- BAM")

- BAM")

Key Details:

- Zillow released a new report showing more than 20% of homeowners are now considering selling their homes within three years, largely due to the overall (modest) improvement in housing affordability.

- Falling mortgage rates have given buyers more breathing room and loosened the grip of the lock-in effect for many homeowners with lower rates.

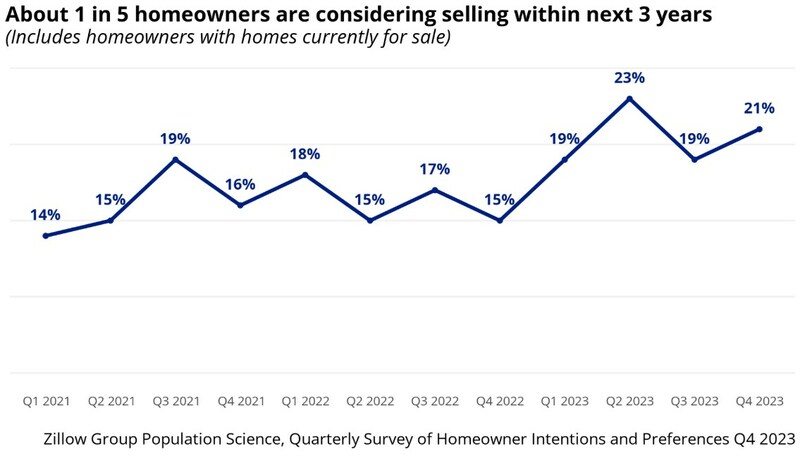

According to a new Zillow report, more than one in five homeowners thinking about selling within the next three years.

That’s in spite of the persistent gap between today’s lower mortgage rates and the rates they’re locked into from purchases made when interest rates were lower. The lock-in effect may be less of a deterrent now for homeowners with low rates who are ready to make a move.

That said, even with lower rates and recent improvements in housing supply, competition for available homes is still high, driving up home sale prices.

Good news for sellers—not so much for first-time buyers.

Buyers found significant savings as rates fell. But mortgage rates are fickle things, as we’ve seen in recent weeks, and they’ll play a massive role in determining appreciation and affordability — especially for first-time buyers — going forward in 2024. Fortunately, rate lock appears to be wearing off for some homeowners, who show encouraging signs that they’re ready to come back to the market.

Byron Lazine reviewed Zillow’s report on Wednesday’s episode of the Hot Sheet, (starting at 06:35).

Read on for the highlights.

Roughly one in five homeowners are thinking of selling within three years

According to Zillow’s report, 21% of U.S. homeowners are warming up to the idea of selling their homes within three years—up from 15% one year ago.

Fielded in the final quarter of 2023, the survey turned up another interesting piece of news: the share of U.S. homeowners thinking of selling was nearly the same for those whose current mortgage rates are above 5% and those whose rates are below that.

That’s quite a difference from just six months ago when homeowners with rates above 5% were almost twice as likely to consider selling compared to those locked into rates below 5%.

Zillow’s data shows more homeowners with lower rates are open to selling their homes in the near future. Current mortgage rates, which have dropped from last October’s high of 8%, are less of a deterrent for those feeling the push to sell.

A more affordable market helps these homeowners in more than one way.

- More buyers in the market shopping for homes—meaning a higher likelihood of competition and offers above the asking price

- Greater affordability when shopping for their next home

Since many of these homeowners have equity to put toward their next home purchase, they have an advantage over first-time homebuyers.

That’s especially true given the general consensus on home values in 2024.

Housing affordability has improved (to a point)

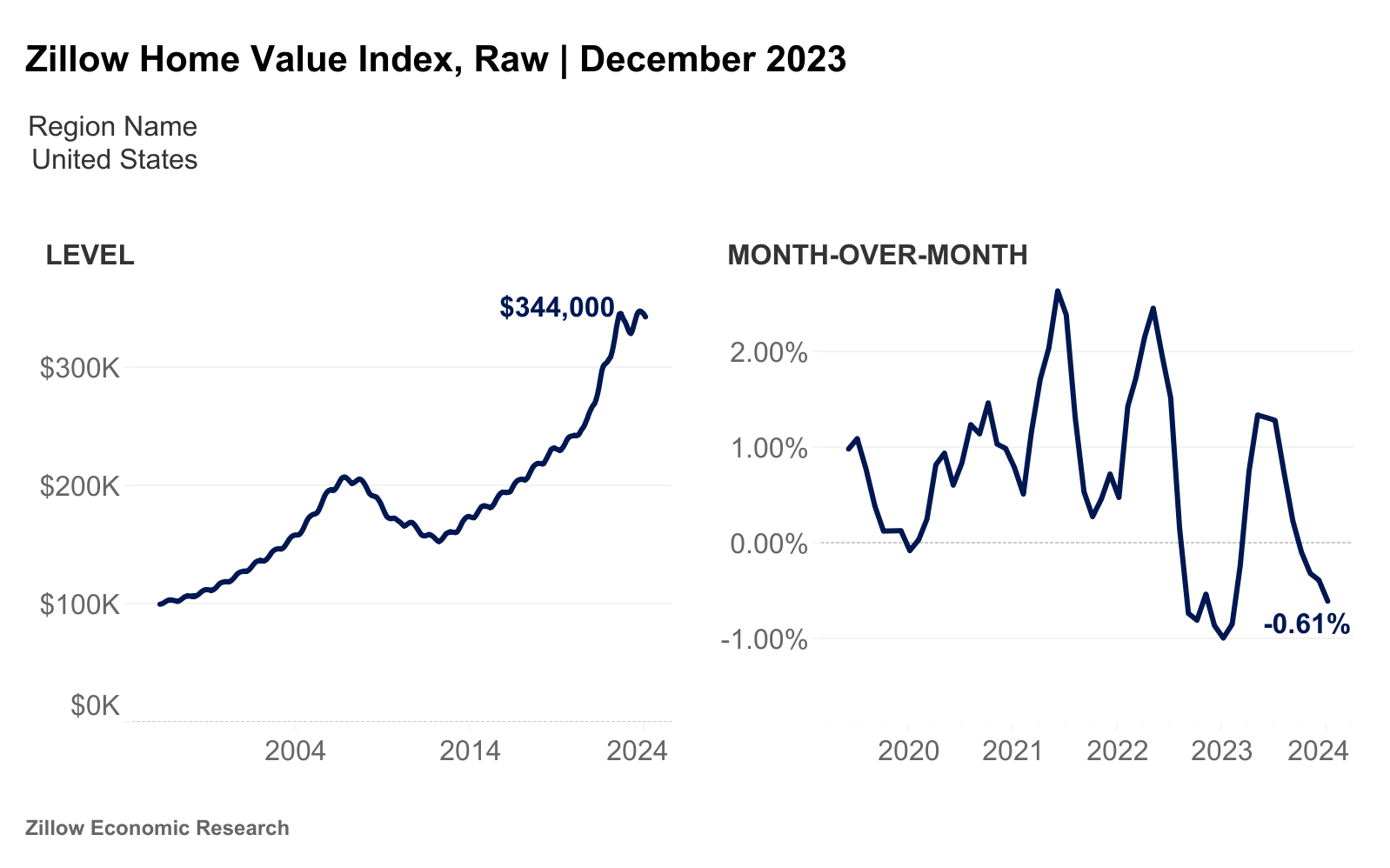

For the buyers out there who’ve been waiting for an improvement in housing affordability, Zillow’s report offers some encouraging news: the monthly payment for a new mortgage on a typical U.S. home (assuming 20% down) is now $1,790—down $143 compared to last October.

That drop is enough to bring affordability back to homebuying, at least for some.

For the first time since April of last year (2023), homebuyers who put 20% down on a new mortgage and earn the (national) median household income would pay less than 33% of that income on their monthly payment.

That said, home prices are so high right now that, in many expensive metros, the median income-earning U.S. household can’t even qualify for a mortgage.

Not only that, but for many first-time homebuyers, a 20% down payment is out of the question.

Half of all U.S. homebuyers put less than 20% down. And half of first-time homebuyers use either a loan or a gift from family or friends to make a down payment of any size.

Plenty of prospective buyers are still on the fence about buying or renting in 2024, given the complex picture of housing affordability, even with the drop in mortgage rates and modest improvements in housing supply.

While it’s a great place to start, there’s a lot more for buyers to consider than whether or not they can qualify for a mortgage.

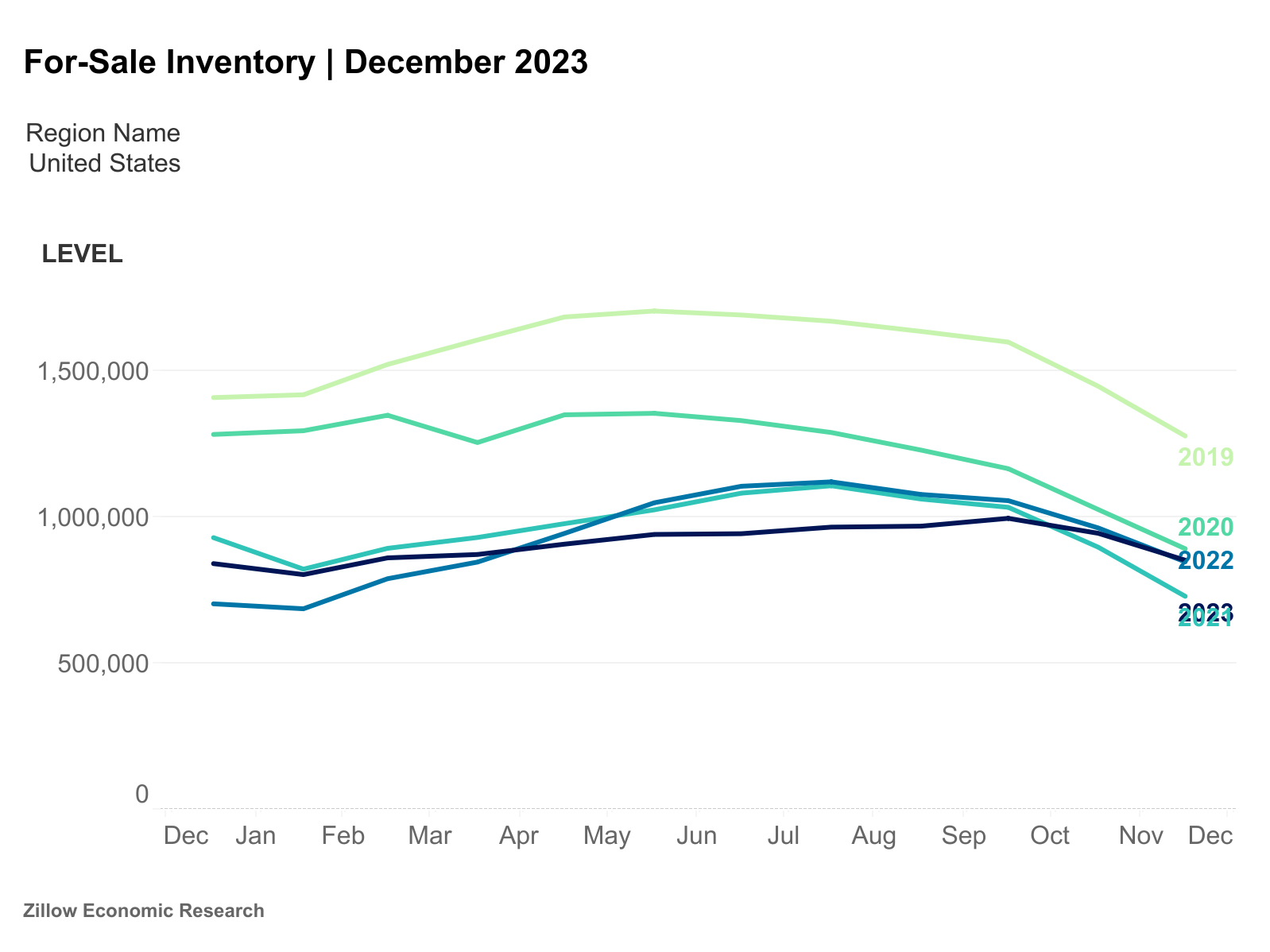

Inventory growth is slightly better than a year ago

Inventory has definitely made some progress climbing out of its pandemic hole.

New listings are trickling into the market at a slightly faster pace compared to a year ago, and while levels are still lagging 14.5% behind pre-pandemic norms, they’re at least trending in the right direction.

It’s too soon to tell whether and at what pace that growth will continue in 2024.

Total housing inventory for December 2023—i.e., the number of for-sale listings at any time during the month—fell month over month by 9.7%. But we still had 0.6% more total listings active that month compared to December 2022.

The supply of for-sale homes has made its first year-over-year gains since last April, and total inventory levels are now 36% below pre-pandemic averages, which is a large enough gap to keep competition strong for available listings but down from the 45.8% gap recorded last May.

Inventory levels dropped year over year in 33 of the 50 major U.S. markets, with the biggest annual declines in—

- Las Vegas, NV (-35.2%)

- Seattle, WA (26.9%)

- Sacramento, CA (-25%)

As rates go down, competition ramps up

While inventory remains historically low, buyers should expect competition for available homes, and especially for the most attractive options.

Price cuts are already less popular during the winter months. And this December (2023), the percentage of listings with a price cut was just under 16%, which is the lowest since last April.

Though buyer demand has cooled since the peaks reached in 2021 and 2022, listed homes are spending about 30 days on the market, going under contract 50% faster compared to pre-pandemic norms.

According to the latest Zillow data, almost 30% of homes nationwide—up from 20% in 2018–2019—are selling for more than the original list price.

Read the full report for more information, including methodology and metro-level statistics.

- BAM")