Key Details:

- A new Zillow report breaks down the affordability crisis in the U.S. showing the gap between household formation and available housing, which currently sits at 4.3 million missing homes.

- Not only are there far fewer homes than households in the U.S., but the gap between the two is growing.

- Nearly seven out of 10 (68%) households doubling up with non-relatives had a family income of $35,000 or less.

The gap between American households and available homes is widening.

From 2015 to 2021, housing stock in the U.S. grew by about 6.3 million units. Meanwhile, the number of families grew by 7.9 million, and 7.1 million new households were formed, outpacing the growth of housing supply. What happened next was predictable: supply went down, and competition for available housing intensified, driving up housing costs.

According to a new Zillow report, the U.S. is now looking at a housing shortfall of 4.3 million for the growing number of “missing households”—or the number of people currently living in homes owned or rented by other families.

The severe lack of housing—and particularly the more affordable options—is leaving millions of American households without a place to call their own.

This is a nationwide affordability crisis. And it calls for policies and investments at the national and local level that will boost the construction of new, affordable housing. Making it easier for buyers to make smaller down payments only helps when there are affordable homes available to buy.

Nearly seven out of 10 of these “missing” households have a family income of $35,000 or less, emphasizing the need for more entry-level housing—or “starter homes.” Because there aren’t nearly enough to go around.

The U.S. housing market is like a high-stakes version of the game musical chairs. There are simply not enough homes for millions of people. Unless we address the shortage of smaller, more-affordable, starter-type homes, we risk leaving families without a seat — and it will only get worse over time.

Missing households

In 2021, the U.S. was home to nearly 8 million “missing” households—or households with “missing” homes, depending on how you want to look at it. With only 3.7 million housing units available to buy or rent, that left 4.3 million whose choices were homelessness or moving into homes owned or rented by someone else.

What’s worse is not only are there too few homes available for households across the U.S., but the gap between household formation and available housing supply is growing.

Also worth pointing out is the income level of households unable to find homes of their own.

Most of the families doubling up (68%) are earning $35,000 or less, making it clear to anyone paying attention that we need vastly higher numbers of more affordable housing units—preferably homes for sale to allow these households to start building wealth.

Providing more affordable rentals is a short-term solution—suitable for policymakers more concerned with votes than with securing long-term benefits for their constituents.

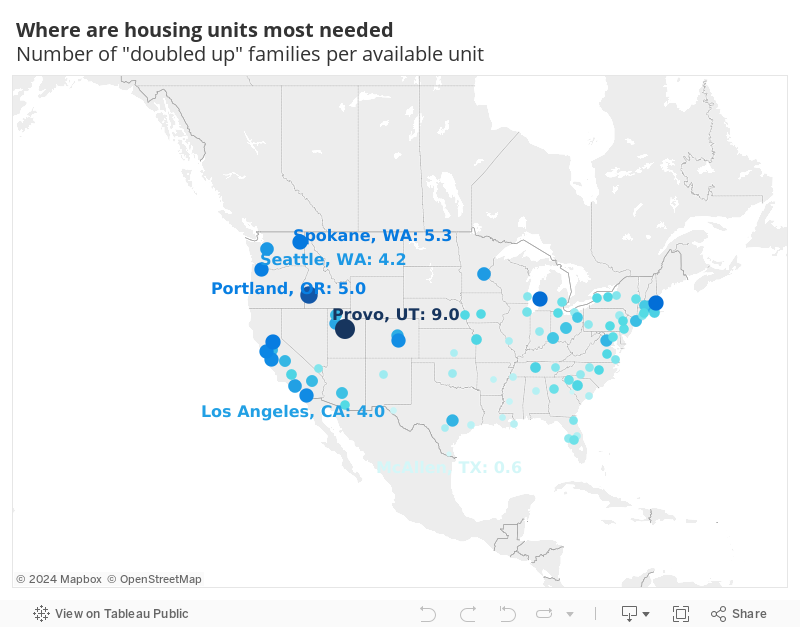

This mismatch between households and available homes is even more pronounced in the most expensive coastal housing markets like Los Angeles, San Francisco, San Jose, San Diego, and Boston, as well as in places like Boise, ID.

Source: Zillow

So, what can policymakers do to turn the tide?

As KCM Chief Economist George Ratiu reminded us in May, construction in the U.S. has not kept pace with household growth.

We’re in an environment in which the market is not temporarily or momentarily undersupplied. We are structurally underbuilt.

In fact, as Zillow’s study pointed out, construction productivity has been suffering since the late 1960s, largely due to land-use restrictions, building approval delays, and stunted growth in the construction sector, all of which have a stranglehold on new home construction.

So, what can policymakers do to turn things around?

For starters, housing experts are almost unanimous in their support for loosening restrictive zoning laws. And, according to the results of Zillow polls, four out of five adults fully support allowing the addition of smaller home types to increase housing options in their own neighborhoods.

That means policymakers at the local level (city/state) are less likely to lose votes over approving new housing projects in those neighborhoods.

To facilitate the construction of more affordable housing, researchers also suggest—

- Speeding up permits for building

- Increasing funds for affordable housing

- Eliminating parking requirements

- Tax incentives to rehabilitate underused housing stock

More than once, too, Byron Lazine has suggested cutting the regulatory fees imposed on construction projects—fees that ultimately result in prices well above the median for those newly constructed homes.

Takeaways for real estate agents

As a knowledge broker for your community, you should know more than most about the factors that limit or even prevent the construction of affordable housing in your area.

Armed with data like the charts in Zillow’s report, find out who pulls the levers affecting new construction and see what you can do to push for policies that would boost the construction of new and more affordable homes for buyers in your market.

Make this part of your efforts to help more renters become homeowners.

- BAM")