Brace yourself: recession talk is heating up again. And whenever that word starts making headlines, homebuyers, sellers, and even agents start wondering, “How will this impact the housing market?”

Will home prices plummet? Will mortgage rates skyrocket? Will the market freeze?

The truth, backed by historical data, is a bit more nuanced. Let’s cut through the noise and break down what actually happens to home prices, mortgage rates, and sales when a recession hits—and what real estate agents need to know.

For starters, recession warnings have faded somewhat since President Trump announced a 90-day pause on most tariffs, together with a hike in tariffs against China to 125%.

The announcement came after some speculation on how China could crush the U.S. housing market by unloading U.S. Treasuries.

On today’s Hot Sheet, Byron Lazine shed some light on whether this is a real danger and how Trump’s tariff pivot could impact housing.

Read on for a quick, data-backed review of recession’s impact on housing. Then tune in for Byron’s full explanation on the latest tariff news.

Recession Doesn’t Equal a Housing Crash

First things first: a recession does not automatically mean a housing crash. In four of the last six recessions, home prices increased, according to data from Cotality (formerly CoreLogic).

The 2008 crash was an outlier, driven by a toxic mix of bad loans, speculative buying, and a financial system on the brink.

Here’s what history tells us:

- Home prices typically follow their existing trajectory rather than falling dramatically.

- Buyer demand declines, but that doesn’t always translate into massive price drops.

- Regional markets react differently, depending on inventory levels and local supply-demand dynamics.

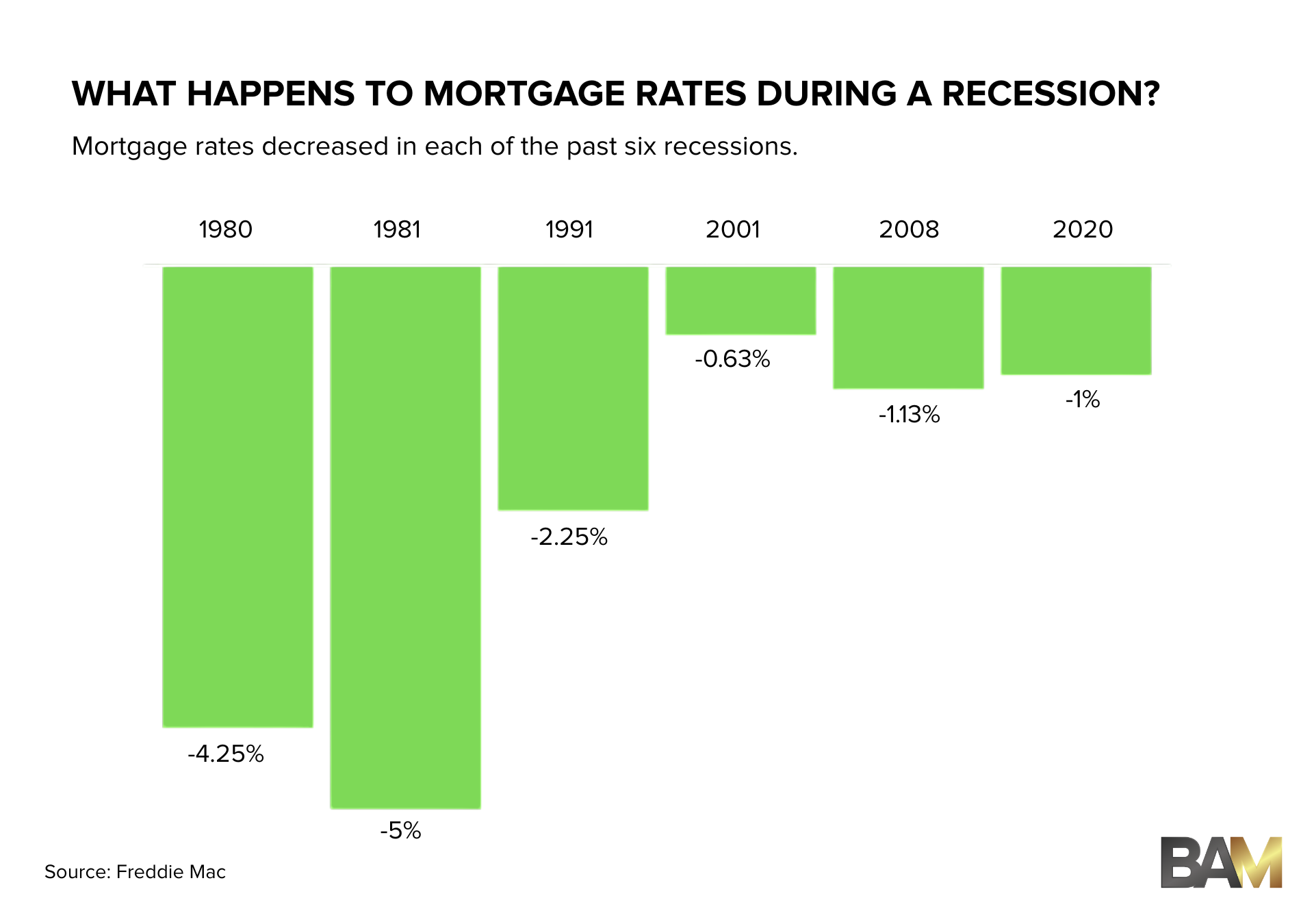

Mortgage Rates Usually Drop During Recessions

While home prices tend to stay on course, mortgage rates tell a different story.

According to data from Freddie Mac, mortgage rates declined in all six of the last U.S. recessions. That’s because economic slowdowns often lead the Federal Reserve to lower interest rates, which in turn eases borrowing costs.

How Home Sales and Inventory Could Shift

A recession almost always means fewer buyers in the market—but in today’s landscape, there isn’t much room for demand to fall further. According to Realtor.com, home sales in 2024 were already at their lowest level since 1995, and early 2025 data isn’t showing much improvement.

So what happens next?

- Regions with more inventory (South & West) may see home prices fall faster. These areas are close to pre-pandemic inventory levels, meaning less competition among buyers.

- Markets with tight supply (Northeast & Midwest) may hold steady longer. Inventory is still down 45.2% in the Midwest and 57.5% in the Northeast, limiting how much prices can drop.

- Homebuilders are likely to pull back on new construction, thanks to cost pressures and uncertainty. That could keep long-term supply challenges intact, even if demand cools temporarily.

Homeowners Are in a Strong Equity Position

One of the biggest differences between now and 2008? Homeowner equity. Thanks to years of rapid price appreciation, most homeowners are in a strong financial position.

Here’s how Realtor.com breaks it down:

- Even if home prices dropped 10%, homeowner equity would still sit at 69.5% of total real estate value, close to late 2021 levels (based on Federal Reserve data).

- A 20% drop would bring equity to 65.6%, which is still on par with 2019 levels.

- 54% of homeowners have a mortgage rate below 4%, meaning they’re less likely to be forced into selling.

Even if prices correct, most homeowners have enough cushion to absorb it without a wave of distressed sales hitting the market.

Though a recession would mean buyers pull back even further, there isn’t much further to fall, so the drop would likely be tame relative to recent sales volume.

Regions with more home supply, such as the South, would likely see home prices fall more quickly in a recession as buyer demand pales in comparison to already ample home supply. Under-supplied areas, such as the Northeast, could see prices hover longer before falling, as the pullback in demand actually allows for more balance in the market.

What This Means for Agents

Real estate pros need to be ahead of the curve when it comes to recession fears. Here’s what you should focus on:

- Educate buyers and sellers. Many people assume a recession = a housing crash. The data says otherwise. Be the expert who brings clarity.

- Watch mortgage rate movements. If rates drop, affordability improves. Be ready to act when buyers see an opportunity.

- Understand regional trends. Markets with more supply will feel the effects differently than those with tight inventory. Use hyper-local data to guide your clients.

- Highlight long-term value. Even if prices soften, real estate remains one of the strongest wealth-building tools. Focus on long-term equity growth.

These are actionable tips whether recession odds are strong or not. And with yesterday’s announcement that Trump has both paused and lowered tariffs on most foreign trade partners—with China as the sole exception—Goldman Sachs has rescinded its recession call.

Logan Mohtashami of HousingWire, who’s been busy addressing consumer fears about the housing market, and correcting doom-and-gloomers, retweeted the news on X:

https://t.co/fXkX9qkD0v pic.twitter.com/KVACO5T3JP

— Logan Mohtashami (@LoganMohtashami) April 9, 2025

That said, it’s still worth pointing out that a recession doesn’t mean the housing market is heading for disaster. History shows home prices tend to stay resilient, mortgage rates often decline, and homeowner equity remains strong—even in downturns.

- BAM")