Key Details:

- The May Spotlight in Freddie Mac’s latest U.S. Economic, Housing and Mortgage Market Outlook focuses on mortgage rate dispersion by generation to reveal which generations are most likely to drive purchase and refinance activity in the months ahead.

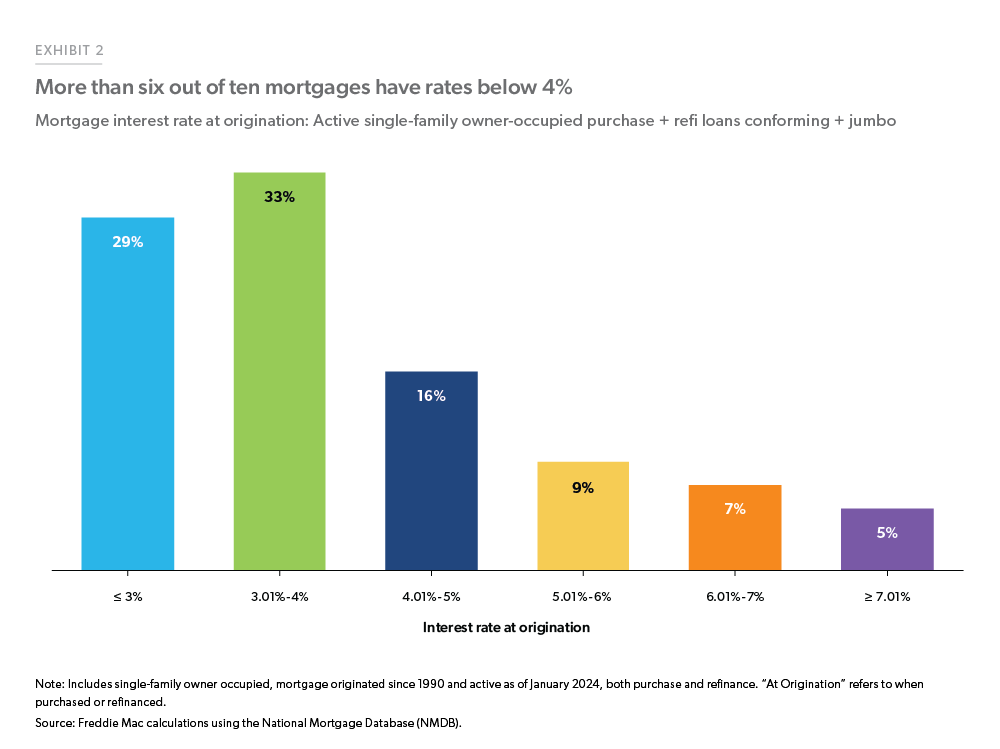

- More than 60% of outstanding mortgage loans have rates below 4%. Gen X and Millennials have the lowest average locked-in rates at 4.0% while Gen Z has the highest at 4.9%.

- Even with their low average rates, 4-5% of Millennials and Gen X have rates above 7%.

According to Freddie Mac’s latest Outlook report, more than 60% of all outstanding mortgages have rates below 4%.

Put another way, according to a previous analysis, homeowners with a fixed mortgage rate have an average locked-in savings of $66,000 per household over the life of the loan. Selling right now would mean giving up those savings.

For some generations, the loss would be greater. But some of those with the lowest locked-in rates are defying today’s average and moving anyway.

The May Spotlight of Freddie Mac’s report highlights the mortgage rate dispersion across generations, how each is responding to today’s rates, and how that’s likely to impact the housing market over the coming months.

The main focal points:

- Which generations have the highest and lowest rates locked in

- Which generations are best positioned or most likely to refinance if and when rates drop

- Which generation is most likely to impact the purchase market despite their low rates

According to Freddie Mac’s Primary Mortgage Market Survey, the average 30-year fixed mortgage rate is again over 7%. Mortgage News Daily puts the current average at 7.17%.

Rates at this level are causing current homeowners—namely those with historically low rates locked-in—to hold off on selling, resulting in lower existing home supply. Many of today’s homeowners secured rates averaging 3.20% in 2020 and 3.06% in 2021.

Rates above 7% also worsen affordability challenges for prospective buyers, especially those finding it harder than ever to save enough for a down payment.

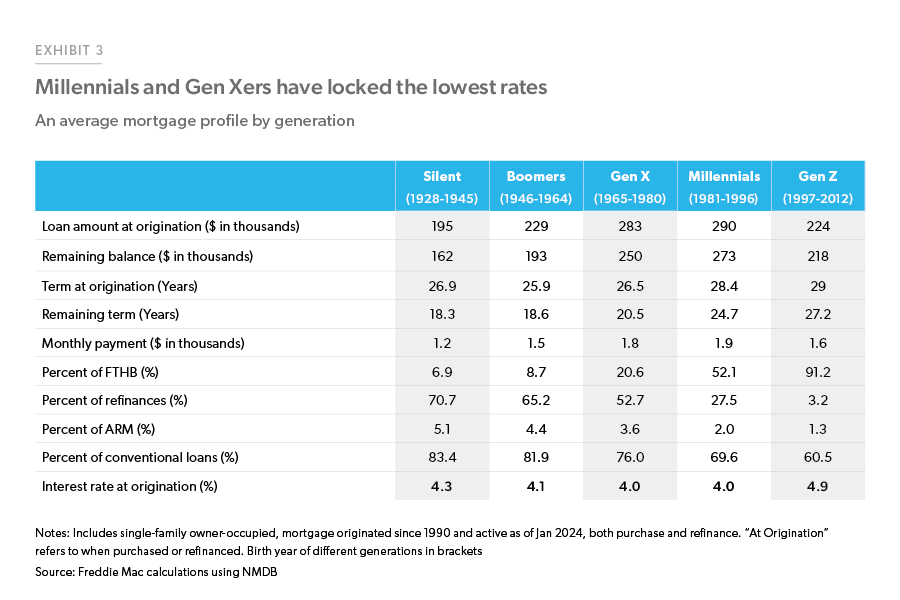

The typical mortgage situation looks different for each generation, based on—

- Current locked-in mortgage rates

- Average loan amount

- Remaining balances/terms

According to Freddie Mac’s analysis of the borrower-level National Mortgage Database—covering single-family owner-occupied home purchase and refinance loans originated since 1990 and still active as of January 2024—

- Millennials are in the lead for average loan amount and remaining balance, with an average remaining loan term of 25 years

- Baby Boomers and Silent Generation homeowners still have over 18 years in remaining loan term, mainly due to refinancing at record-low rates in recent years

- More than 90% of Gen Z are first-time homebuyers

- ARM rates are primarily concentrated among the Silent and Boomer generations, with the the majority of homebuyers across all generations opting for conventional loans

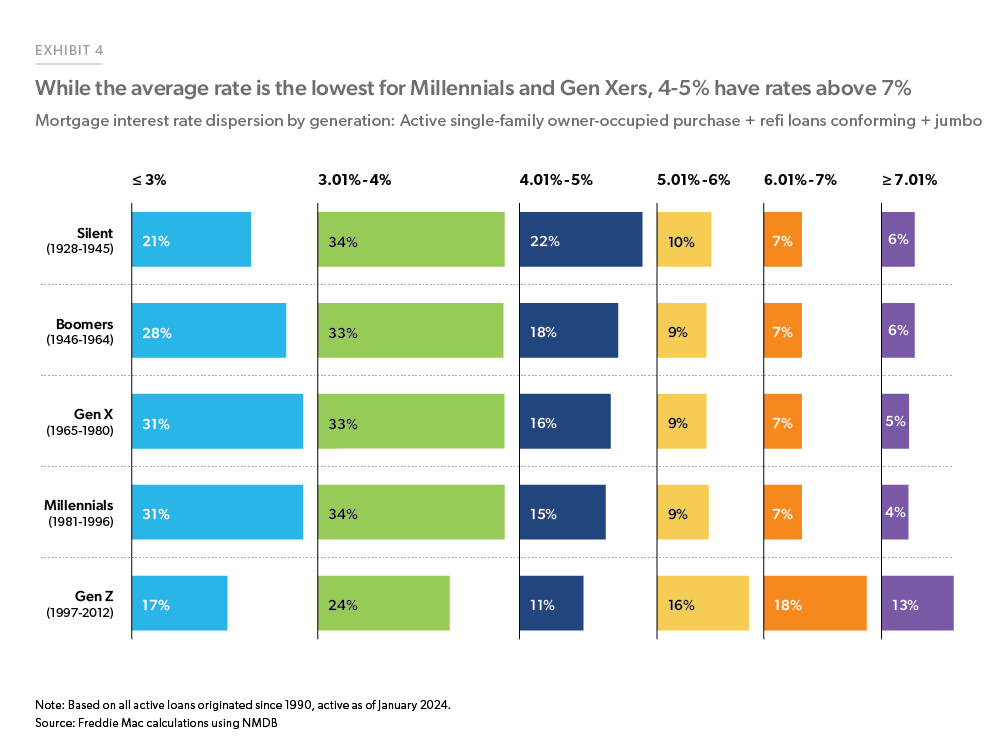

Millennials and Gen Xers currently have the lowest average locked-in mortgage rates at 4.0%, while Gen Z has the highest at 4.9%.

Where Millennials and Gen Xers differ is the types of loans driving those lower rates:

- Purchase rates for Millennials

- Refinance rates for Gen X

According to Freddie’s NMDB data analysis, 37% of Millennial borrowers’ home purchases were made in 2020 and 2021, when rates were historically low. One-quarter of Gen X borrowers’ home purchases were made during the same period, but Gen X homeowners took advantage of those low rates to refinance their existing loans.

Even with their lower average rates, 4-5% of both Millennials and Gen Xers have rates over 7%.

According to Freddie’s NMDB data analysis, 37% of Millennial borrowers’ home purchases were made in 2020 and 2021, when rates were historically low. One-quarter of Gen X borrowers’ home purchases were made during the same period, but Gen X homeowners took advantage of those low rates to refinance their existing loans.

Even with their lower average rates, 4-5% of both Millennials and Gen Xers have rates over 7%.

Gen Z has higher rates locked in because they started buying homes when rates were higher. More than six out of ten (62%) started buying homes in 2022 and 2023 when rates were averaging 4.9% and 6.7%, respectively.

Based on those average mortgage rates, Gen Z leads other generations for refinance potential, with 13% of these borrowers having rates above 7%. But since Gen Z represents a fraction of total borrowers, that 13% accounts for a small share of potential refi customers.

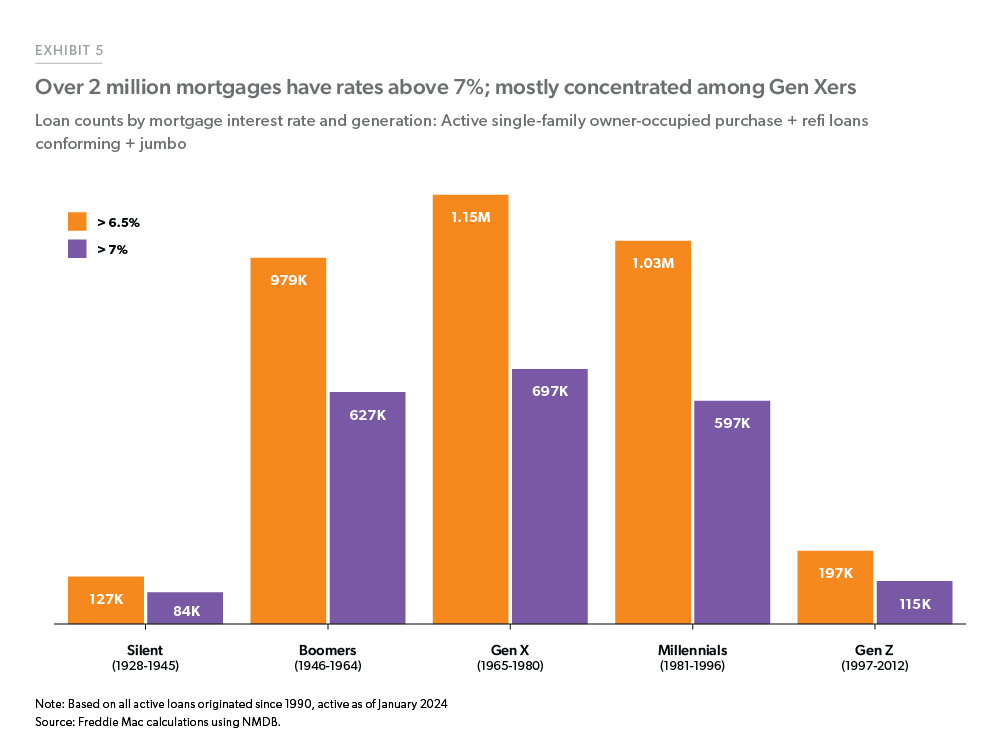

The data on rate dispersion shows a higher potential for refinance activity among older generations—and particularly Gen Xers and Millennials. But that potential is highest among Gen Xers, as nearly 700,000 Gen X borrowers have rates above 7%.

While the Millennial homeownership rate is lower than that of Baby Boomers and Gen Xers, Millennials are still the largest population cohort. So, that 4-5% of Millennials with rates above 7% still represents a substantial number of borrowers with higher average rates.

Looking at all generations combined, more than two million borrowers have rates higher than 7%, and over 1.2 million of those are Millennial and Gen X borrowers.

If rates drop faster than Fannie Mae’s recent update would suggest and fall below 6.5%, an additional 1.4 million borrowers—for a total of more than 3.4 million—will have rates higher than 6.5% locked in—primarily among Gen Xers who are more likely to refinance.

Gen Xers are less likely to move due to their low locked-in rates and proximity to retirement.

Millennials–-and particularly younger Millennials—are more prone to changes that require them to relocate, whether to pursue a career opportunity or to upgrade to a larger home.

According to the American Community Survey, when the average mortgage rate was 5.3% in 2022, 12% of Millennial homeowners still relocated, while just 3.8% of Baby Boomers and 5.5% of Gen Xers did the same.

So, it makes sense that today, with rates above 7%, Gen Xers and Boomers would be more likely to stay put and keep their low rates, while Millennial homeowners are more likely than other generations to make a move (for personal or professional reasons) despite less than optimal market conditions.

Freddie Mac’s analysis suggests Millennials will be the biggest supporter of the purchase market. And if and when rates drop, Gen X homeowners will be the heroes of the refinance market.

That said, mortgage rates are not the only factor determining market activity across generations. Home prices are and will continue to influence homebuyer and homeowner decisions in the months ahead, and steady price growth could slow lower for longer.

- BAM")