You’ve got a lifestyle in mind. Will you be financially better off renting or buying it?

Reporting on monthly affordability differences illuminates only a small chunk of this question, which also involves future asset streams, tax breaks, and big differences in upfront costs. Incorporate all the main features into this major economic decision, and the picture is much less straightforward.

At that time, the pressure that had built up on single-family rent growth after eviction moratoriums was releasing. Today, the tables have turned with single-family rent growth on a tear, hitting 13% in February 2022, according to CoreLogic. Home prices are expected to slow down significantly as the Federal Reserve switches course to tackle rampant inflation.

The average mortgage rate for prime borrowers hit 5.3% this week, the fastest increase in decades.

How has all that housing market trauma affected the buy versus rent calculus? Turns out, by a lot or only a little, depending on your expectations for the future. I could be sorry to say that this is the quintessential economist’s post: multiple answers to one question. But our system has never been shocked like this before.

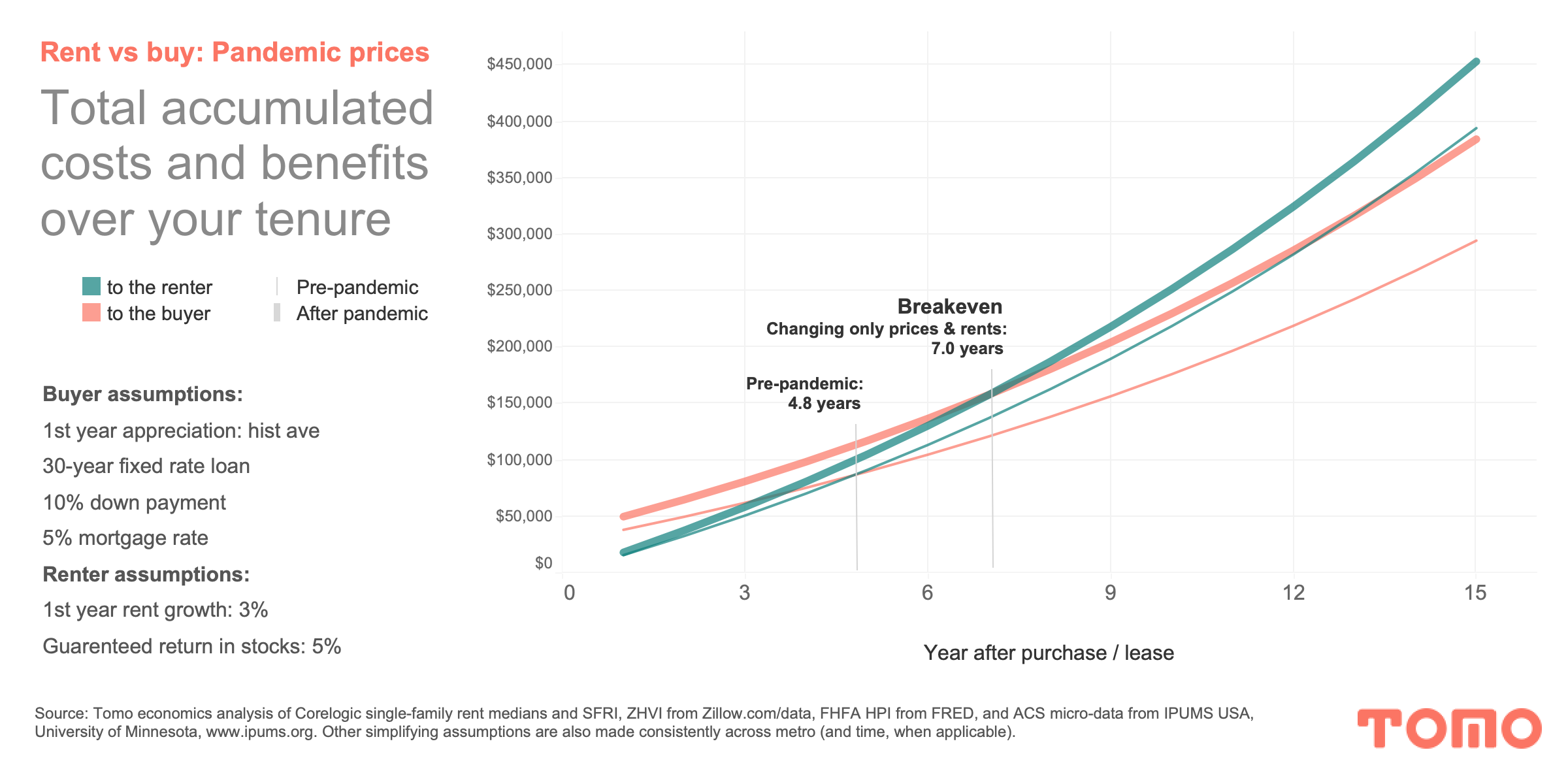

So, first what if the pandemic had never happened?

The typical home price for the U.S. was roughly $250K and growing a more moderate 4.5% a year, still above the long run average of 3.7% despite prices exceeding previous bubble peaks. That was all good because at that time, incomes had risen to keep years-to-save significantly lower than 2007 highs. Typical rent for a similar property might have ballparked for around $1,250 a month and grew around 3% a year on average. Investors were starting to worry about corporate debt and inflated stock prices. The average mortgage rate for the prime borrower was around 4.75%.

If we anticipated all your costs as a homeowner:

- transaction costs at purchase and sale

- mortgage payments

- insurance

- maintenance

- property taxes

- capital gains taxes (in many states a sales tax can also apply)

Then we can also offset them by the home equity growth and a massive capital gains exclusion. We can do the same for the renter:

- rent

- renter insurance

To compare apples to apples, we’d assume the renter invests the downpayment and foregone transaction costs into the stock market instead (as well as accounting for the difference in renter vs. homeowner recurring costs by saving into or withdrawing from the same investment account).

We could simulate this renter’s alternative and figure out how long it would take for the benefits of homeownership, such as:

- avoiding ever-increasing rent/fixing part of your monthly payment

- the leveraged nature of the investment

- the tax breaks

- functionally using part of the monthly payment as “forced savings”

These overcome the down sides, such as:

- big transaction costs

- and in many markets too-high prices

To simulate this situation, we need to make assumptions about the path of the future. Let’s assume:

- the historic average growth rate for home values by region

- a modest 3% growth rate for rents

- a 5% average rate of return for the renter’s alternative investment vehicle

- and that the buyer gets a 5% mortgage rate on a 30-year fixed rate loan with a 10% down payment

- as well as a myriad of other simplifying assumptions (go deep on the rent vs buy calculation).

Today, two big things have changed

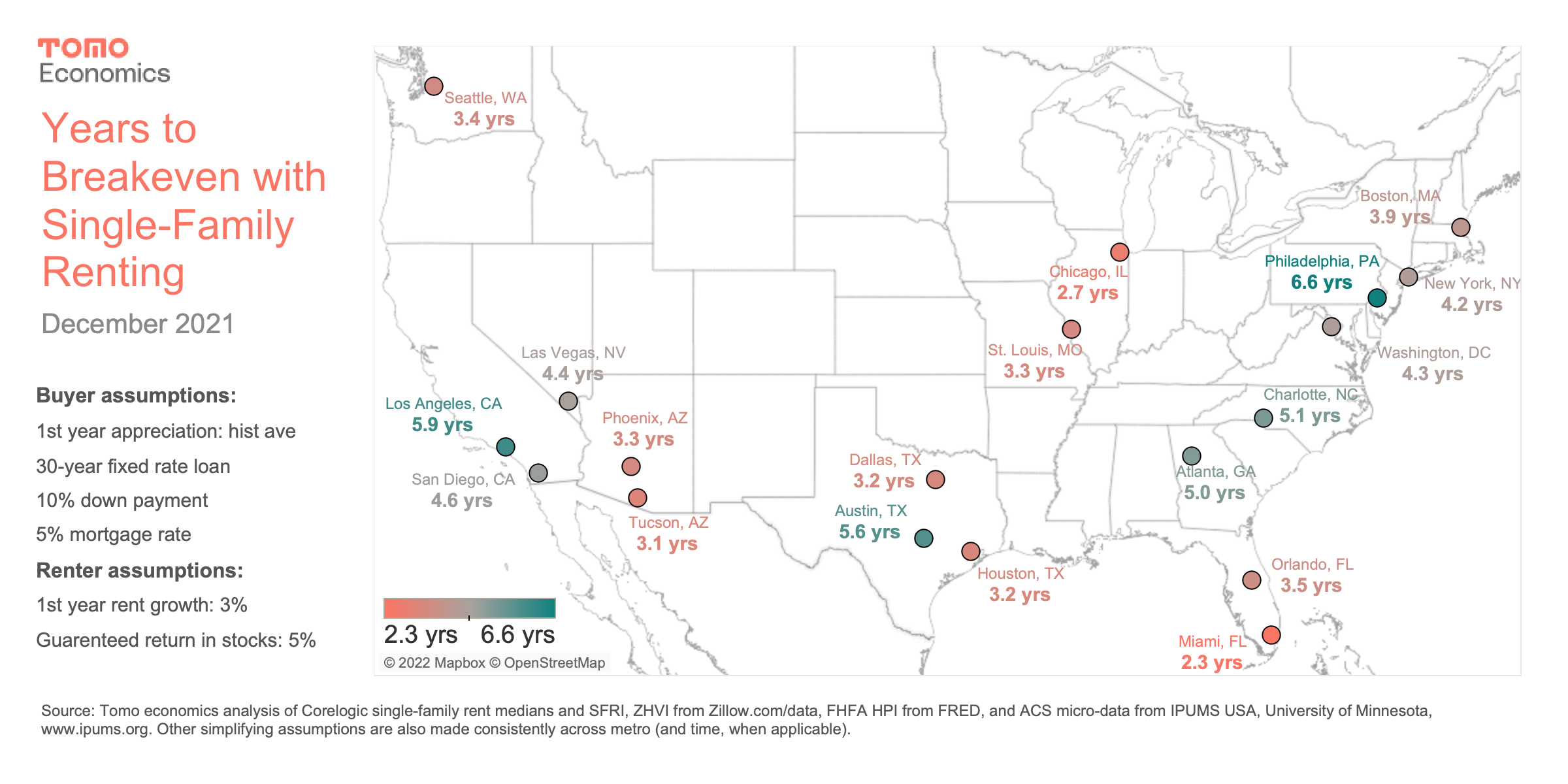

- What are the potential prices and rents for the lifestyle you’d like?

- And what are you comfortable assuming about the future?

Mortgage rates are higher (growing?), but not too much higher, than pre-pandemic levels.

If all we change is the purchase price and the first year’s rent, we’d have to account for this:

- The U.S. typical home value reached $326K by Dec 2021, up over $75K in only two years.

- 3-bedroom, single-family rent was up to $1,450 by Dec 2021.

Changing nothing else but that increase in the price-to-rent ratio lengthens the breakeven to 7 years. But what if we also incorporate the expectation for more aggressive rent growth?

Prices could keep rising too. 40 years ago when Volker pulled the brakes to combat inflation, CPI topped 14%. National home value only stalled. Don’t imagine a 2007-08 housing crash to bring down these inflated home prices. A foreclosure wave is NOT expected. The credit history of recent buyers is solid relative to the year leading up to the housing bubble and Global Financial Crisis.

That would increase the price-to-rent ratio too. A move that would lengthen the breakeven, except your mortgage payment is fixed so the price growth is home equity.

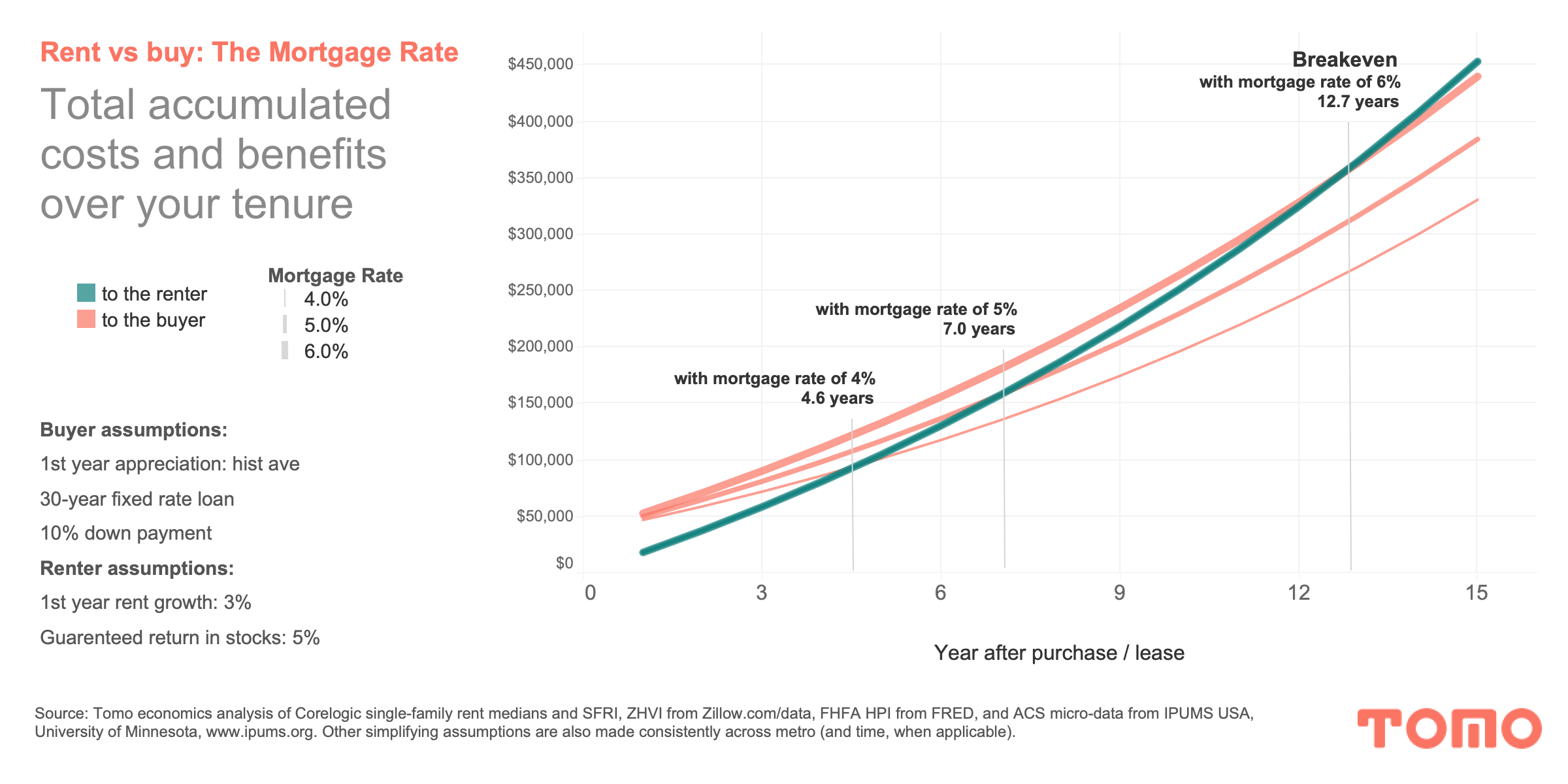

When prices exceed rents this badly, the mortgage rate matters.

A mortgage is a leveraged investment. After contributing only the down payment, you benefit from the appreciation on the full home value, not just your contribution. The mortgage rate and the interest you pay on the loan is the cost of leverage. Stock market investments are typically not leveraged because it’s too risky. Stock markets are volatile so you could too easily go underwater on your loan.

Add a high price-to-rent ratio, which further exacerbates the relative monthly costs as high prices meet high rates and the simulated breakeven changes dramatically with mortgage rates.

Increasing the rent growth over the first year to 10% in the scenario graphed above and keeping the home value forecast the same, the breakeven with a 6% mortgage rate drops down from 12.7 back to 7.0 years with a much smaller spread between the breakevens with 4, 5, and 6% rates.

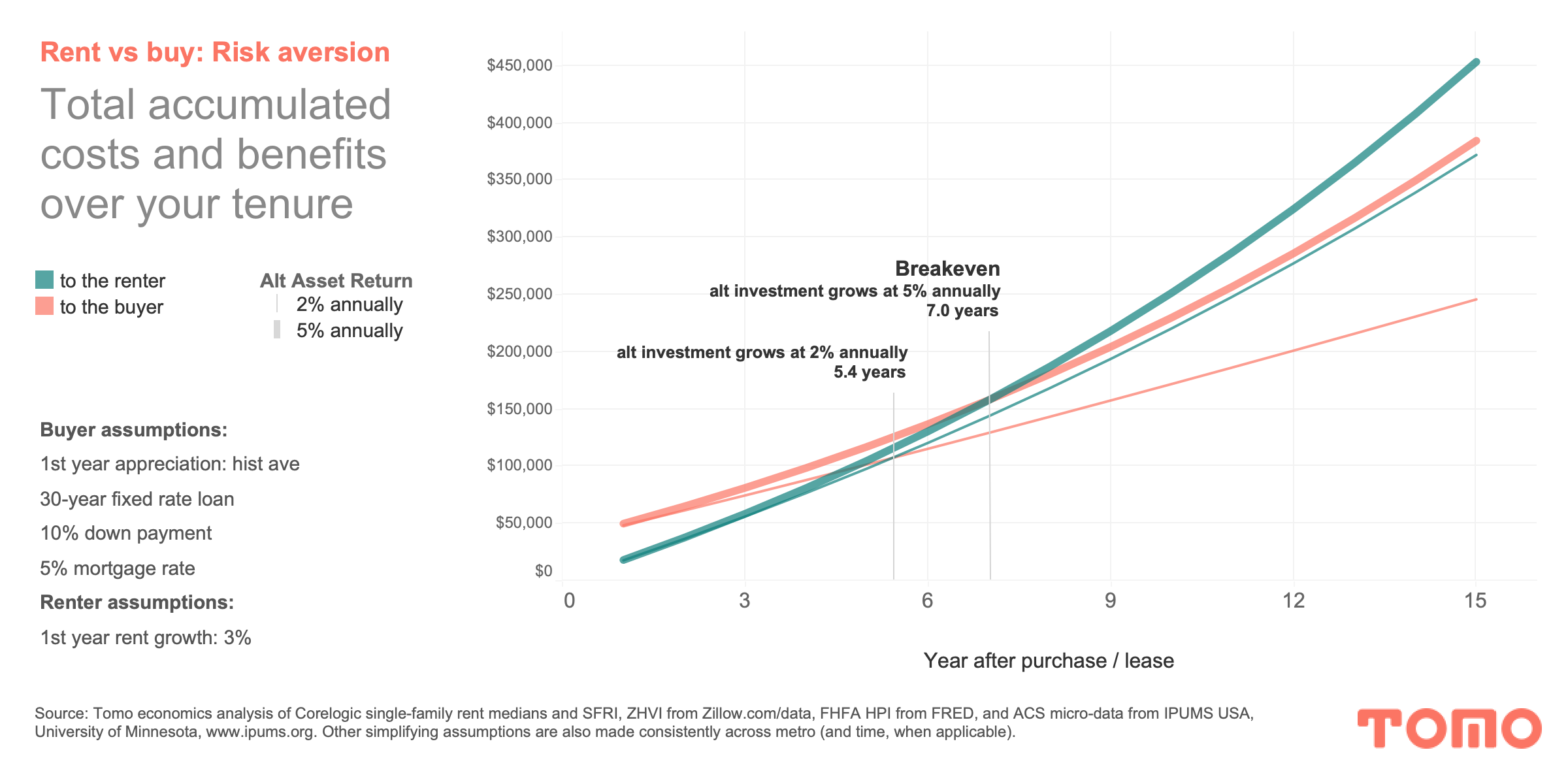

The renter’s alternative investment

Stock market performance or whatever alternative investment the renter will pursue is also critical to the breakeven.

The paradox is not such a paradox to behavioral economists who have explored our general lack of financial literacy and the curious nature of people to suffer more from a loss than they celebrate a gain. Having to pull money out in a down market sucks from a math perspective too.

So if, as a renter, your alternative investment to home equity is to put your money in a safe account, say a Certificate of Deposit (CD), then your alternative investment is low yielding, say 2% annually. The opportunity cost of buying/homeownership drops because you’re not missing out on high-yielding stocks after all. In our example, the breakeven drops from 7 to only 5.4 years.

Wrap it up, Skylar

Home buying is the dominant path for the average household into wealth and investment.

This is probably because we subsidize it with tax breaks and wrap it in accomodative monetary policy and an insulating regulatory environment. Probably because we’re a bit risk averse and home buying is familiar. Probably because it’s a financial path that reinforces stability.

It’s a financial investment that becomes more advantageous the more it’s a part of an intent to stay—to invest in your home and your community. Now’s a time for resilient decisions.

Now is also the time to figure out how to de-gnarl this gnarly decision. Both the financial literacy piece but also the process itself. Fix the process, turn up the transparency, increase the sanity, and lower transaction costs. Optimize the secondary market and lower the rate. The latter shortens the breakeven, making more futures pay off. The former are how you do it.

On it.

- BAM")