The time for creating your 2024 business plan is now.

Last Wednesday, Byron Lazine and Tom Toole hosted a value-packed business planning webinar. Both shared their favorite business planning tools and demonstrated, step-by-step, exactly how to make the best use of them.

BAMx members can watch the replays of the webinar and the after-party, and gain access to Byron and Tom’s business plans, on the BAMx platform.

Byron kicked off the webinar by asking Tom for his favorite quotes on planning. Tom had two:

- “Proper preparation prevents poor performance.”

- “Failing to prepare is preparing to fail.”

That second quote comes from Benjamin Franklin, who shares a birthday with Tom (minus the year). But both quotes essentially say the same thing: if you want to build a successful business, you need to plan for that success. Because it doesn’t just happen.

The new year starts in November

When January 2024 hits, you want to already be in motion, implementing the plan you’re making now.

This is the same plan you’ll be acting on in November and December of this year. Because, in the real estate industry, the new year starts in November. Any clients you take on in these months will most likely transact in 2024.

So, waiting until January to create a business plan for the new year makes zero sense.

For one thing, you want to be taking advantage of the fact that it’s generally easier to get a hold of people in the fourth quarter of the year. And when you’re planning out your days in October, November, and December, you need to have your whole year’s business plan in mind.

If you have a good final quarter of 2023, you’re more likely to have a strong first quarter of 2024. And that paves the way for an even better second quarter, and so on. Momentum kicks in, and you’ll be reaching your goals week by week and month by month.

So, how do you create a business plan that supports that kind of momentum?

3 key components of an effective business plan

Effective business plans have these three things in common:

- They have S.M.AR.T. goals

- They’re visible—all the time

- They have accountability built in.

#1 S.M.A.R.T. Goals

Every one of the goals included in your business plan—from your big annual goals to your daily targets—should be S.M.A.R.T. goals:

- Specific

- Measurable

- Achievable

- Relevant

- Time-bound

As for how many goals you should have in your business plan for the year, keep it to three.

The simple plan that’s specific is what works. You shouldn’t be trying to do a million different things at once… When you have zero goals or ten goals, you actually accomplish the same thing: absolutely nothing. Three is the magic number for everybody. Three key initiatives in your business tied to math—how much by when—and that’s going to be the thing that carries you through the day when you wake up, and you don’t feel like it.

#2 Visibility

Your business plan has to be in writing, and it has to be up and visual.

Byron recommends writing it out by hand. He keeps a visual plan with him wherever he goes. And he presented a fillable form for creating your own. BAMx members can download a copy in BAMx.

Tom keeps his business plan to one page and posts it where he can see it every day. Because if you don’t see it and review it on a daily or weekly basis, it’s easy to forget the plan.

Then, instead of being proactive, you become reactive, dealing with one emergency after another. And that leaves very little energy (if any) to work toward the goals you’ve set.

Just because your business plan is visible doesn’t mean it has to be pretty. In fact, it’s better if it’s not and you feel free to make changes when necessary. You’ll likely need to make revisions along the way as you learn. So, the less pretty, the better.

Write it all down, make it clear, and make it visible.

#3 Accountability

To build in accountability, you must tell other people about the plan. When other people know about the plan, and you check in with them on a regular basis to provide updates on your progress—as well as your setbacks—there’s less risk involved in slacking off and not working as hard as you could to reach your goals.

Internal accountability is important. Self-discipline is critical to your success in any business. But external accountability takes it to the next level. No one wants to tell their accountability partner that they dropped the ball and missed a weekly target—especially when they know they could have reached it.

If you remember only one takeaway from this webinar, let it be this: if you don’t have at least one external person to be accountable to, your plan is likely to fail.

Internal accountability depends too much on your own personal energy. When no one but you has to know that you skipped your daily workout to watch YouTube videos instead, it’s just too easy to keep scrolling through those Shorts.

This is why Byron, Tom, and their Knowledge Brokers co-host Lisa Chinatti have accountability calls three days a week. Even high-performing industry leaders have vulnerable moments when things aren’t going well. Between their businesses, these three take on upwards of 2500 transactions a year. And accountability is a huge part of that.

There are moments—very vulnerable moments where the business isn’t going in the right direction, where we need to adjust the plan that we built back in October of ‘22 because now it’s March of ‘23 and things are getting real. And we have to make an adjustment. Or we need to raise the level of commitment to the plan. Because we’ve got numbers and data that we’re committed to, and maybe now we’ve got three months of data that suggests it’s a little bit more that’s required or we’re going to need to lower that goal. And the ability for us to talk through those vulnerable moments and those struggles that are undoubtedly going to happen over the next 12 months allows us to push forward—allows us to make those adjustments and bounce it off of somebody…because if not, you cripple yourself for weeks on end thinking about it.

After all, your accountability partners aren’t there just to push you out of your comfort zone (though they can definitely do that); they’re also there to remind you that everyone has setbacks. What matters is how you handle them.

Goals that stick

As mentioned earlier, focus on three S.M.A.R.T. goals for your annual plan. Setting more than that is counterproductive; you’re more likely to tune them all out and get zero results.

Once you’ve got your goals for the year, break them down into quarterly, monthly, and weekly goals. Draw from those weekly goals when setting your daily targets. For example, Lisa Chinatti sets a daily goal of two appointments, and she doesn’t stop for the day until she’s set them.

Conversations lead to appointments, which lead to sales. And how many conversations you have is something you can control, along with—

- How many phone calls you make

- How many doors you knock

- How much time you spend (every day) responding to messages

- How much content you put out to deliver value to your database

Every one of those daily micro commitments should be tied to math. Everything should be trackable and measurable. Because whatever you consistently track and measure improves. This is where scorecards come in.

Whatever tasks you need to focus on to reach those daily targets, get them on your calendar. Time blocking for those tasks makes them a priority.

As Tom put it, quoting basketball coach Buzz Williams, “Show me your calendar, and I’ll show you your commitments.”

Why does this work?

The reason this kind of business plan works is because you have your annual goal at the top—your big-picture, all-encompassing goal for the year.

There’s a reason this 411 plan works—this is another Gary Keller special—is that you’ve got your annual goal at the top. Coming into November, think about what your annual goal is…it’s a big number and it can be scary, and it can cause paralysis because most people can’t even fathom how they’re going to get there when you set a big goal…. Then you have your activities and behavior that are going to support the goal. There should be no more than three—again, all tied to math.

Then you have your monthly goals, which you’ll break down week by week. But you don’t plan all four weeks at once. You get to week one, and you set your week one goal.

What you’re doing is coming up with micro-commitments that are chewable, digestible, and chunked down over a 30-day period into a 7-day period. And as you work on that, you can literally see the progress on a weekly basis so you’ve got a game plan and you’re not waking up trying to figure out what to do.

Keep your plan with you

As mentioned earlier, Byron keeps a paper version of his business plan in his bag. He keeps it where he’ll see it every day, and he takes it everywhere he goes. He puts pen to paper first when creating his business and life plan for the year. Then it’s got to be digital, too.

I just got off a flight an hour or two ago. And in my bag…I have the paper version of my business plan. It is a fold-out visual. Because if I’m at the Connecticut house, I’ve got it up. If I’m in Naples, I’ve got it up where I change in the morning every single day. I’ve got it visual, so I know what I’m going after. Still today, I’m using paper to be aware of what the plan is. And at this point, now, it’s digital, it’s in the leadership meeting at every level of the meeting.

And again, to be effective, every goal, every objective, and every micro-commitment has to be tied to math. Doing the math beforehand ties the overarching annual income goal to your present and to each month, week, and day of the year.

If you don’t do the math, you won’t see how that big number for the year relates to your day-to-day.

The business plan doesn’t have to be complicated, but it’s got to include math. You’ve got to know [your] numbers inside and out. You’ve got to break it down quarter by quarter and month by month, week by week. It’s the only way to attack this. If you wait two months on your 2024 business plan, you’re going to be well behind.

Creating a business and life vision board is an ideal first step to creating your business and life plan because the numbers on the plan should reflect the numbers on the vision board you create. With both, you’ll want a physical version you can take with you wherever you go.

Byron emphasized the instruction on the first page of his One Year Plan:

“Must be completed by early October of each year. Can be adjusted at any time during the year.”

#1—Must-Haves, Wants and Goals

On page two of the One Year Plan, the left-hand column is where you’ll put your “Must-Haves,” which includes everything you need to survive each month. That includes any payments you have to make on a monthly basis to pay down debt.

#2—The Benefit vs Pain Analysis

There’s a reason negative headlines get more clicks. People are hard-wired to avoid danger. Anything that helps you avoid an outcome you do NOT want is going to grab your attention more forcefully than something that promises something you DO want.

This is why answering the following questions is such an important part of this planning exercise:

- “What happens when you complete these commitments?”

- “What pain do I incur if I fail?”

Number two is probably easier to picture than the first because our brains are constantly busy imagining worst-case scenarios. Ask “What’s the worst that could happen?” and your brain will get right on that. It’s a survival thing.

After you add up the cost of your “must-haves” you know the bare minimum you need to earn every month after taxes to cover your needs. Next, you’ll make a list of your wants and tally up the cost of those. The vision board exercise is a big help with that.

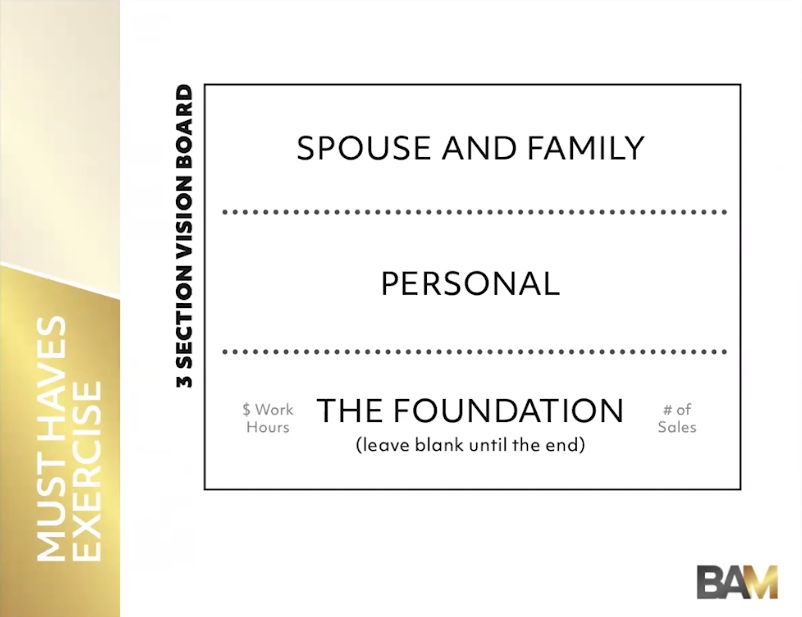

#3—The Vision Board

Page three of the One Year Plan is where you’ll create the vision board. And at the top of the three sections is where you’ll put the things your spouse/partner and/or kids want. If you don’t have a spouse/partner or kids, you could include the wants of close friends or family members.

Communication is critical here. Don’t assume you know what the people closest to you want in any year. Talk to them and encourage them to tell you exactly what they want. If for some reason, one of those things can’t go on the board for 2024, save it for a future vision board.

The middle part will have the things you want. And the bottom is the foundation. This is where you’ll record the numbers you need to keep in mind throughout the year:

- Total income after tax that you need to cover your needs and wants

- Number of sales you need to earn that amount (using average commission per sale) plus the amount that will go to taxes

- Hours you’ll have to work (based on income per hour)

- The amount you’ll need to earn per day and per hour to reach your income goals

Those numbers tell you exactly what it will take to not only survive but to make all those wants happen.

Pages four and five of the One Year Plan take you step by step through the math you’ll do to get the numbers you need for your business plan. Page six is all about your morning and nighttime routine, which have a huge impact on your mindset and your productivity. For one thing, the hours you work will impact how many people you can reach on a daily and weekly basis. You can get the complete plan in BAMx:

Revise as needed

Byron asked Tom how often he would recommend making revisions to a business plan over the course of a year. He gave the example of an agent who filled out the plan and then, months later, had to revise it because they were ahead of the game—or, alternatively, because they’d fallen behind.

As often as needed. I would argue that you don’t want to quit too soon on the plan if you’re not seeing results…90 days is the world we live in. So, if you’re coming up with the plan now, you’ve got to give it 90 days to see if it’s going to work or not. You’ve got to do the things. We also live in a 30-day cycle… The second [page] is something you should be doing and looking at regularly. Because a business plan is fluid…[it’s] something you’ve got to adjust based on what’s going on around you…because there are things you can’t control in every business. And if you’re not acknowledging that, and you’re thinking, ‘Well, I’m going to succeed in spite of them,’ instead of adjusting to them, you might be in for a rude awakening when the year’s over or when you start to see the results come in.

- BAM")