Key Details:

- A new Redfin report shows homebuyers now need a household income of $115,000 to afford a median-priced home. That’s roughly $40,000 more than the typical U.S. household earns.

- Housing affordability is at its all-time worst with sky-high mortgage rates and home prices that keep climbing, largely due to low inventory.

- The required household income is up 15% year over year while the typical U.S. wage grew only 5% over the same time period.

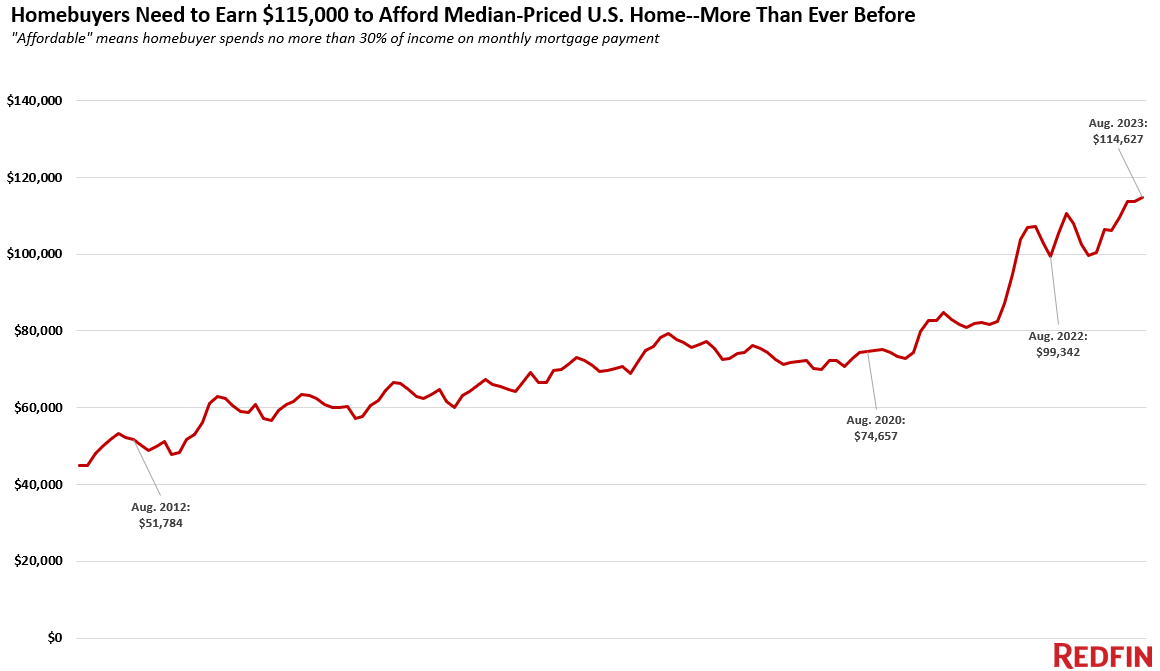

Just when you think you’ve heard it all about how unaffordable housing is right now, a new Redfin report shows the typical American household is $40,000 shy of what they need to earn to afford a median-priced home.

Between mortgage rates and home prices that just keep on climbing, it’s harder than ever for the typical American to afford a home.

In August of 2023, the household income required for a typical American household rose to $114,627—up 15% or $15,285 from one year ago and up 50% from what was required at the start of the pandemic. It’s also the highest required income ever recorded.

Meanwhile, the typical wage grew only 5% over the same period.

Data for the Redfin report is based on its analysis comparing median monthly mortgage payments for U.S. homebuyers in August 2023 and August 2022. Income data is adjusted for inflation.

Housing costs are higher than ever

In August (just two months ago), the average rate on a 30-year fixed mortgage was 7.07%. And they’ve climbed even higher since then, reaching 7.57% (Freddie Mac) for the week ending October 12th—their highest in over two decades.

But even with the dampening effect of those rates on buyer demand, inventory is still low enough that home prices continue to rise.

In August, 2023, the typical American home sold for about $420,000—up 3% from one year ago and only about $12,000 below the all-time high reached in mid-2022.

The typical homebuyer’s monthly mortgage payment in August was $2,866—an all-time high and up 20% from $2,395 in August 2022. At that time, monthly payments had already gone up significantly from the start of the pandemic, when buyers could take advantage of ultra-low mortgage rates and home prices that hadn’t yet begun to skyrocket.

Just to compare, in August 2020, the typical monthly mortgage payment was $1,581—based on that month’s 30-year fixed rate of 2.94% and the median home price of $329,000. A homebuyer at that time would have needed a household income of $75,000 a year to afford the typical home.

Now, a year later, the typical American household income falls $40,000 short of the required amount for a median-priced home.

Last year (2022), the median household income was about $75,000. Hourly wages have gone up in 2023 but not nearly fast enough to keep up with the income necessary to afford a home. The average hourly wage in the U.S. has increased by roughly 5% over the last year.

In a homebuyer’s ideal world, rising mortgage rates would push demand and home prices down enough to make up for high interest payments. But that’s not what’s happening now: Although new listings are ticking up slightly, inventory is still near record lows as homeowners hang onto their low mortgage rates–and that’s propping up prices. Buyers–particularly first-timers–who are committed to getting into a home now should think outside the box. Consider a condo or townhouse, which are less expensive than a single-family home, and/or consider moving to a more affordable part of the country, or a more affordable suburb.

All-cash and move-up buyers have the advantage

It stands to reason that sky-high mortgage rates are less of an issue for buyers who can pay in cash—as well as buyers who are selling a home to purchase another one, who have likely built up equity in the home they’re selling.

Buyers who have a home to sell and who are also in a position to buy their next home with cash are in an enviable position. These buyers tend to earn more than the income required to purchase a home, anyway.

The sticking point for some of these seller/buyers, specifically those who bought their current home at an ultra-low mortgage rate at the height of the pandemic-era market, is that selling now will mean both giving up that low rate and possibly selling their home at a loss.

That said, first-time homebuyers looking to finance their purchase are most likely to feel the sting of the sharp rise in required income. For many, it will mean continuing to rent while waiting for rates to go down or for inventory to go up—or both.

Income needed to buy a home: Biggest increase in Miami—smallest in Austin

Redfin’s analysis highlighted the biggest and smallest increases and declines in the necessary income at the metro level.

Buyers in every major U.S. metro need to earn more to afford a median-priced home, compared to a year ago. That includes metros where home prices have seen year-over-year declines.

Metros where the necessary income increased the most:

- Miami, FL — up 33.4% to $143,000

- Newark, NJ — up 33.4% to $160,000

- Bridgeport, CT — up 32.1% to $183,000

- Dayton, OH — up 31.2% to $60,000

- Rochester, NY — up 30.7% to $66,000

- Hartford, CT — up 30.2% to $95,000

Necessary income has grown the least in pandemic hotspots:

- Austin, TX — up 8% to $126,000

- Boise, ID — up 9% to $127,000

- Salt Lake City, UT — up 13% to $139,096

- Fort Worth, TX — up 13.2% to $98,185

- Lakeland, FL— up 13.4% to $88,639

In 50 of the 100 metros in Redfin’s analysis, homebuyers must now earn six figures to purchase a median-priced home. In all of those metros, buyers must earn at least $50,000 a year.

Metros with the household incomes required to afford a median priced home in the area are all in California:

- San Francisco — up 23.2% to $404,332

- San Jose — up 24.8% to $402,287

- Anaheim — up 28.6% to $300,010

- Oakland — up 17.0% to $249,554

- San Diego — up 28.7% to $241,372

- Los Angeles — up 19.8% to $237,281

- Oxnard — up 23.6% to $233,190

Metros with the lowest income needed to purchase a median priced home were all in the Rust Belt:

- Detroit, MI — up 19% to $52,000

- Akron, OH — up 18.4% to $59,702

- Dayton, OH — up 31.2% to $60,002

- Cleveland, OH — up 22.1% to $61,536

- Little Rock, AR — up 13.9% to $62,729

Takeaways for real estate agents

Depending on your typical client’s price point, the increase in the household income required to purchase a home could have a significant impact on their decision to purchase a home in today’s market.

Many of those transacting now are doing so because they have to. Prepare for these conversations by educating yourself on all the options these buyers have that could mitigate the impact of higher rates and home prices.

And for those who need to sell and who could buy their next home with cash, use this script to help them make the most of their advantage.

- BAM")