Key Details:

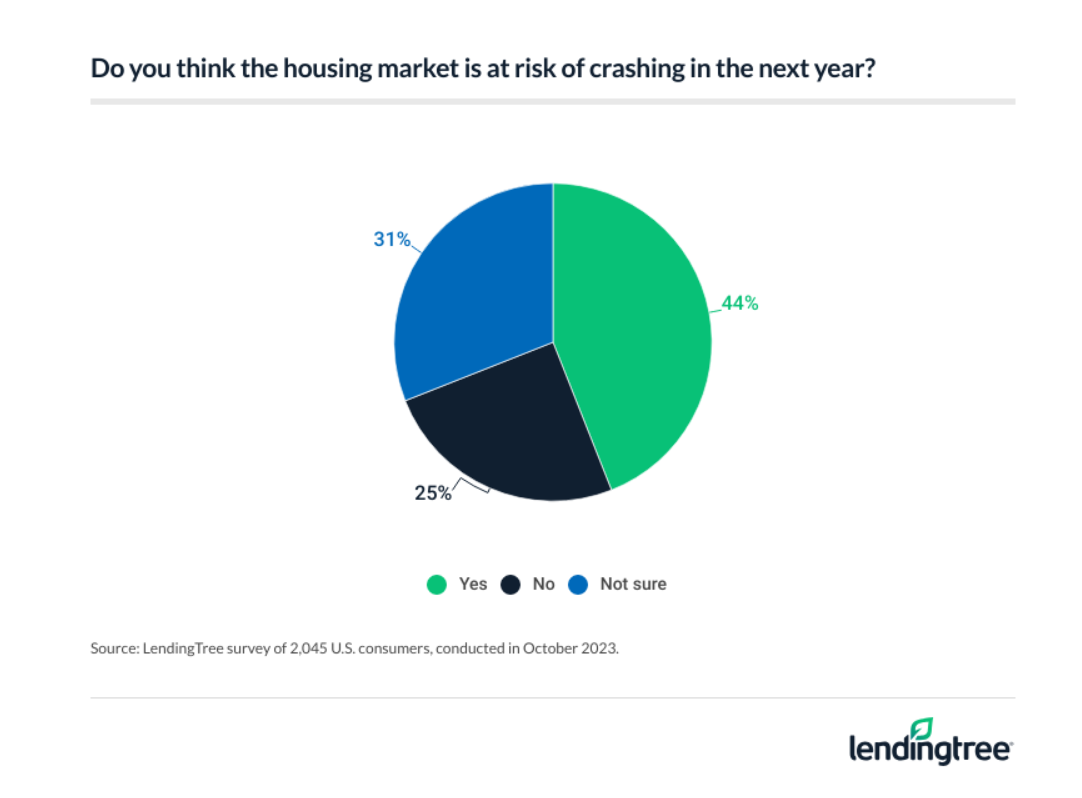

- A new LendingTree survey of over 2,000 U.S. consumers shows 44% of Americans believe the housing market could crash in the next year. Another 31% are unsure.

- What’s more surprising (or not) is that 35% overall are hoping for a crash.

LendingTree conducted a survey of more than 2,000 U.S. consumers to gauge their confidence in the housing market. According to their results, 44% of Americans believe the market is at risk of a crash over the next 12 months. Another 31% are uncertain.

The real kicker is that an average of 35% are actually hoping for a crash, with a significant share of buyers, in particular, seeing that as their only hope of becoming homeowners.

Here’s what the survey revealed—and what it could mean for your clients.

More than two-fifths of Americans (44%) expect a housing market crash

Breaking it down by generation, at 52%, millennials (ages 27-42) are most likely to expect a market crash is likely within the next year. At the other end of that spectrum, only 30% of baby boomers (ages 59-77) have the same expectation.

After millennials come Gen Zers (ages 18-26) at 48%, followed by 42% of Gen X (43-58).

By parental status:

- 55% of parents with children younger than 18 expect a market crash, followed by

- 39% of those without children, and

- 35% of those with children aged 18 or older

Also, homeowners were just a little more likely (46%) than nonhomeowners (41%) to think a housing crash is likely in the next 12 months.

Over one-third of Americans want the housing market to crash

More than a third of Americans are actually hoping the housing market takes a dive in the next year—with 36% of homeowners and 35% of Americans overall indicating as much.

While more than half (51%) of homeowners aren’t keen on the idea, 15% say they want a housing crash to lower their property taxes and another 15% say it could improve market stability in the long run.

Almost a third of nonhomeowners (32%) see a housing crash as the only way they’ll ever be able to afford a home. That share is greater among Gen Zers (39%) and millennials who are not homeowners (38%).

Overall, 35% of Americans are hoping for a housing market crash. And that share goes up significantly among Gen Zers (53%), millennials (46%), and those with children under the age of 18 (46%).

On the flipside, only 18% of boomers want the housing market to crash, along with 22% of those with children older than 18.

Source: LendingTree

To LendingTree senior economist Jacob Channel, it’s hardly surprising so many Americans want to see the housing market crash. It’s also doubtful that many of those expressing this desire fully understand what it would mean.

Right now, home prices are high, as are mortgage rates. With that in mind, I can understand why some might wish for a housing crash that brings lower prices. Unfortunately, if the national housing market were to crash, odds are that it would bring down the rest of the economy with it.

Case in point, when the housing market crashed in 2008, it contributed to the largest global recession since World War II. Housing prices did drop, but lending standards also tightened, and millions of Americans lost their jobs. So, it actually became harder for most to buy a home.

It’s not impossible for home prices to fall and make a given housing market more affordable. It’s also not necessarily impossible for the housing market to outright crash next year while the rest of the economy remains relatively OK (though it’s very unlikely). But if you’re hoping that the housing market will crash and make it easier for you to buy a house, you’ll probably be disappointed. Not only does data indicate the odds of a housing crash in the next few years are slim, the past shows that when the market crashes, it tends to hurt more people than it helps.

What consumers expect from mortgage rates

While mortgage rates have dropped significantly from 8%, most Americans (79%) expect them to increase for at least another year, while over half (53%) are worried rates will remain high.

More than a quarter of Americans believe they’ll climb back up to 8% or higher one year from now. On the other hand,

- Nearly one in five (19%) believe rates will be between 5.00% and 5.99%.

- 15% believe they’ll range from 6.00% to 6.99%.

- 13% are expecting rates from 7.00% to 7.99%.

Americans most likely to worry about mortgage rates include—

- Those with children under the age of 18 (61%)

- Those with household incomes of $75,000 to $99,999 (60%)

- Millennials (59%)

Also, women (56%) tend to worry more about high interest rates than men (49%).

The most optimistic generation is Gen Z, with 21% of Zoomers believing rates will fall between 5.00% and 5.99% in a year’s time. Baby boomers take the opposite view, with 21% expecting rates between 7.00% and 7.99%.

While it’s difficult to say exactly what rates we should expect in the next year (or further out), Channel believes there’s a good chance rates will go down next year.

Across the board, interest rates have risen dramatically since the start of 2022, and mortgage rates are no exception. Fortunately, just because rates have risen over the last two years doesn’t mean they’ll continue to climb in 2024. On the contrary, there are encouraging signs, like cooling inflation, that could help bring down rates next year. If inflation continues to cool and the Fed starts cutting rates in 2024 (as they appear poised to do), rates should fall. They won’t plummet, but they might end up closer to 6.00% or 7.00% than 8.00% or higher.

The lock-in effect keeps many homeowners from moving

Among the homeowners responding to the LendingTree survey, half (50%) say their current mortgage rate is keeping them right where they are.

Three quarters (75%) say they’re not sure they’ll ever see mortgage rates as low as they were in 2020 and 2021. And just over one in ten homeowners (11%) don’t expect they’ll ever be able to buy a home again.

Among the homeowners responding to the LendingTree survey, half (50%) say their current mortgage rate is keeping them right where they are.

Three quarters (75%) say they’re not sure they’ll ever see mortgage rates as low as they were in 2020 and 2021. And just over one in ten homeowners (11%) don’t expect they’ll ever be able to buy a home again.

Channel would agree with consumers who believe a return to rates as low as we saw in 2020 and 2021 is unlikely.

There’s a chance that they could fall back to their 2020 and 2021 levels again at some point, just as there’s a chance they’ll spike back up to their early 1980s levels. From where things stand, I’d say that either scenario is more unlikely than not.

Biggest housing market worries

Homeowners and homebuyers alike are concerned about home prices—for opposite reasons.

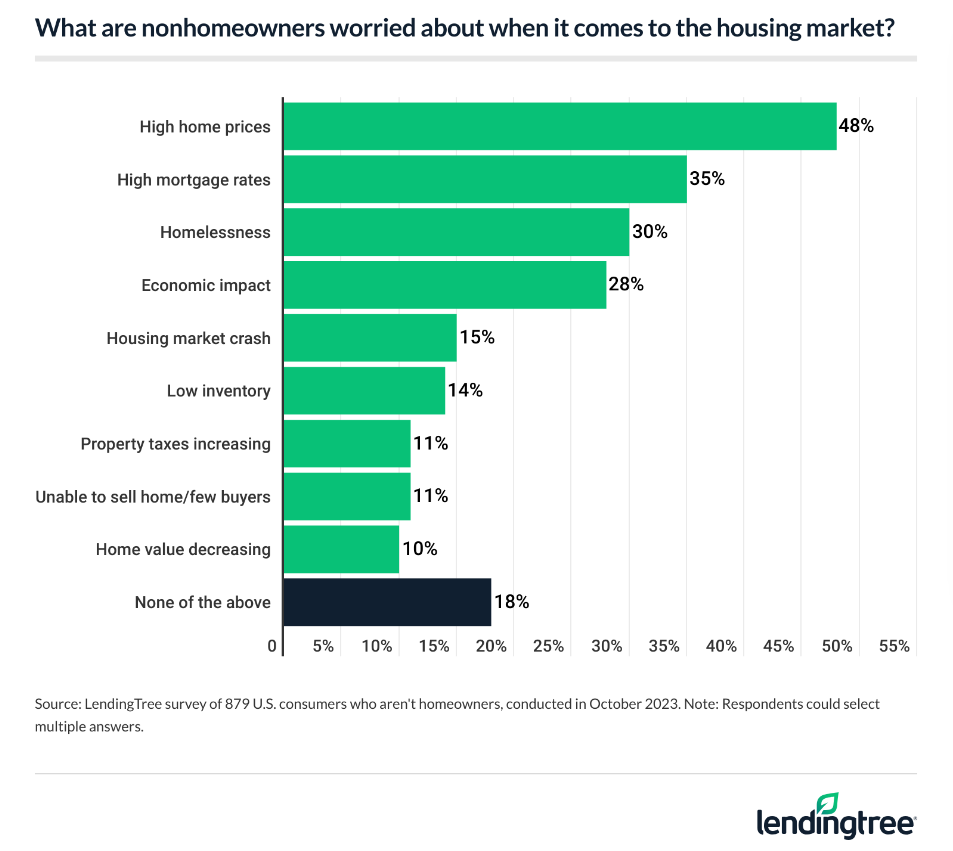

Among nonhomeowners, their number one housing market concern is high home prices (48%), followed by high mortgage rates (35%) and homelessness (30%).

The top housing market concern for homeowners is a drop in home values (38%). But their second and third-ranking concerns mirror those of potential buyers:

- 37% worry about high mortgage rates

- 34% worry about high home prices (when it’s time to buy their next home)

Across the board, 62% of Americans surveyed believe home prices will rise in the next year. Of these—

- 66% believe they’ll rise by 5% or more

- 48% expect an increase between 5% and 9.99%

Takeaways for real estate agents

When you’re having conversations with potential buyers, maybe you’ve already had to develop a script to answer the question, “Is the housing market going to crash?” or even “Should I wait on buying a home until the market crashes?”

Housing affordability challenges will likely remain for some time, though it’s difficult to say for how long. As 2024 housing market predictions start coming in from industry economists, we’re seeing a common theme—next year could likely bring some relief to homebuyers. But there’s little (if any) reason to think the housing market will crash in the next year and suddenly make it far easier for buyers to become homeowners.

Because housing markets don’t crash in a vacuum.

You’ll also want to encourage your clients to focus on the present and not on what could happen.

An ‘ideal’ time to buy a house may never come, and if you’re in a good position to buy now, doing so might be a good idea. After all, you could miss plenty of great opportunities if you’re too worried about the future to act in the present.

Another key piece of advice Channel offers consumers applies to real estate agents as well: Keep informed!

The housing market is constantly changing and what’s going on can vary significantly from place to place. Because of this, you’ll want to try to stay on top of what’s going on.

The best way to do this is to be educating yourself on a daily basis. Stay on top of housing market developments by tuning in for the daily Hot Sheet. And keep yourself informed on what’s going on in the economy, with the Fed, unemployment, and everything that impacts housing by watching (or listening to) the Knowledge Brokers Podcast every Friday.

And if you’re not already a member, sign up for BAMx to take advantage of our growing library of online courses and livestreams, as well as the most knowledgeable and supportive Facebook group for real estate agents.

- BAM")