Key Details:

- Freddie Mac’s latest outlook report spotlights the growing challenges facing first-time homebuyers, from historic lows in available housing to increased competition, with 30 renters for each available home for sale.

- Freddie Mac data highlights three headwinds facing future first-time buyers: supply, affordability, and tougher economic conditions, including higher unemployment.

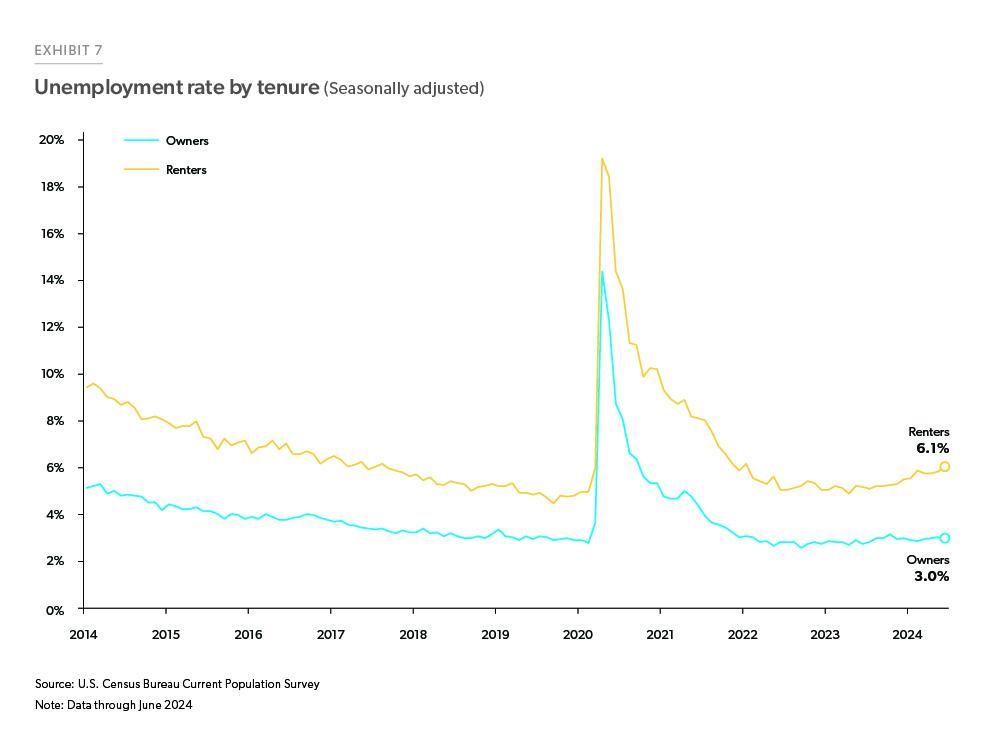

- The unemployment rate for renter households has grown from 5% to over 6% since 2023, while the rate for owner-occupied households has stayed relatively flat.

Freddie Mac’s latest market outlook report highlights the challenges faced by first-time homebuyers.

For one, the number of homes for sale for each renter household in the U.S. remains near historic lows. In fact, according to Freddie Mac’s report, there are currently about 30 renters per home for sale in the U.S.

That’s up from less than 10 renters per home for sale in 2006.

The reason for that goes back to the Great Recession, which significantly undermined new construction, slowing the pace of inventory growth and leading to a severe shortage.

As a result, not only do people looking to buy their first home have to navigate higher home prices and mortgage rates, but they also have to compete with a higher number of first-time buyers when making offers on available homes.

Freddie Mac’s October Spotlight focused on three first-time homebuyer trends:

- Their increasing role in overall housing demand

- Geographic preferences of first-time buyers

- Potential headwinds that could hinder first-time buyer activity in the near future

Renters’ Aspirations and Barriers to Homeownership

According to a recent LendingTree survey, 62% of renters are afraid they’ll never own a home:

- 65% cite the cost of a down payment as their primary roadblock

- 52% say home prices are too high in their areas

- 39% struggle with their credit scores

More than eight in 10 (83%) indicated a preference for homeownership over renting, including 76% of those earning less than $30,000 a year and 79% of Gen Z.

As for motivating factors:

- 62% prioritize the flexibility of owning a home

- 61% value stability

- 44% are motivated by home value appreciation

Recent first-time homebuyer trends

Even the youngest Millennials are of prime homebuying age. And the oldest members of Gen Z are entering the adult workforce. Together, these two generational groups are set to become the driving force in the housing market, adding to the pool of first-time homebuyers and investors.

On top of that, young adults who rent are earning more money now than in previous years, even after adjusting for inflation.

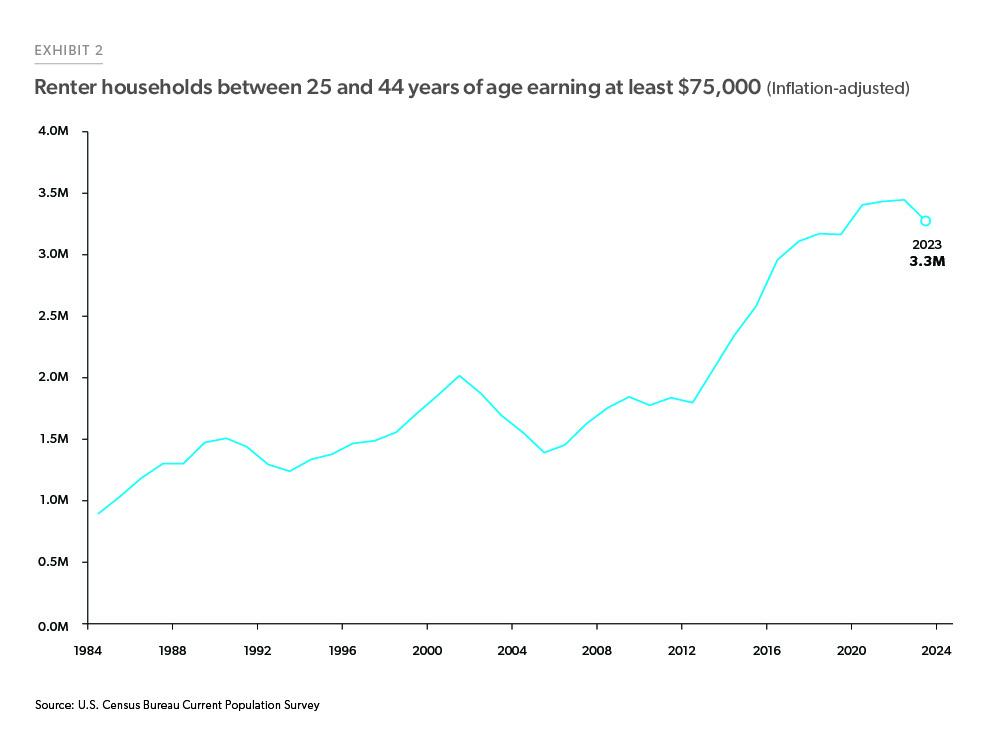

The chart below (Exhibit 2) shows renter households aged 25 to 44 with real, inflation-adjusted incomes of at least $75,000. Since 2012, the number of these households has risen significantly. And as of 2023, there were three million of these households in the U.S.

These favorable conditions are helping first-time buyers make inroads as a significant presence in the housing market.

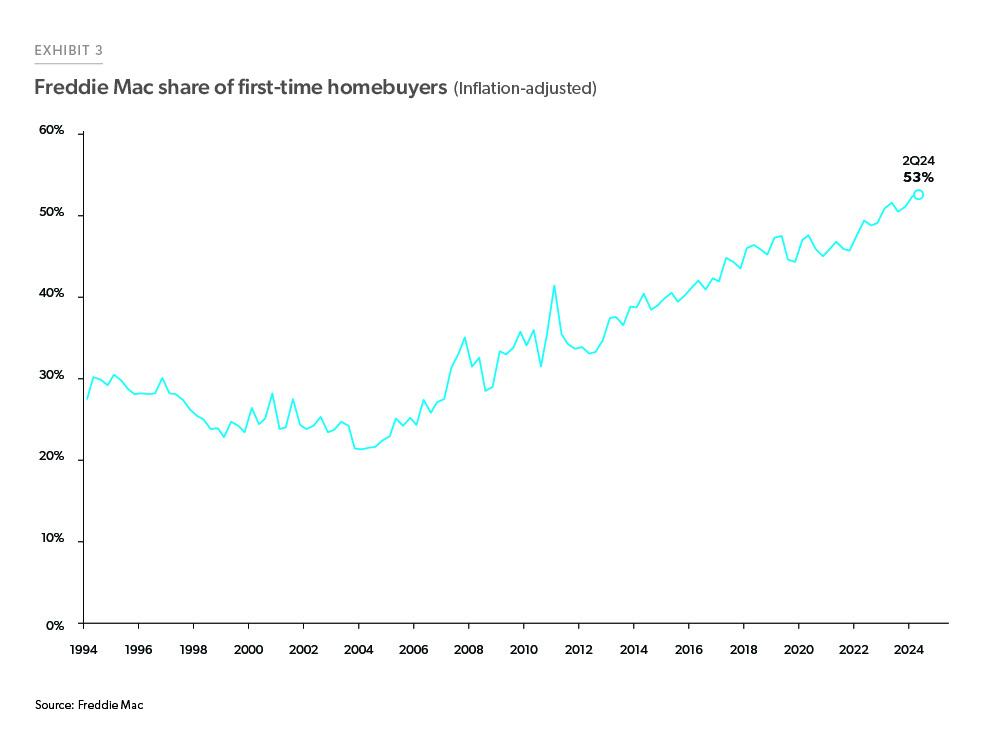

Using Freddie Mac-funded loan data, we can look at the historical share of conventional home loans going to first-time home buyers. The chart below (Exhibit 3) shows the share of first-time homebuyers has been steadily increasing from 2004, from roughly 20% of conventional mortgage loans to over 50% as of the second quarter of 2024.

One possible explanation for this increase in the share of first-time buyers receiving conventional loans is that repeat buyers have been less active in the market due to the lock-in effect of higher mortgage rates.

From 2018 through 2022, the share of first-time buyers held steady at around 45% of funded loans, but in 2023 and 2024, that share increased as the lock-in effect cooled demand in the resale market.

That said, even if the entirety of the increase from 2022 to 2024 was caused by the lock-in effect, first-time buyers would still account for a significant share of all loan activity. And if rate-lock persists, that only underscores the importance of first-time homebuyers as one of the few cohorts behind the growing demand for housing in today’s market.

Where is the first-time homebuyer share increasing?

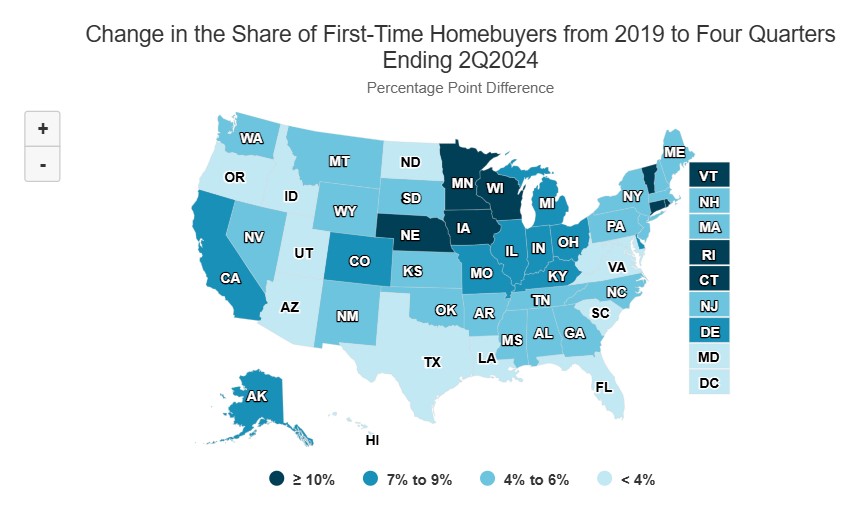

Freddie Mac’s loan data also shows which states have seen the most first-time homebuyer activity. Generally, most states show steady growth for this metric but markets in the Northeast and Midwest have seen particularly high shares of first-time buyers, especially in recent years.

Exhibit 4 below shows how the share of first-time buyers with Freddie Mac-funded loans has increased from 2019 through the four quarters ending in Q2 2024. The map also shows how the share of first-time buyers is growing more quickly in areas with moderate or slower home sale activity—while popular destinations with more repeat buyers, like Arizona and Florida, have seen smaller increases in first-time buyer activity over the past five years.

3 Potential headwinds for future homebuyers

To sum it up, Freddie Mac’s data points to three potential headwinds for future homebuyers, which includes renters as well as those currently living with relatives or friends:

- Low Housing Supply

- Affordability (due to rising homeownership costs)

- Tougher Economic Conditions—including higher unemployment rates, especially among renter households

Exhibit 7 from Freddie Mac’s report shows the unemployment rate for renter households has climbed from about 5% to more than 6% since 2023, while unemployment for owner-occupied households has remained relatively flat.

Between January 2000 and July 2024, cumulative entry-level house prices have gone up 63% more than high-end home prices. Elevated mortgage rates have compounded the issue, with the average 30-year fixed rate climbing to 7.00% as of yesterday (October 28, 2024).

As economic and supply obstacles persist, ensuring support for first-time buyers will be essential to maintaining a balanced and accessible housing market.

- BAM")