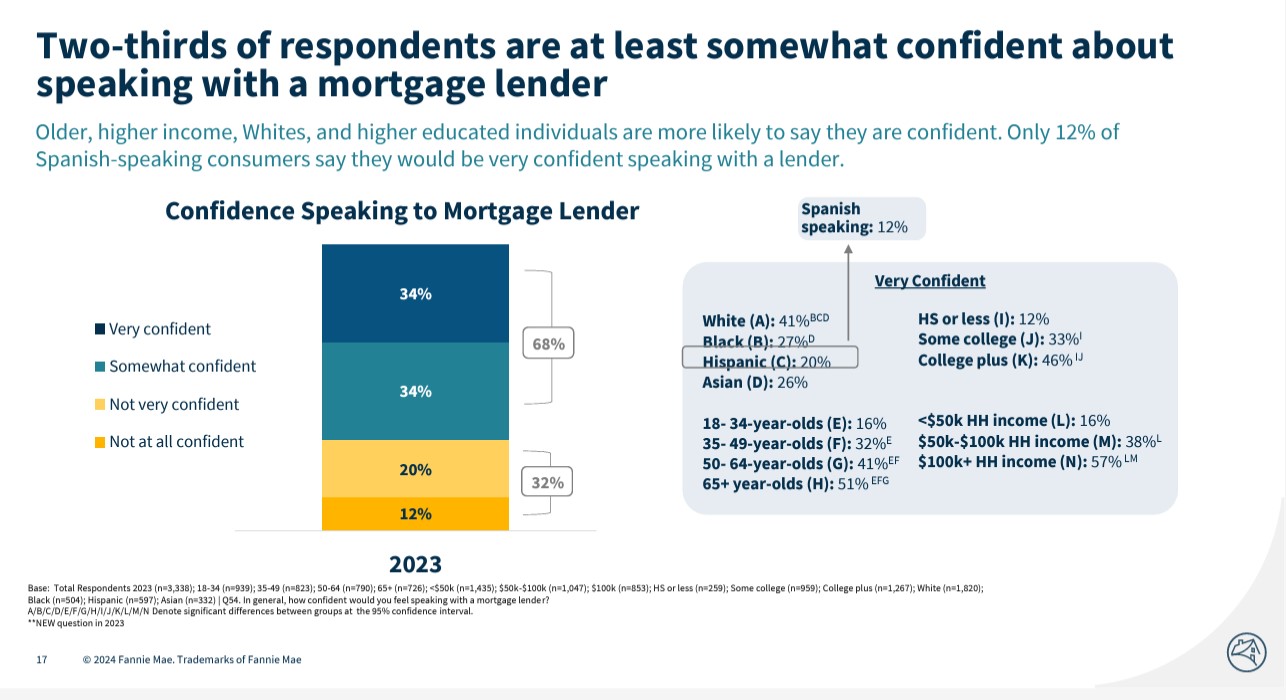

A larger percentage of consumers feel somewhat or very confident about having a conversation with a mortgage lender. That said, non-white, lower-income, and younger borrowers report less confidence.

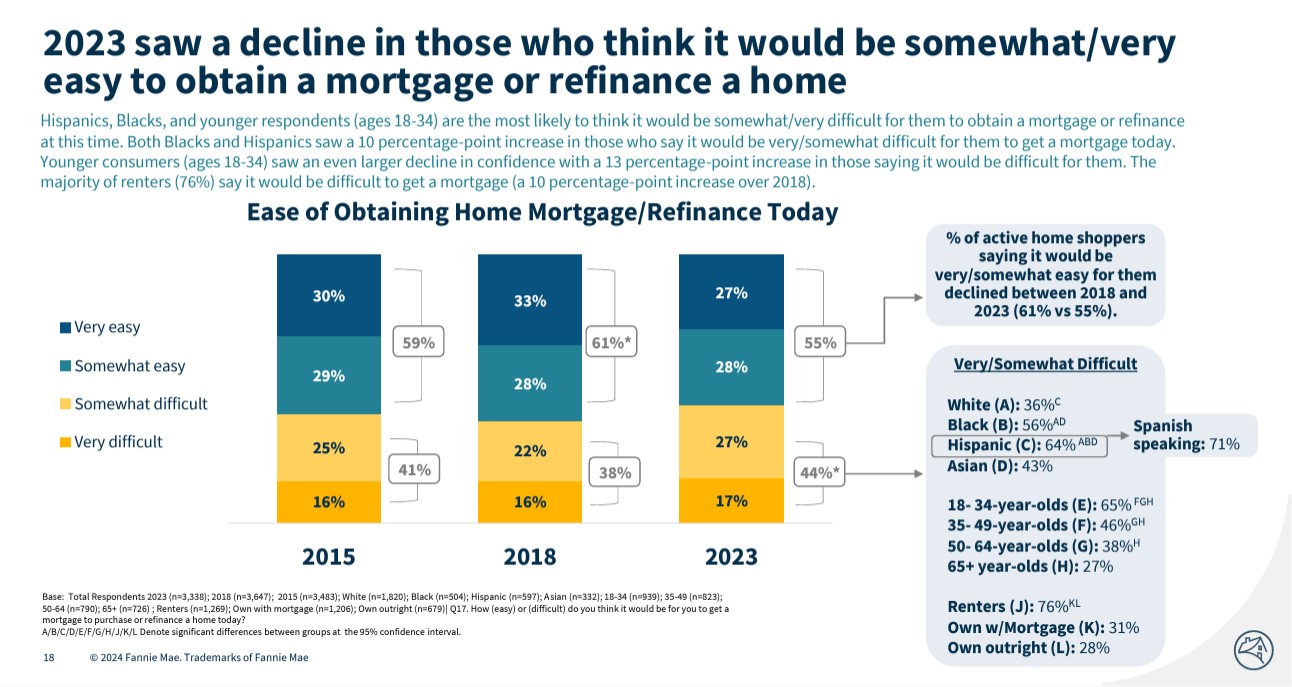

Among those actively searching for a home to buy, a little more than half (55%) expect it to be somewhat easy or very easy to obtain a mortgage—down from 61% in the 2018 study.

When it comes to specific lending standards, 90% of consumers in the 2023 study overstate or are unaware of the minimum down payment required.

Just under one-third of them (32%) are unaware of or significantly over/underestimate the minimum required credit score.

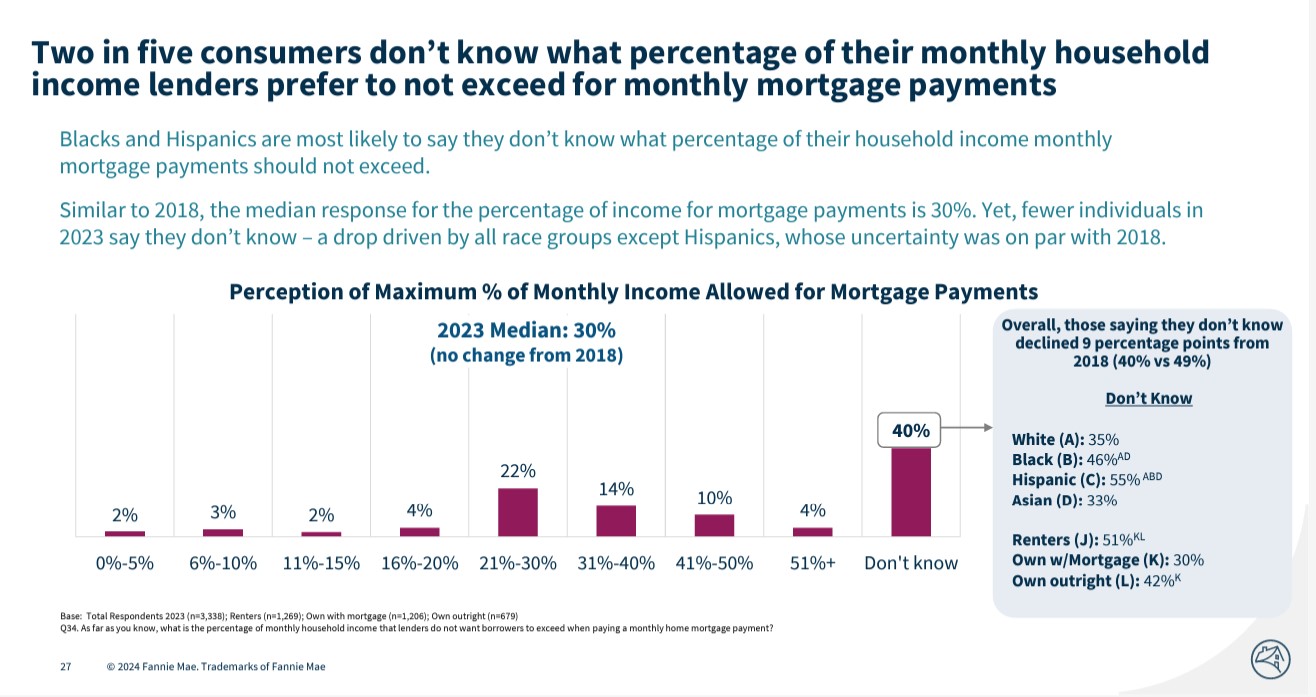

Two in five consumers (40%) don’t know what percentage of their household income lenders prefer not to exceed for estimated monthly mortgage payments.

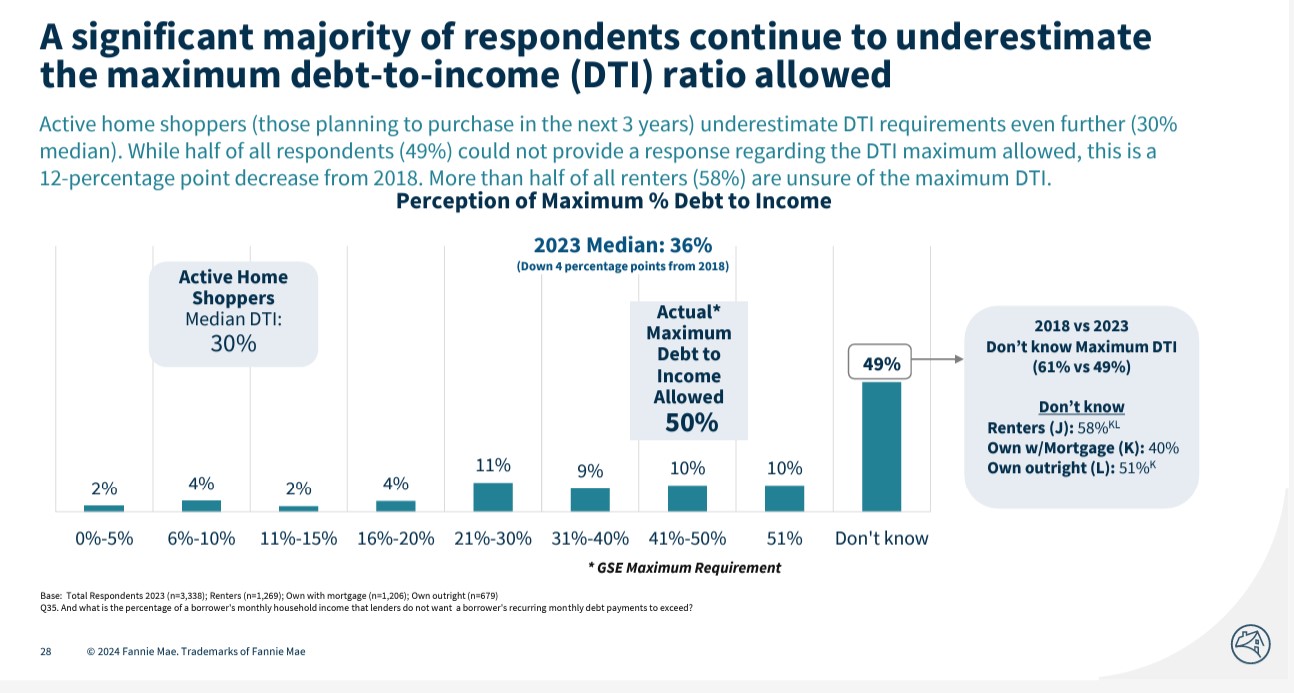

And nearly half (49%) continue to underestimate the maximum debt-to-income (DTI) ratio allowed.

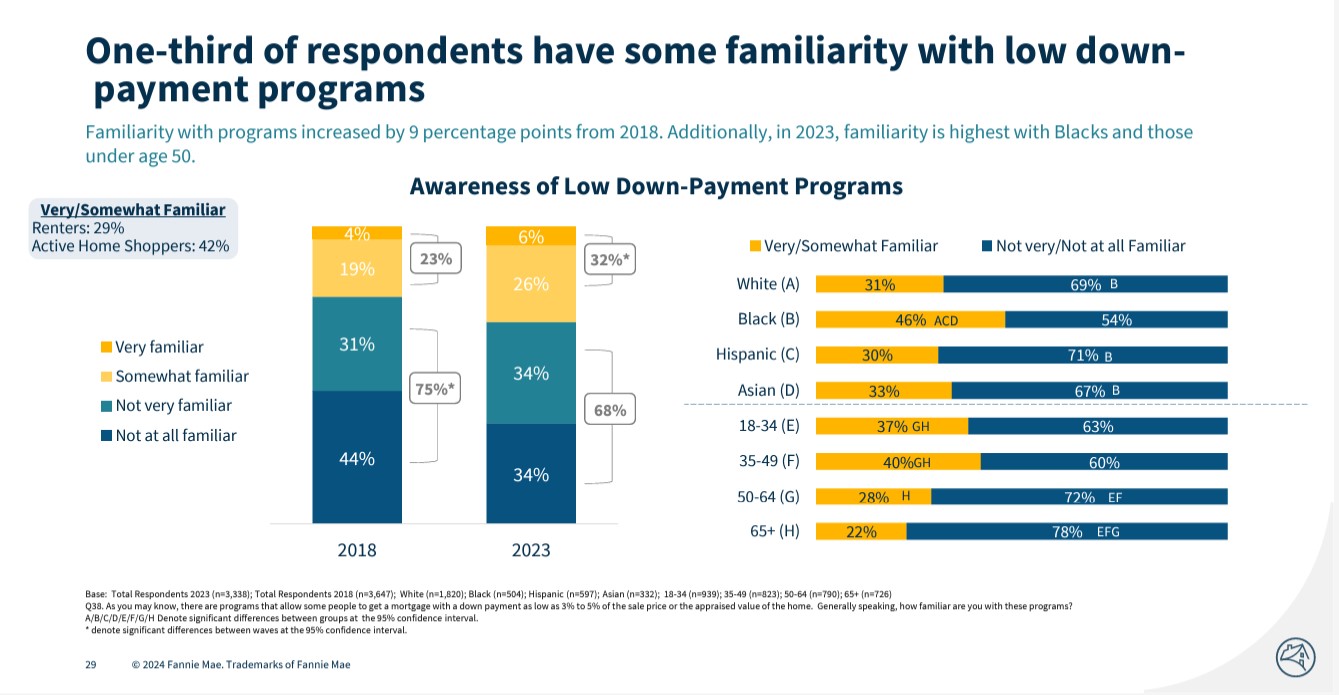

Just 32% are “somewhat” or “very” familiar with low down-payment programs—up from 23% in 2018.

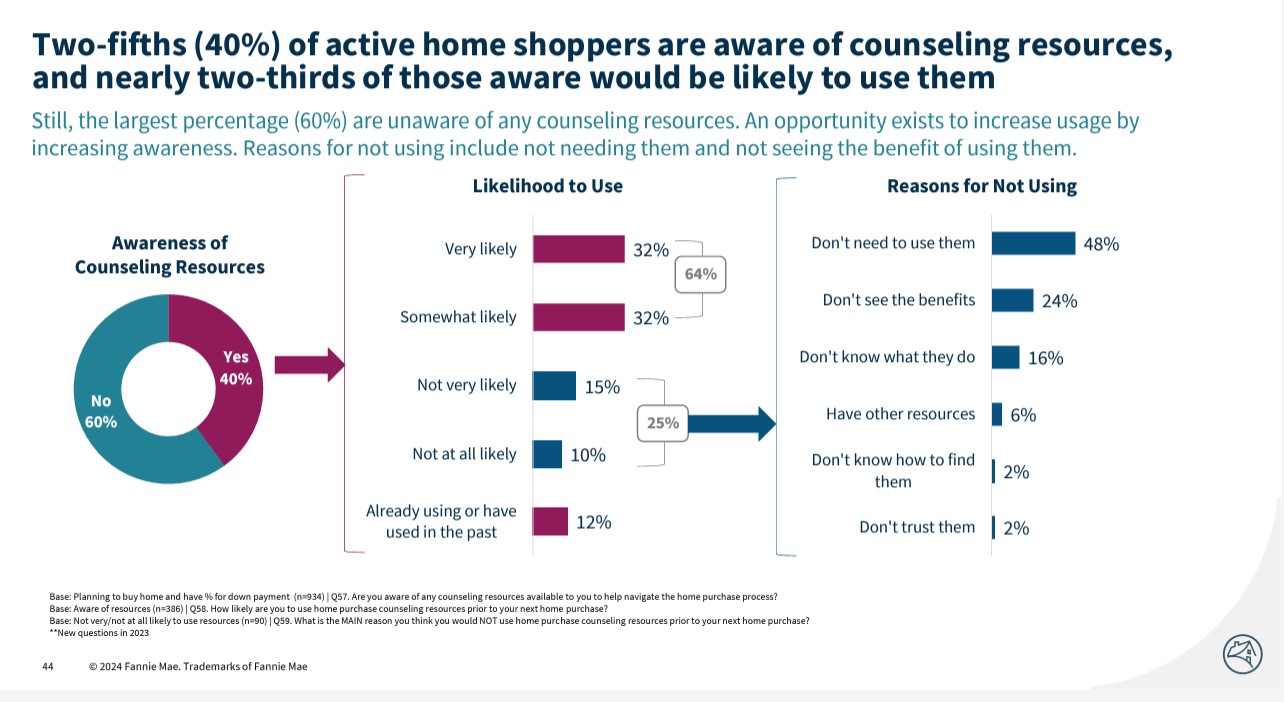

Four in ten are aware of counseling services available to assist them with the home mortgage process. Of that number, 63% say they would likely use those services.

Fannie Mae’s own resources include—

- Affordable mortgage options like HomeReady® Mortgage,

- Rent payment records to help qualify for a mortgage

- HomeView® first-time homebuyer course

- Various calculators and checklists for financial planning

The findings shared in Fannie Mae’s report provide valuable intel on the gaps in consumer knowledge of the homebuying process and their chances of qualifying for a mortgage.

The more conversations you have with home buyers in your area, the more likely you are to be aware of the knowledge gaps among those actively shopping for homes. Use that, along with the data in this report, to close those gaps and make your clients the best-informed homebuyers (and homeowners) in your market.

Because despite housing affordability challenges, 74% of the consumers in Fannie Mae’s 2023 study—including 43% of renters—plan to buy a home on their next move.

More than that, a full quarter (25%) are actively considering buying a home at some point in the next three years. Yet 30% of that quarter currently has $0 saved for a down payment.

So, providing reliable information on down-payment assistance programs and low down payment options could be the difference between those homebuyers making good on their homeownership plans and their having to save for another (several) years before they become homeowners.

See the full report for more information.

- BAM")