Key Details:

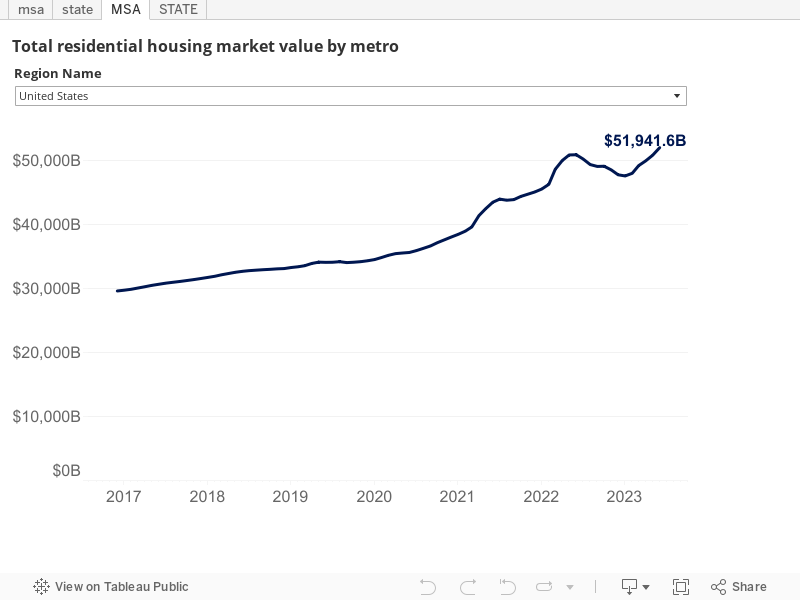

- A new Zillow® analysis shows the total value of the U.S. housing market has increased by more than $2.6 trillion year over year, climbing to just under $52 trillion, which is $1.1 trillion above the previous peak reached in June 2022.

- Miami edged out Washington, D.C. to make the top five most valuable metros, led by New York, Los Angeles, San Francisco, and Boston.

- Florida has climbed to the #2 spot on the list of most valuable states. California remains at the top.

After a brief downturn late last year, the U.S. housing market has grown in value by more than $2.6 trillion year over year—surging to nearly $52 trillion, which puts it at $1.1 trillion over the previous peak reached in June 2022.

That’s according to a new Zillow analysis, which highlighted the key factors behind this growth in the total value of the U.S. housing market. While the 1.3% increase in the average value of a U.S. home did contribute some of the growth, new construction gets most of the credit.

Compared to before the pandemic, the U.S. housing market has seen a 49% increase in total home value.

At the metro level, Miami has risen to the top five on the list of most valuable metropolitan areas, edging out Washington, D.C. And among the states with the most valuable real estate in the country, Florida now ranks at number two, surpassed only by California.

A steady flow of new homes hit the market this spring and summer, helping chip away at the deep inventory deficit and boosting the total value of the market. Despite the presence of higher mortgage rates, which deterred some home shoppers and kept many existing homeowners on the sidelines, enough buyers remained to keep the market moving. Builders recognized the unmet demand and responded by starting more projects. New home sales rose this year while existing home sales fell, and should make up a bigger piece of the home sales pie for as long as rates remain elevated.

Builders adapt to buyer needs and lean into higher-density construction

A small share of the growth in total home values is due to the 1.3% increase in the average value of the U.S. home compared to a year ago. But most of the credit goes to builders, who’ve been chipping away at the deficit in housing supply. While many would-be sellers decided to sit tight and hold onto their lower mortgage rates, a steady flow of new construction went on the market this spring and summer.

And with builders facing higher mortgage rates and record-low affordability, builders are adapting with smaller and more affordable homes. They’re also offering incentives like mortgage rate buydowns to entice buyers.

Wherever possible, builders have been prioritizing higher-density homes to work around rising home prices and increase housing supply. Unfortunately, in many parts of the country, builders still face obstacles that drive up the cost of the homes they can build.

Local housing policies that allow for greater housing density and open up buildable land to new construction would help.

Among metropolitan areas, the five with the most valuable real estate in the U.S. include—

- New York

- Los Angeles

- San Francisco

- Boston

- Miami

Miami recently edged out Washington, D.C., jumping from ninth place to the number five spot as recently as May 2021. The top four have largely held their place over the past five years.

Of the six U.S. markets that have gained the most in real estate value since the start of the pandemic, four are in Florida:

- Tampa (+88.9%)

- Miami (+86.6%)

- Jacksonville (+82.4%)

- Orlando (+72.3%)

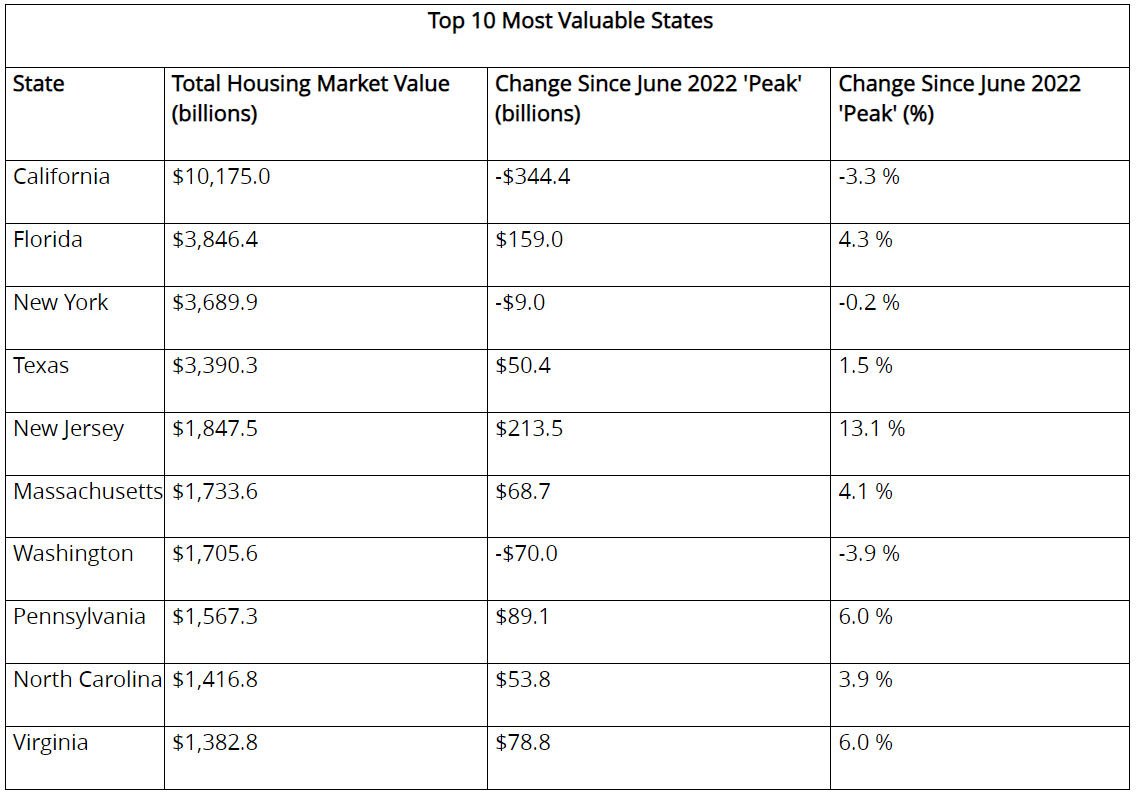

So, it’s not surprising to see Florida rise to number two on the list of most valuable states, surpassing New York, while California holds its position as the state with the most valuable housing market.

One reason for Florida’s strong new construction figures is the large growth in population—i.e., buyer demand. An increase in competition for existing homes has driven up home values, further incentivizing new construction.

California’s housing market amounts to more than $10 trillion, representing almost 20% of the national total.

Massachusetts, which held the number five spot just before the start of the pandemic, has slipped to number six, while Washington, D.C. now sits at number seven.

Takeaways for real estate agents

As a knowledge broker for your community, be aware of the challenges facing builders in your area as well as potential buyers and sellers.

Not all residents are keen on the idea of new apartment complexes being built in their neighborhoods. But most buyers can get behind policies that make it easier and less expensive for buyers to build new for-sale homes in their area, especially if those builders are offering concessions to make the new housing more affordable.

Be the agent who knows what’s going on with inventory, so you can be the first to let your buyer clients know all the options they can’t easily find online.

- BAM")

- BAM")

- BAM")