- BAM")

- BAM")

Key Details:

- Realtor.com®’s March 2024 Rental Report shows a $5 annual drop in the median U.S. asking rent to $1,722—up $14 from the previous month.

- Median rents declined across all rental size categories in Realtor.com’s analysis—from studio apartments to two-bedroom rental units.

- Northeast and West markets experienced annual rent increases, while rents in Midwestern markets remained flat, and Southern markets saw year-over-year declines.

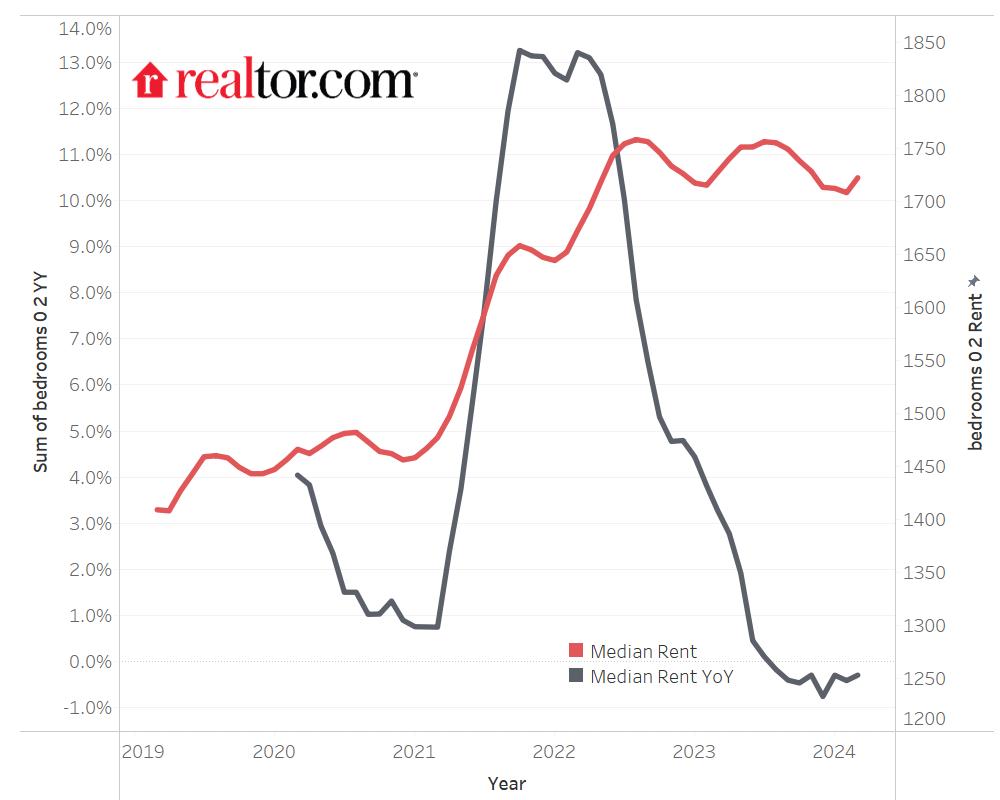

Realtor.com has released its March 2024 Rental Report showing a nationwide 0.3% decline in median asking rents, marking the eighth annual decline in a row for 0-2 bedroom rental properties since trend data was first recorded in 2020.

That pace of decline is just a hair off the -0.4% observed in February 2024.

The median asking rent in March was $1,722—$5 less than a year ago but up $14 from the previous month, following the usual seasonal trends.

Despite the annual drop, the national median rent is just $36 (or -2.0%) under the peak set in August 2022. And it’s still $313 (22.2%) higher than the median rent reported for March 2019.

Rising shelter costs are a major factor behind the sticky inflation rate. Even with the small annual decline overall, stabilizing rental prices could make reducing the overall inflation rate more difficult, further muddying the waters for Fed policy decisions.

It should also serve to remind policymakers of the widespread need for additional housing construction, with an emphasis on affordable housing, to alleviate the ongoing supply shortage.

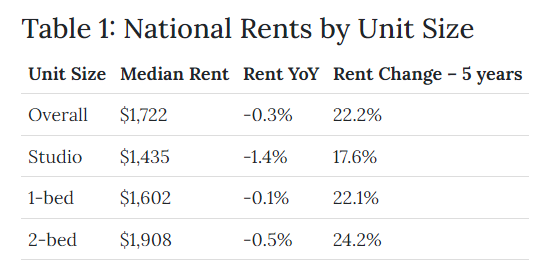

Median rent declined across all rental size categories

Median rents dropped year over year in all rental size categories in Realtor.com’s analysis:

- Studio: $1,435, down $21 (-1.4%) year over year

- One-bedroom units: $1,602, down $2 (- 0.1%)

- Two-bedroom units: $1,908, down $10 (-0.5%)

Northeast and West rents went up year over year

The median rent in the West rose 0.4% year-over-year in March—the first annual increase after 13 straight months of declines.

Western metros with the fastest annual growth in March 2024:

- San Diego–Chula Vista–Carlsbad, CA (2.9%)

- Los Angeles, CA (1.6%)

- San Jose–Sunnyvale–Santa Clara, CA (1.5%)

Among Western metros, the largest annual declines in median asking rent in March 2024 were reported in Phoenix, AZ (-3.2%) and Denver–Aurora–Lakewood, CO (-1.9%).

Meanwhile, major Northeastern markets saw continued rent growth, especially in—

- New York–Newark–Jersey City, NY-NJ-PA (3.8%)

- Boston–Cambridge–Newton, MA-NH (3.3%)

- Pittsburgh, PA (2.8%)

Rents are climbing faster in expensive markets for number of reasons:

For one, inflated housing costs—due to a combination of high home prices and elevated mortgage rates—has compelled many prospective buyers to stick with renting for longer. That, in turn, drives up rental demand in these markets, which keeps median rents trending upward.

Second, unemployment rates in Western metros have climbed from 3.9% to 4.7% between February 2023 and 2024. The short-term effect of that increase is a further incentive for renters to put their homebuying aspirations on the back burner, again strengthening demand and driving up prices for existing rentals.

If the labor market continues to worsen, however, renters in the area may choose to relocate to a more affordable area, reducing rental demand and sending prices on a downward trend.

Meanwhile, median rents in pricey Northeastern metros like New York, NY (+3.8%) and Boston, MA (3.3%) continue to climb at a faster rate than Western metros (for the most part) for couple of reasons:

- The Northeast labor market is stronger, which contributes to higher demand

- Supply growth is failing to keep up with demand, driving up competition and, consequently, rental prices.

In March 2024, the Northeast had seasonally adjusted annual rates for multifamily supply growth at 41,000 units—down 37.9% from the previous year.

In the West, that rate remained significantly higher at 161,000 units, though that figure was down 12.0% compared to a year ago.

Midwest median rents are holding steady

Overall, median rents in Midwest markets remained flat from a year ago (+0.0%), though some markets reported notable increases.

Top performing rental markets in the Midwest:

- Chicago, IL (up 4.3% year over year)

- Kansas City, MO (3.4%)

- Indianapolis, IN (3.3%)

Midwest markets are typically more affordable compared to the Northeast and West even as rents climb faster in metros like Chicago. The median rent in the Windy City ($1,846) was higher than its Midwest neighbors but still over $1,000 less than rents in New York City ($2,876) and Los Angeles ($2,869).

That said, Chicago’s unemployment rate in February 2024 reached 5.3%—up from 4.5% a year earlier—while the overall unemployment rate across the Midwest rose from 3.6% to 4.0% during the same period.

If this keeps up, the softening labor market could lead to slower growth or even declines in rental prices, possibly due to renters choosing to move in with family or friends to reduce costs.

Southern markets see a drop in median rents

The median asking rent for 0-2 bedroom rentals in the South declined year over year by 1.5%.

The five metros with the biggest annual declines:

- Austin, TX (-4.7%)

- Memphis, TN (-4.4%)

- Atlanta, GA (-3.7%)

- Miami, FL (-3.6%)

- Nashville, TN (-2.9%)

On the other hand, the South had a relatively low unemployment rate at 3.4% in February 2024, indicating a strong labor market, which contributes to strong demand for housing (both rentals and for-sale homes)

This region also reported seasonally adjusted annual multifamily completion rates of 273,000 units—rising 71.7% between March 2023 and March 2024. The stronger supply growth has exerted downward pressure on rent prices even as rental demand remains high.

Read the full report for more information, including methodology.

- BAM")