Key Details:

- In its report, “The 9th National Risk Assessment: The Insurance Issue,” First Street Foundation shared recent data and projections on the impact of climate-related disasters on home valuation, insurance premiums, and insurability in high-risk areas.

- Recent disaster data for California shows a 270% surge in the cost of wildfires and a 335% increase in the number of structures destroyed by wildfires since 2009.

As climate change-related disasters happen more frequently and do more damage, insurance companies have adapted by either limiting coverage or withdrawing completely from high-risk areas—driving up the cost of homes and leaving homeowners vulnerable.

While both politics and math have a role to play in those decisions, recent disaster data for California shows a 270% increase in the cost of wildfires and a 335% increase in the number of structures destroyed by wildfires since 2009.

Given growing concerns regarding the cost, affordability, and insurability of many areas of the country due to the increasing risk of climate-related disasters,

First Street Foundation launched Version 2 of its Wildfire Model (FSF-WFM) to measure and estimate the costs associated with wildfires. Their report, “The 9th National Risk Assessment: The Insurance Issue” shares their latest findings and projections.

Climate change-related disasters are more frequent and more destructive

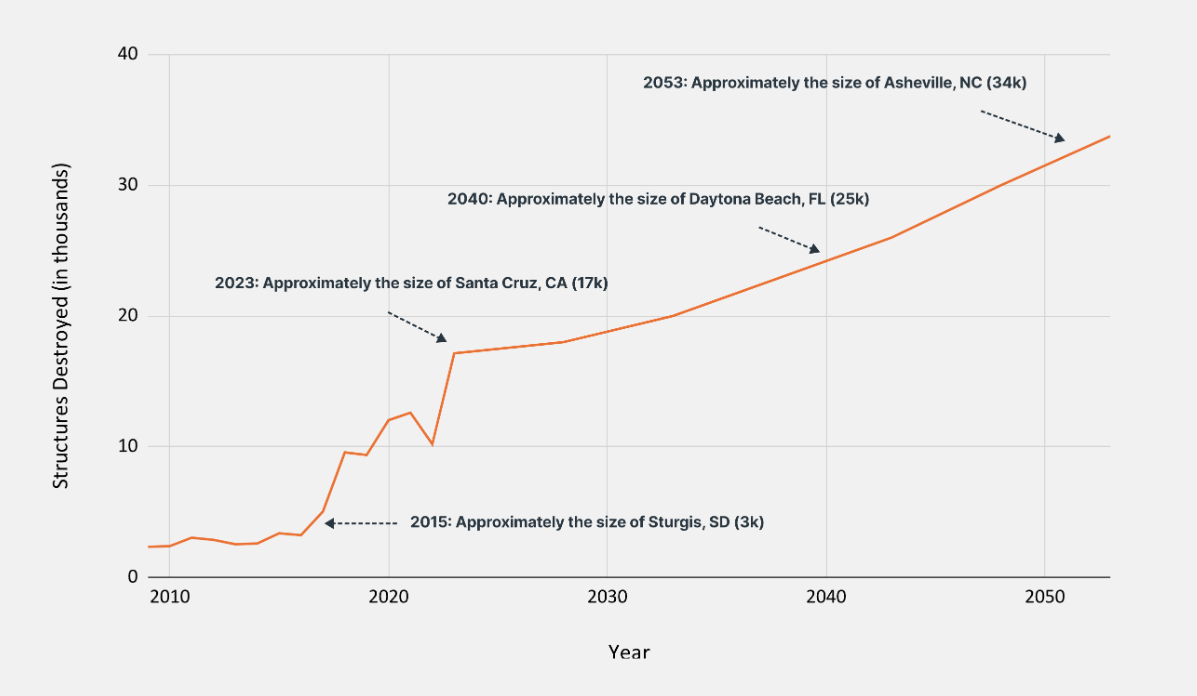

As shown in the report, nationally, wildfire risk estimated from the FSF-WFM is associated with an average of 17,139 structures destroyed per year in the current environment.

Fast forward 30 years, and the Wildfire Model estimates a doubling of that figure to an average 33,753 structures per year by 2053. For context, that means in 30 years, a city the size of Asheville, NC (with about 34,000 buildings) will be destroyed by wildfires every year.

The report also estimates a near doubling in damages from wildfires over 30 years from the current average of $14 billion to around $24 billion by 2053 (in today’s dollars).

These numbers are similar to the 23.9 million structures identified as at risk from damaging winds and the 12 million identified as structures at significant risk of flooding but outside the FEMA Special Flood Hazard Area (SFHA).

We’ve reached the point where certain areas of the country—because of their high climate risk and the annual associated costs—have become money pits for insurance companies.

Insurance companies are withdrawing from areas with high climate risk

For decades, homeowners and business owners have relied on insurance as a risk transfer mechanism. But as the cost of climate hazards rises, insurance companies have had to raise their rates—dramatically, in some cases—to offset the financial toll.

In areas with high climate risk, insurance coverage at a rate deemed affordable for homeowners has become unsustainable.

The result? Well-known nationally-operated insurance companies are backing away from these areas and leaving homeowners with the state’s “insurer of last resort.”

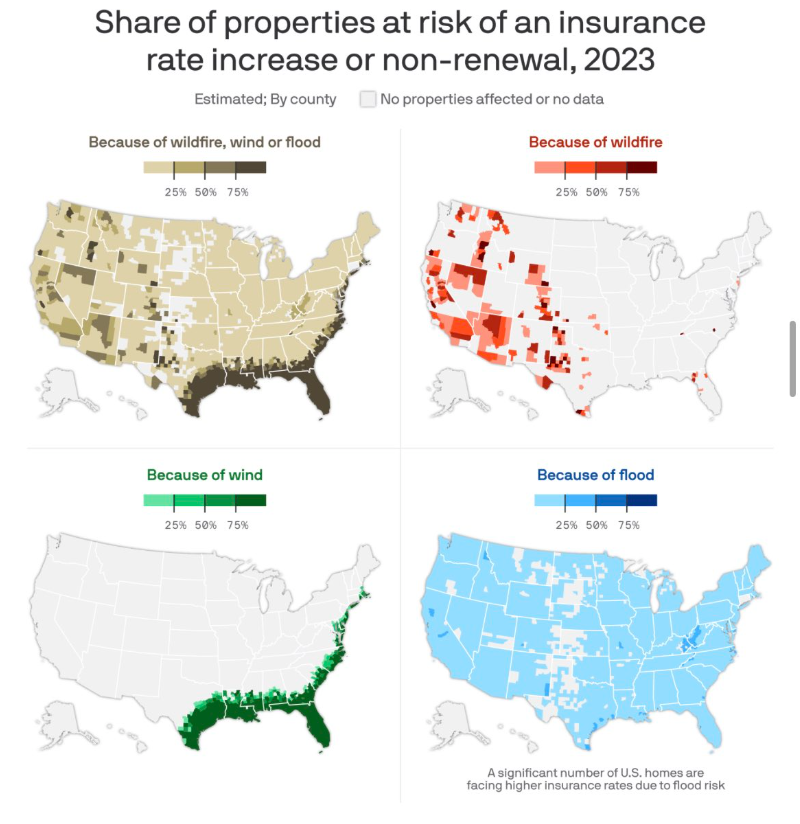

Results from the First Street Foundation Wildfire Model (FSF-WFM) show huge numbers of homes at risk of rising insurance rates and non-renewals thanks to the growing risk of climate change-related disasters:

- Wildfires for almost 4.4 million properties

- Wind-related damage or destruction for 23.9 million properties

- Flooding for 12 million properties not included in FEMA SFHAs

Lance Lambert shared the following graphic in a recent post on the X platform:

Those millions of homes across the country account for a significant share of the national real estate market. And it’s a subset for which we’ve only just begun to quantify the impact of climate risk on property valuation.

The climate-corrected valuation gap is not yet universally acknowledged. But insurance companies, by necessity, are ahead of the game.

When climate risk drives up financial risk for insurance companies, the increase in insurance payouts begins to outpace premium rate increases. The only way insurance companies can offset those risk increases is by raising rates.

But some states—most notably California, Florida, and Louisiana—have suppressed insurance price growth for years, ostensibly to protect consumers from out-of-control increases.

Unfortunately, with the growing cost of climate risk making insurance coverage at those limited rates unsustainable, the insurance industry is either limiting or completely withdrawing coverage in high-risk wildfire areas.

Homeowners in high-risk areas have two options

Homeowners in areas abandoned by private insurance companies now have two options to consider:

- Pay a much higher premium for far less coverage with the state’s “insurer of last resort”

- Decide not to insure their homes—and pay the price if/when disaster strikes

Either way, the cost of owning a home in these areas is growing at a significantly faster rate than homeowner incomes. And for those who can’t afford the much-higher premiums for much-lower coverage, all it takes is one disaster to leave them without their biggest asset.

Some homeowners will decide to forego insurance and hope for the best, simply because they can no longer afford the monthly premium. In any case, the cost of rising premiums is driving up the cost of homeownership in these areas, even as the risk of losing their investment goes up.

What can you do when private insurance companies give up on your area as “uninsurable,” leaving you with the state’s “insurer of last resort” as your only insurance option? You either come up with the money for whatever coverage you can get, or you roll the dice.

Homeowners who can no longer afford the available insurance option can either stay put and cling to blind optimism or sell as quickly as they can and move to a lower-risk area.

Meanwhile, the more people leave these areas, the more property values are likely to deflate, even as the cost of insuring those properties continues to grow.

Homeowners in the most at-risk portions of California are finding it nearly impossible to find affordable homeowner’s insurance. Recent data suggest that some of the most at-risk zip codes have seen an almost 800% increase in insurance policy non-renewals between 2015 and 2021.

California’s wildfire risk isn’t the only climate hazard leaving homeowners without affordable insurance. Over the past year, Louisiana’s “insurer of last resort,” Citizens Insurance Agency, raised homeownership insurance rates by 63% to offset the growing windstorm risk.

In Florida, the insurer of last resort for windstorm insurance has become the state’s largest insurer. Between 2016 and 2023, Policies in Force grew by 168% to over 1.3 million, with the Average Premium rising by 61% from about $2,000 to roughly $3,300.

Takeaways for real estate agents

Whether you’re helping people leave high-risk areas or move into them, do your research so you can give them as full a picture as possible of their situation and their opportunities.

And keep in mind that while a seller of yours may be keen to move out of a high-risk area, there are still buyers looking to move into those areas for other reasons.

Use that to your client’s advantage.

- BAM")