Key Details:

- A new Redfin report shows a housing market poised to finish the year with about 4.1 million home sales nationwide—the fewest since the housing bubble burst in 2008.

- High mortgage rates and low inventory are making it harder than ever for buyers to afford a home.

- That said, buyers and sellers are still transacting, and the potential to earn is still high for skilled and motivated real estate professionals.

With the 30-year fixed topping 8% as of Wednesday, October 18th, Redfin economists expect the year 2023 to end with a nationwide total of around 4.1 million existing home sales—the lowest number since the housing bubble burst in 2008.

That’s according to a new Redfin report that predicts this will be the slowest year for home sales since the Great Recession, thanks to a one-two punch of high mortgage rates and low inventory.

Buyers have been in a bind all year. High mortgage rates and still-high prices are making it harder than ever to afford a home, shutting many young people out of homeownership and causing homeowners to reevaluate whether 2023 is the right time to move. Mortgage rates are staying high longer than anticipated, keeping away everyone except those who need to move and pushing our sales projection for the year down to a 15-year low. The last time home sales were this low was during the Great Recession. At that time, tough economic conditions and slow demand pushed home prices down 30% year over year in some parts of the country, creating an opportunity for first-timers to snatch up starter homes–but this time, there’s no deal to be had.

What Redfin agents are saying

Given the low inventory and high housing costs, Redfin agents are recommending that buyers consider newly constructed homes. Sales of new construction are holding up better than sales of existing homes.

For one, builders aren’t locked into low mortgage rates—unlike the vast majority of homeowners. Also, they’re often more motivated to close a deal and more likely to offer concessions to sweeten the pot.

According to Redfin’s data, sales of newly constructed homes rose 1.5% year over year in September as prices fell 4%.

Key housing market indicators

Here are the latest numbers for key housing market indicators, starting with those related to homebuyer demand and activity:

- The 30-Year fixed mortgage rate reached 8.03% on October 19th—the highest level in 23 years. The weekly average also hit a 23-year high of 7.63% for the week ending October 19th.

- Mortgage purchase applications are down 6% from the prior week (ending October 12) and down 21% year over year, falling to their lowest level since 1995.

- Redfin’s Homebuyer Demand Index is down 6% month over month, falling to its lowest level in almost a year. It’s also down 6% year over year.

- Google searches on “homes for sale” are down 23% month over month (as of October 14).

- The median sale price is up 2.5% year over year to $369,250, partly because high mortgage rates were hampering price growth this time last year.

- The median asking price is up 5% year over year to $385,048—marking the biggest increase in a year.

- The median monthly mortgage payment for homebuyers went up 10% year over year $2,730 at a 7.57% mortgage rate (Freddie Mac’s average rate for the week ending October 12), sitting just $8 shy of the record high set two weeks earlier.

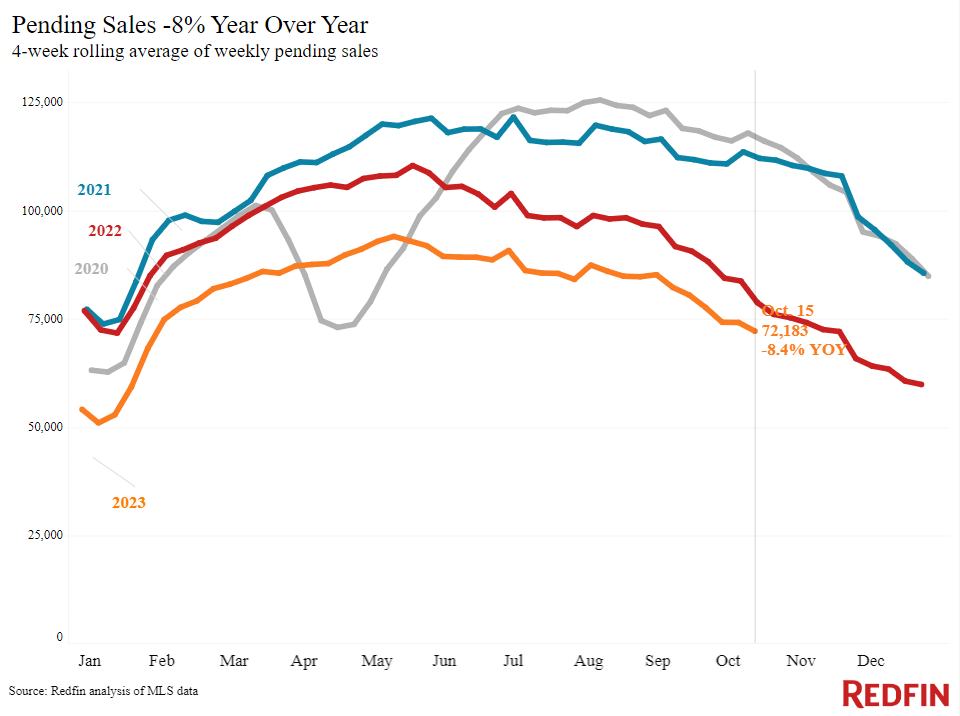

- Pending sales dropped 8.4% year over year to 72,183, marking the smallest annual decline since May 2022, partly because of a sharp drop in pending sales this time last year.

- New listings fell 1.9% to 81,497—the smallest drop since July 2022. Active listings fell 13.6% to 829,629.

- Months of supply are up 0.2 points to 3.4 months, reaching their highest level since February. For context, four or five months of supply is considered balanced; anything lower points to seller’s market conditions.

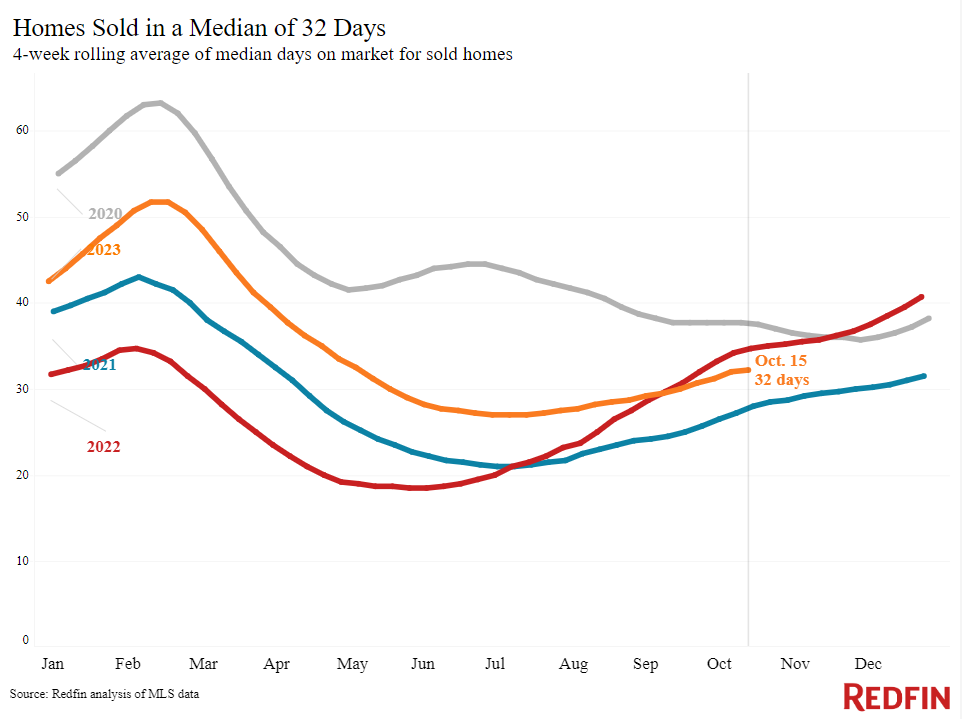

- Median days on market dropped year over year by three days to 32. And the share of homes that went off market in two weeks went up from 36% one year ago to 39.1%.

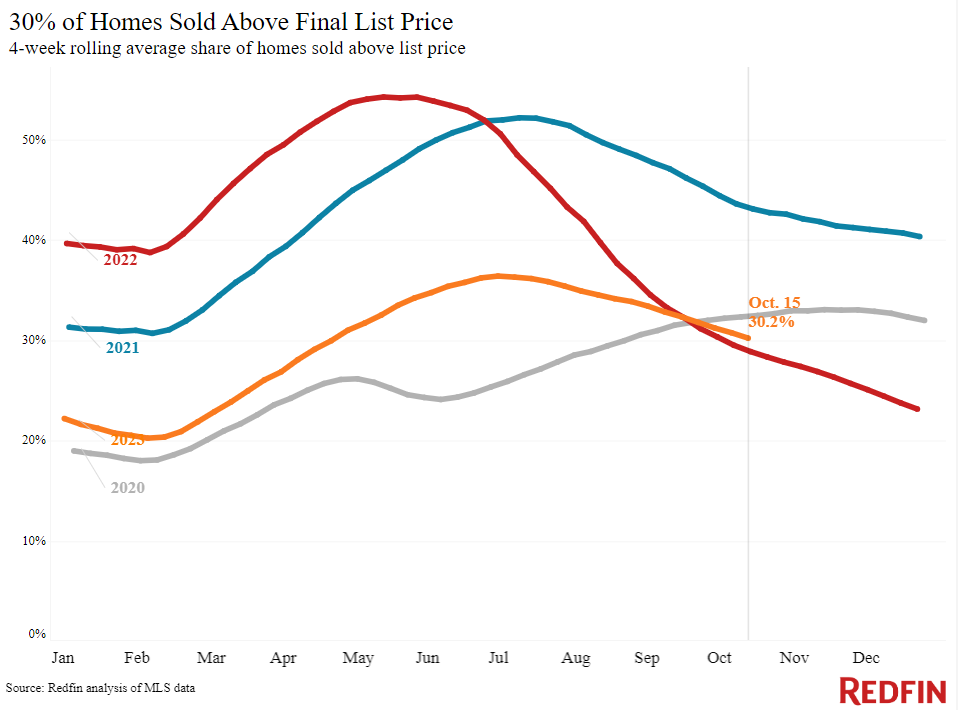

- The share of homes that sold above the final list price went up year over year from 29% to 30.2%. The share of homes with a price drop remained unchanged at 6.7%.

- The average sale-to-list-price ratio rose 0.3% year over year to 99.2%.

Read the full report for more information, including charts and methodology.

Though fewer homes are selling, potential to earn is still high

Hot Sheet host Byron Lazine has been telling us for weeks now that 8% rates were coming. And now that they’re here, it’s fair to wonder just how high they’ll go before they head back down again. Because historically, rates do come down—eventually.

But despite how daunting those rates are for many buyers, not all are compelled to wait on the sidelines for affordability to improve. Buyers are still buying, and sellers are still selling. Skilled and committed real estate professionals are uniquely positioned to help them take advantage of every cost-saving option they have.

No buyer should have to go through the home buying process alone. And by the same token, no agent should try to succeed in this industry by going it alone.

Byron Lazine goes into that in the following video, where he talks about how this market still has high earning potential for agents who know how to navigate it.

Nobody’s done everything—or anything, rather—great alone.

- BAM")