Key Details:

- ATTOM released its Q3 2023 U.S. Home Affordability Report showing affordability has continued to worsen, driving up the portion of average wages needed to cover major homeownership costs up to 35%, up from 21% in 2021 and the highest level since 2007.

- A new Redfin report shows the combined effect of rising home prices and mortgage rates around 7.5% has cooled buyer demand, causing an increase in the number of listings with price reductions.

New reports from ATTOM and Redfin show just how much housing affordability has worsened compared to a year ago. With home prices rising and mortgage rates hovering around 7.5%, the share of the average income needed to cover the cost of homeownership has climbed to 35%.

That’s according to ATTOM’s Q3 2023 U.S. Home Affordability Report, and it marks the highest share since 2007. According to standard lending practice, it’s also well over the 28% maximum affordable debt-to-income ratio—not to mention the 21% share recorded in 2021, just before mortgage rates started ratcheting up from historic lows.

ATTOM’s report shows median-priced homes are less affordable in Q3 2023, compared to historical averages, in 99% of U.S. counties with enough data to analyze.

Overall, homeownership has been getting tougher for the average U.S. wage earner over the past two years. This is the latest development of a growing trend with no end in sight.

In a recent interview with CNBC, Redfin CEO Glenn Kelman shared some of his perspective on the issue as it relates to Fed rate hikes.

The housing market is just taking a beating because affordability is at a four decade low. And so at some point we just need to catch a break from the Federal Reserve. And that doesn’t seem likely to happen in 2023.

The latest home price and interest rate hikes, combined with other forces, continue to drive up the cost of major homeownership expenses at a much faster rate than U.S. wages, worsening affordability and putting homeownership out of reach for more people.

The dynamics influencing the U.S. housing market appear to continuously work against everyday Americans, potentially to the point where they could start to have a significant impact on home prices. We clearly aren’t there yet, as the market keeps going up and the slowdown we saw last year looks more and more like a temporary lull. But with basic homeownership now soaking up more than a third of average pay, the stage is set for some potential buyers to be priced out, which would reduce demand and the upward pressure on prices. We will see how this shakes out as the peak 2023 buying season winds down.

Home prices are growing faster than wages in nearly half of the U.S.

From Q3 2022 to Q3 of this year, annual home price appreciation has outpaced weekly annualized wage increases in 272 (47%) of the 578 counties in ATTOM’s analysis.

Just last quarter—Q2 of 2023—wages were growing faster year over year than home prices, or shrinking less, in three-quarters of those same counties.

Counties where annual home price gains are outpacing wage increases by the largest margins:

- Cook County, (Chicago), IL

- San Diego County, CA

- Orange County, CA (outside Los Angeles)

- Miami-Dade County, FL

- King County (Seattle), WA

Counties where annual wage growth is outpacing—or declining less than—annual home price growth:

- Los Angeles County, CA)

- Harris County (Houston), TX

- Maricopa County (Phoenix), AZ

- Kings County (Brooklyn), NY

- Dallas County, TX

Homeownership takes up a larger portion of monthly income throughout the U.S.

The share of average local wages needed to cover major homeownership expenses increased year over year in 99% of the 578 counties in ATTOM’s analysis. It increased on a quarterly basis in 94% of them.

The typical cost of mortgage payments, property taxes, and insurance nationwide has surpassed $2,000 for the first time ever. It now takes up 34.6% of the average annual U.S. wage of $71,214. That’s up from 32.3% in Q2 2023 and 28.4% in Q3 2022. It’s also the highest recorded level since 2007.

That figure far exceeds the 28% lending guideline in 457 (or more than three-quarters) of the counties analyzed, assuming a 20% down payment. That’s up from roughly two-thirds of those counties one year ago and 44% of them two years ago.

This pattern really jumps out. While lenders will often push the 28 percent rule, especially if buyers have lots of financial resources outside of wages, we now are seeing fully three-quarters of markets around the country pushing the basic lending benchmark.

Regionally, homeownership costs continue to take up the largest portions of wages in Northeast and West markets.

The minimum annual income needed to pay the major homeownership costs on a median-priced U.S. home purchased in Q3 2023 has risen to more than $75,000 in 57% (330) of the 578 counties in ATTOM’s analysis.

Among those counties, 99% are less affordable in Q3 2023 compared to their historic affordability averages. That’s higher than the 96% from one year ago and well over the 48% in Q3 2021. Historical indexes have worsened from the previous quarter in 94% of those counties, driving the nationwide affordability index to its lowest point since 2007.

Only four counties (1%) are more affordable in Q3 2023 than their historic averages—down from 4% one year ago and well below the 52% in the third quarter of 2021.

Read the full ATTOM report for more, including methodology.

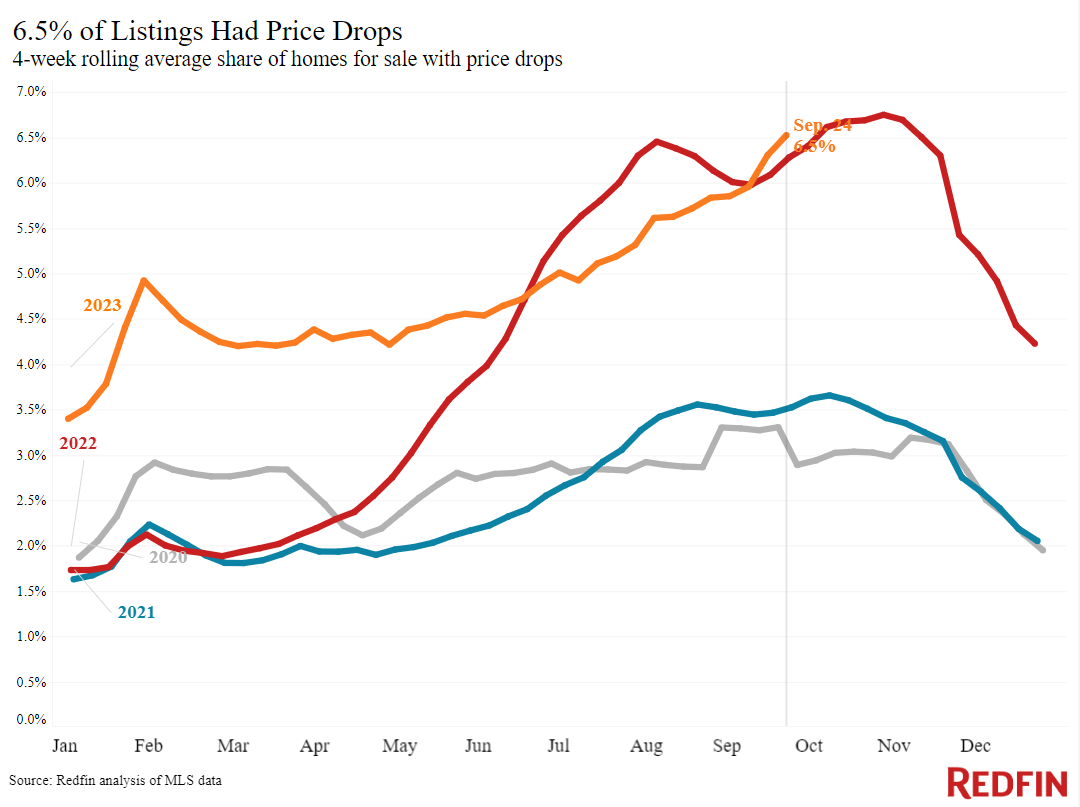

As affordability worsens, more sellers are reducing their home’s asking price

As declining affordability drives more buyers away from the market, more sellers are finding it necessary to reduce the asking price for their homes.

A new report from Redfin shows about one in five (6.5%) U.S. homes for sale had a price reduction during the four weeks ending September 24—up from 5.8% the previous month and marking a sharp monthly uptick compared to the same time period in years past.

Meanwhile, the median home sale price has increased 3% year over year, and the typical homebuyer’s monthly mortgage payment has reached a record high as rates remain elevated, reaching a two-decade peak on September 27.

One area where you can help sellers is by applying your knowledge of the local market to help them price their home just low enough to avoid having to reduce the price down the road to attract a buyer.

Motivated buyers are still out there, and total inventory is down 15% year over year, reducing available options. But monthly mortgage payments are at an all-time high.

Where you can help buyers is by negotiating with sellers, many of whom are open to making concessions. Those concessions could include—

- Paying for repairs

- Helping fund a mortgage rate buydown

- Paying closing costs

- Including newer major appliances

- Seller financing

Redfin’s report also highlighted an unseasonal uptick in new listings for September, giving buyers more options to choose from if sellers aren’t willing to be flexible.

Takeaways for real estate agents

Today’s affordability challenges make it all the more important for you, as a real estate agent, to be aware of all the options buyers have to help reduce the cost of buying (and keeping) a home.

Whether it’s creative financing or negotiating with sellers (or builders) for concessions, be the agent your client can count on to make homeownership a real and affordable possibility, especially for those who can’t afford to stay where they are.

- BAM")