Key Details:

- A new ATTOM report shows a quarterly and annual drop in profit margins from home sales in 89 (or 66%) of the 134 U.S. metros analyzed.

- Sixty-three of those metros reported annual increases in seller profit margins.

- ATTOM’s recently released Q1 2024 U.S. Home Sales Report provides a detailed breakdown of profit margins, median home price changes, homeownership tenure, foreclosures, cash sales, investor activity, and FHA-financed home purchases.

Last week, ATTOM released its Q1 2024 U.S. Home Sales Report, which showed a decline in profit margins for median-priced single-family home and condo sales to 55.3%—down from 57.1% the previous quarter (Q4 2023) and from 56.5% in the first quarter of last year.

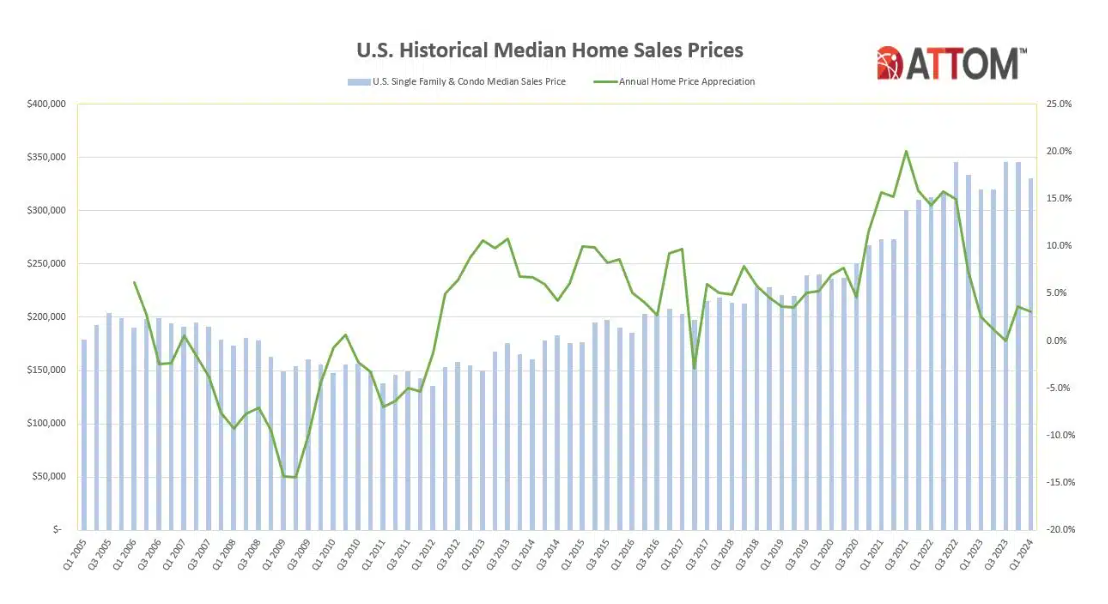

The quarterly and annual drop in profit margins coincided with a quarterly 4.3% decline in the national median home price, down to $330,000.

According to ATTOM’s report, though home prices typically soften during the winter homebuying season, the recent quarterly decline in profit margins is one of the most significant of the past 10 years.

Concurrently, after several quarterly increases last year, investment returns for sellers have dropped for the second consecutive quarter, reaching their lowest level since mid-2021.

Yet, despite the recent drop, home seller returns have still outperformed most of the housing market boom observed over the past 10 years. The typical gross profit for home sales nationwide in the first three months of 2024 was $120,500.

“The latest price and profit numbers show notably downward trends, which raises new questions about whether the housing-market boom is indeed ebbing, or even ending, after so many years of improvement. But due caution is needed in looking at the first-quarter data and what the patterns mean. We saw a similar downward pattern from late 2022 into early 2023, and then the market surged. Plus, profits and profit margins still are very high by historical measures. Amid all that, the Spring buying season will be a huge barometer for whether the market still has steam in its engine.”

Metros with the largest annual and quarterly increases in profit margins

Per ATTOM’s report, typical profit margins—meaning the percent difference between median purchase and resale prices—fell from Q4 2023 to Q1 2024 in 89 (or 66%) of the 134 metros analyzed.

They also fell year over year in 71 (or 53%) of those same 134 metros. On the flipside, profit margins increased from the previous year in 63 (47%) of those metros.

Among metros with sufficient data and at least 1,000 single-family home and condo sales in Q1 2024, those that experienced the biggest annual gains in typical profit margins were—

- Peoria, IL (margin up from 32.6% in Q1 2023 to 52.8% in Q1 2024)

- Scranton, PA (up from 88.1% to 106.5%)

- Oxnard, CA (up from 55.1% to 71.2%)

- Rochester, NY (up from 50.4% to 65.2%)

- San Jose, CA (up from 85.8% to 100%)

Also, if 89 of those 134 metros registered quarterly declines in profit margins, that still leaves 45 metros where margins either increased from the previous quarter or remained flat.

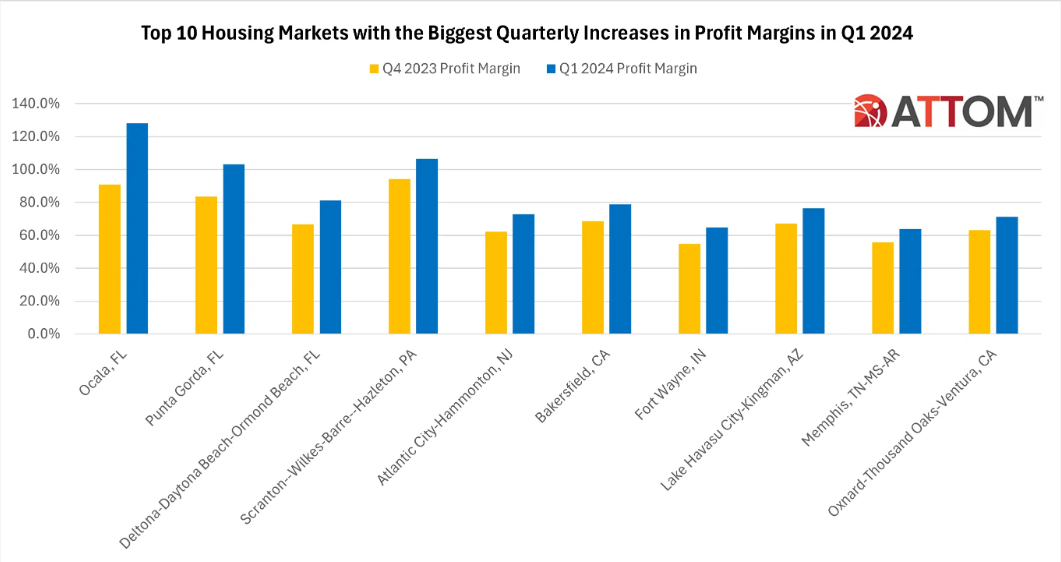

Top 10 metros with the largest quarterly increases in home sale profit margins:

- Ocala, FL (up from 90.8% in Q4 2023 to 128% in Q1 2024)

- Punta Gorda, FL (up from 83.5% to 103.1%)

- Deltona–Dayton Beach-Ormond Beach, FL (up from 66.7% to 81.1%)

- Scranton–Wilkes Barre–Hazelton, PA (up from 94.1% to 106.5%)

- Atlantic City–Hammonton, NJ (up from 62.1% to 72.8%)

- Bakersfield, CA (up from 68.7% to 78.7%)

- Fort Wayne, IN (up from 54.7% to 64.7%)

- Lake Havasu City-Kingman, AZ (up from 67.1% to 76.3%)

- Memphis, TN-MS-AR (up from 55.7% to 63.9%)

- Oxnard-Thousand Oaks-Ventura, CA (up from 63.1% to 71.2%)

Read the full ATTOM report for Q1 2024 for a full breakdown of market indicators for the first quarter, including median home price changes, homeownership tenure, cash sales, foreclosures, investor activity, and FHA-financed purchases.

- BAM")