Key Details:

- Fannie Mae has revised its outlook for the U.S. economy and housing market. Its December report predicts an economic deceleration in 2024, along with a slow recovery for home sales and mortgage originations.

Last Thursday, December 14, Fannie Mae’s Economic and Strategic Research (ESR) Group issued a report with an updated economic and housing forecast for 2024.

While they expect a slowdown in the U.S. economy in the months ahead, they’re projecting a slow recovery for both home sales and mortgage originations.

At the start of 2023, the ESR Group was forecasting a modest recession in 2023, but the combination of disinflation and low unemployment suggests a soft landing is more likely.

As for housing, as they predicted, this year’s record-low housing affordability, lock-in effects, and a severe shortage of for-sale housing supply brought the pace of existing home sales to its lowest since the Great Financial Crisis.

However, the resilience of new home sales exceeded their expectations. And Fannie Mae now expects the recent drop in mortgage rates to drive an uptick in home sales.

Tune in to this episode of the Hot Sheet for a breakdown from Byron Lazine, and read on for more details on Fannie Mae’s revised outlook for the 2024 housing market.

Drivers of slow sales will persist in 2024, with modest improvement over 2023

By now, we’re familiar with the usual reasons for slowdowns in home sales:

- Low housing affordability

- Lock-in effects

- Low housing supply

While the ESR Group sees some relief ahead, for the most part, they expect all three of the above to continue in 2024.

With the 10-year Treasury rate’s continued decline since the completion of their last forecast, they acknowledge some upside risk to their numbers for both sales and mortgage originations.

But with mortgage rates still comparatively high, they expect home sales to remain suppressed, with total sales ending 2023 at 4.8 million, with a similar pace of 4.8 million in 2024 and 5.4 million in 2025.

That said, this year’s growth in home prices and refinance activity has upgraded their forecast for total single-family mortgage originations:

-

- $1.5 trillion in 2023

- $1.9 trillion in 2024

- $2.3 trillion in 2025

They entered 2023 forecasting around 4 million existing home sales for the year—less than most other forecasters and the slowest pace since 2010.

While volatile mortgage rates throughout the year impacted the ESR Group’s outlook on the market, they held to a narrow range for their home sales forecast. And they expect the pace of home sales to show only marginal improvement over 2023 numbers.

October’s low point, where the annualized pace of home sales hit 3.79 million, is likely at or near the lowest point. And while October’s low in pending sales pointed to a drop in the next month’s home sales, purchase mortgage applications bounced roughly 15% off their trough in November, according to Mortgage Bankers Association, thanks to the drop in mortgage rates.

Housing forecast changes

Mortgage rates

Given the recent drop in interest rates, the ESR Group has lowered its forecast for mortgage rates this month and is now predicting an average FRM30 rate of 7.4% over Q4 2023.

From there, it expects an average FMR30 rate of 6.7% in 2024 and 6.2% in 2025.

The ESR Group completed this forecast on Monday, December 11. Rates have fallen further since then and are expected to remain volatile as the market transitions from tightening to loosening monetary policy in 2024, adding risk to Fannie Mae’s outlook for mortgage rates.

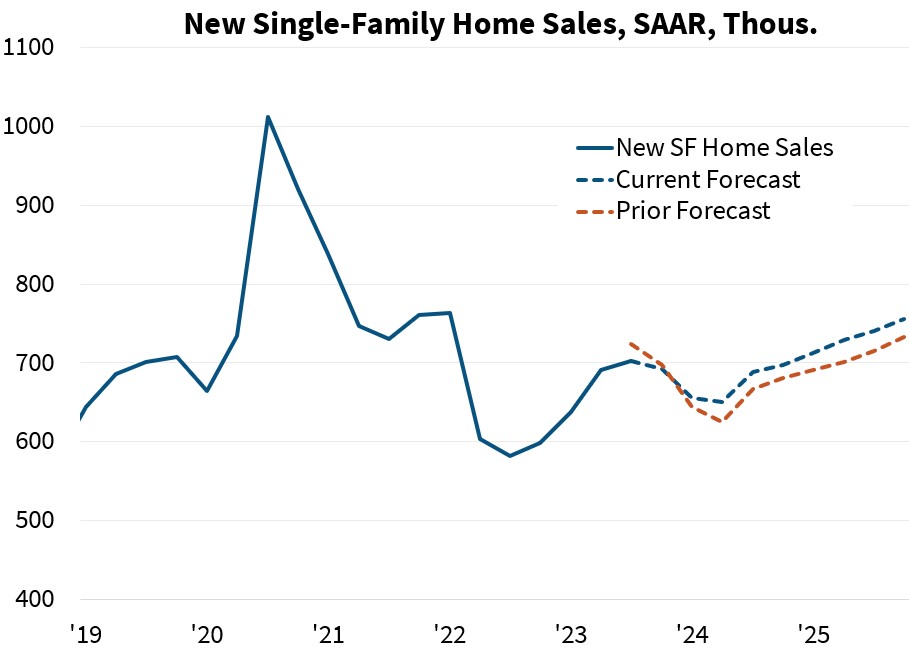

New vs existing home sales

While the ESR Group anticipated the resilience of new home construction beyond what is typical in an economic downturn—thanks to the shortage in housing inventory—they did not anticipate home sales and single-family starts to flout high mortgage rates to the degree they have in recent quarters.

Homebuyers appear desensitized to higher mortgage rates compared to 2022, judging by the lower-than-expected degree of order cancellations even in the wake of the last Fed rate increase.

On top of that, homebuilders, who’ve benefited from lower materials costs and healing supply chain disruptions, are willing and able to offer concessions to buyers, including mortgage rate buydowns, to offload new housing inventory and stimulate home sales.

Given that trend, the ESR Group now expects new home sales to drop only slightly in 2024 from their current levels due to a modest contraction in the U.S. economy.

In October, new single-family home sales dropped 5.6% to a seasonally adjusted annualized rate (SAAR) of 679,000. But the lower projected path for interest rates has led to a modest upgrade in Fannie Mae’s forecast for new home sales.

Existing home sales in October hit the lowest level since 2010 with a seasonally adjusted annualized rate of 3.79 million, falling below Fannie Mae’s expectations. With pending sales for the month also weak, the ESR Group revised downward their Q4 2023 estimate for home sales.

That said, beginning in 2024, they’ve revised their forecast modestly upward, largely because of the lower projected mortgage rates. But the volatility of long-run mortgage rates continues to pose a risk for home sale projections.

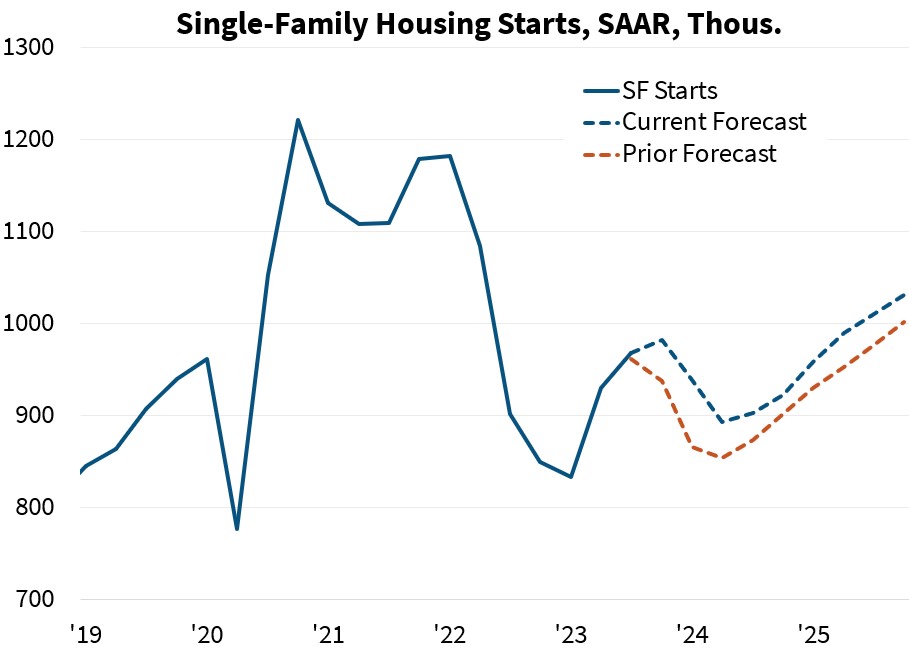

Housing starts

In October, single-family housing starts increased to a seasonally adjusted annualized rate of 970,000, and permits reached a pace of 968,000.

While they still project a softening trend in housing starts for the coming year, in line with their expectation of a slowdown in the U.S. economy, the ESR Group has revised their earlier forecast upward due to lower projected mortgage rates.

As before, they also expect the shortage in existing homes for sale to boost new home construction in the medium term.

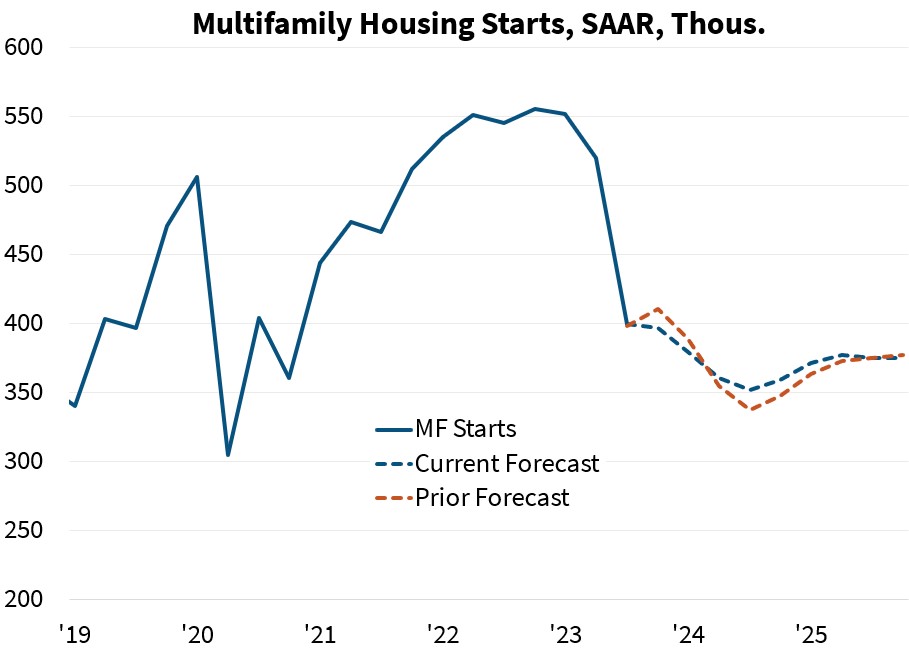

October also saw an increase in multifamily starts, climbing to a seasonally adjusted annualized rate of 402,000. Permits increased to a SAAR of 519,000.

Given incoming data, the ESR Group revised slightly upward their near-term forecast for multifamily starts, which they expect to decline in 2024 due to muted rent growth nationwide and the increase in supply as new multifamily units are completed.

Single-family home prices

Just as the resilience in new home sales came as a (welcome) surprise, home price growth in 2023 also exceeded the expectations of Fannie Mae economists with a modest rebound after its mild declines of late 2022.

September home prices increased 6.0% year over year, according to the most recent non-seasonally adjusted FHFA Purchase-Only House Price Index (HPI).

The ESR Group updates the Fannie Mae HPI home price forecast on a quarterly basis and will issue the next update in January 2024.

Single-family mortgage originations

As a function of both home sales and home prices, the outlook for mortgage originations drifted gently upward during 2023 but remained within a 9% band.

This month, the ESR Group upgraded their forecast for purchase mortgage origination volumes, consistent with upgrades to their forecast for home sales. The Group now expects purchase volumes in 2024 to reach $1.4 trillion—a 13% upgrade ($29 billion) from 2023’s projected volumes of $1.3 trillion.

Based on projections for continued growth in 2025, the ESR Group anticipates purchase origination volumes will reach $1.6 trillion.

They’re also projecting 2024 refinance origination volumes of $451 billion—a $23 billion upgrade over their previous forecast, due primarily to the more favorable mortgage rate environment.

Based on recent data from the Refinance Application-Level Index, refinance application volumes have increased slightly from their low point in October as mortgage rates have dropped.

In 2025, the ESR Group projects an increase in refinance volumes to $686 billion.

Read the full report for more information.

- BAM")