Key Details:

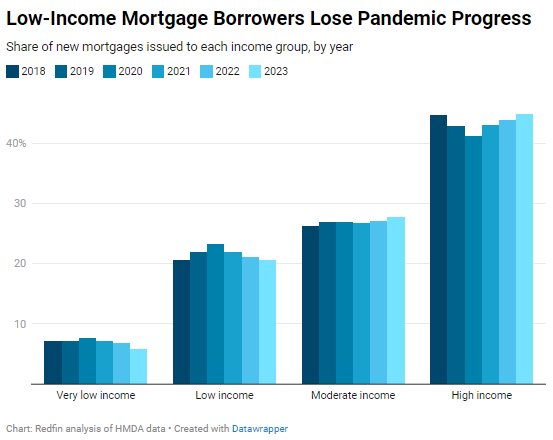

- A new Redfin report shows the share of new mortgages issued in 2023 to low-income homebuyers dropped from 23.2% in 2020 to 20.6% in 2023.

- This brings the share of mortgages back down to where it was in 2018 and erases the progress made during the pandemic.

Four years ago, in 2020, 23.2% of new mortgages were for low-income homebuyers in the U.S. Fast forward to 2023, and that share dropped to 20.6%, returning to 2018 levels.

That’s according to a new Redfin report, which sheds light on the reasons low-income households have lost the progress they made during the pandemic with regards to homebuying.

First of all, let’s get clear on the income categories Redfin uses for its research, based on median household income for those who purchased homes in 2023:

- Very-low-income households: $41,000

- Low-income households: $64,000

- Moderate-income households: $96,000

- High-income households: $172,000

Overall, the estimated median household income was about $84,000 in 2023.

Byron reviewed Redfin’s report on Tuesday’s Hot Sheet.

Data for the report is based on Redfin’s analysis of Home Mortgage Disclosure Act (HMDA) data on purchases of primary homes. It does not include purchases of second homes or investment properties.

Pre-pandemic, pandemic, and post-pandemic mortgage shares across income levels

Very-low-income Americans also lost what progress previously made in buying homes during the pandemic; the share of new mortgages issued to this demographic dropped from 7.7% in 2020 to just under 6% in 2023—even less than their share in 2018 (7.1%).

Meanwhile, higher-income homebuyers are picking up the share of mortgages lost by lower-income households. Their share dipped in 2020 to a low of 41.2% but increased to 44.8% in 2023, bringing it back up to nearly what it was in 2018.

Unlike the peaks and valleys for low- and high-income households, moderate-income buyers saw little change in their share of new mortgages over the past six years. Despite higher housing costs, their share increased slightly from 2018 to 2019, held steady in 2020, dipped slightly in 2021, rallied in 2022, and increased still more in 2023.

On the whole, though, the losses in market share for low-income households are understandable considering rents are currently more affordable than mortgage payments in many U.S. markets.

Housing affordability dropped to a record low in 2023

Thanks to a combination of high home prices and elevated mortgage rates, housing affordability reached an all-time low in 2023. And it hasn’t improved during the first quarter of 2024.

- Home Prices: Today’s median home sale price is about $420,000—up 5% from a year ago. That’s nearly 40% higher compared to the start of the pandemic (March 2020) and almost 50% higher compared to March 2019.

- Mortgage Rates: Today’s average 30-year fixed mortgage rate is at about 7.25%, up from 6.43% one year ago and more than twice the record low of 2.65% reached in 2021. It’s also significantly higher than the 4% and 5% rates of 2018 and 2019.

- Monthly Payments: The monthly mortgage payment for the typical homebuyer reached a record-high $2,886, up 13% year over year—compared to a little over $1,500 in both March 2020 and March 2019.

- Down Payments: The typical down payment for a buyer putting down 20% is $84,000—up from the previous year’s $80,200 and even further removed from the $60,800 in March 2020 and $56,800 in March 2019.

While the U.S. economy and labor market remain strong and wages have increased, the costs of buying a home have grown much faster. Hourly wages have grown about 5% from 2022 to 2023 while monthly housing costs have grown year over year by 15%.

That gap has an outsized impact on lower-income homebuyers on at least two fronts:

- Down payment—Lower-income buyers are less likely to have money saved for even a 3% down payment, let alone 10% or 20%

- Monthly payment—A larger share of their household income goes toward record-high housing costs every month

There was a sweet spot in 2020 when mortgage rates were ultra low and home prices had yet to skyrocket, allowing some lower-income Americans to break into the housing market. But somewhat ironically, the continued strength of the economy has made it harder to afford a home and widened the real-estate wealth gap between rich and poor Americans. The Fed’s interest-rate hikes, meant to help cool inflation and slow a hot economy, have pushed mortgage rates to near their highest level in more than two decades. That’s on top of home prices, which skyrocketed during the pandemic buying boom and have stayed high due to a shortage of homes for sale.

- BAM")